Get Specialized with our Financial Planning & Analysis (FP&A) Program

Support business leaders in their decision-making with best-in-class financial models to evaluate and forecast the financial performance of a company.

Bottom-up budgeting is a budgeting method that starts at the department level, with each department creating a budget and moving it up to the top, creating a company-level budget. Each department is required to compile a list of the things it needs, hires it plans to make, projects it plans to carry out, as well as cost estimates for all of these.

The estimates of all the departments are then summed up to get the overall company budget. This budgeting process requires the managers of each department to give their input since they are in the best place to know all of the various needs and costs.

Top-down budgeting is a budgeting method where top management prepares a high-level budget for the company. This budget is based on overall company objectives and strategies and is then passed down to department-level managers for implementation.

While department-level managers may make suggestions to the company budget, it’s up to senior management as to whether or not to incorporate those suggestions. After the budget is created, senior management makes specific allocations to the different departments, which must then create their own budgets based on their budget allocation and goals.

The two different approaches to budgeting are naturally at tension with each other and even with themselves.

On the one hand, an ideal budgeting approach would result in buy-in and acceptance from the entire company. However, this is difficult to achieve regardless of budgeting approach.

For example, a top-down budget is effectively imposed on junior managers and employees who may disagree with the way this budget allocates resources. Therefore, there may be pushback from the employees that must implement and follow the top-down budget.

The bottom-up budget has similar issues. Since each department budget is effectively created in isolation, the budget itself may not be in line with other department heads and overall company goals.

Choosing the right approach — whether bottom up or top down — really depends on the company’s needs and culture.

The following are some generalities regarding which approach is better for a certain type of organization:

The top-down budgeting process is generally better for companies with a centralized decision-making authority and uniform operations. Examples of this would be a large retail or restaurant chain or a large manufacturing firm.

The top-down approach is also better for companies that need to respond quickly to changes in a dynamic business environment, and management doesn’t have time to get input from many stakeholders.

A situation where the top-down approach is pretty much required would be if a company is in decline and in need of a turnaround. In a turnaround, there are often difficult but necessary changes that must happen in order for the company to mitigate its decline. In this case, the company cannot afford to take the time to use a bottom-up strategy.

The bottom-up approach is usually better suited for decentralized organizations, where decision-making is spread across various business units. Examples of decentralized organizations might be large multinational corporations or diversified conglomerates. These types of organizations are also likely to have robust systems and processes in place that allow for the additional complexity of bottom-up budgets.

Another situation in which a bottom-up budget might be preferred is for industries that require constant creativity and innovation to thrive. Industries in need of constant innovation will need the input of day-to-day employees and stakeholders to stay on top of trends. This makes bottom-up budgeting a better approach. Examples of industries that are constantly innovating are technology firms or pharmaceutical companies.

Below are the general steps to creating a bottom-up budget.

If satisfied, senior management will approve the various budgets and will monitor how well different teams’ actual results compare to the budget in a process known as variance analysis. However, if company leadership is not satisfied with the budget, it will ask the departmental managers to make necessary changes before the budget is again submitted for approval.

The top-down budgeting process starts with senior management meeting to come up with the objectives for the year. As part of this, management will discuss and determine high-level targets for the company in terms of sales, expenses, profits, etc. Department managers and lower-level staff do not usually participate in these discussions but may put forward suggestions for consideration.

Once management finishes preparing the targets, the objectives are passed on to the finance department for allocation to the different departments and projects. Management deploys resources based on the finalized targets set during the budgeting process.

Once all of the budgets are finalized, they are loaded into a financial system to track monthly expenditures and other metrics via variance analysis. The departments receive monthly or periodic reports to show the amount of revenues and expenses compared to the allocated budget. Leaders must monitor any variances and understand how actual results differ from expectations.

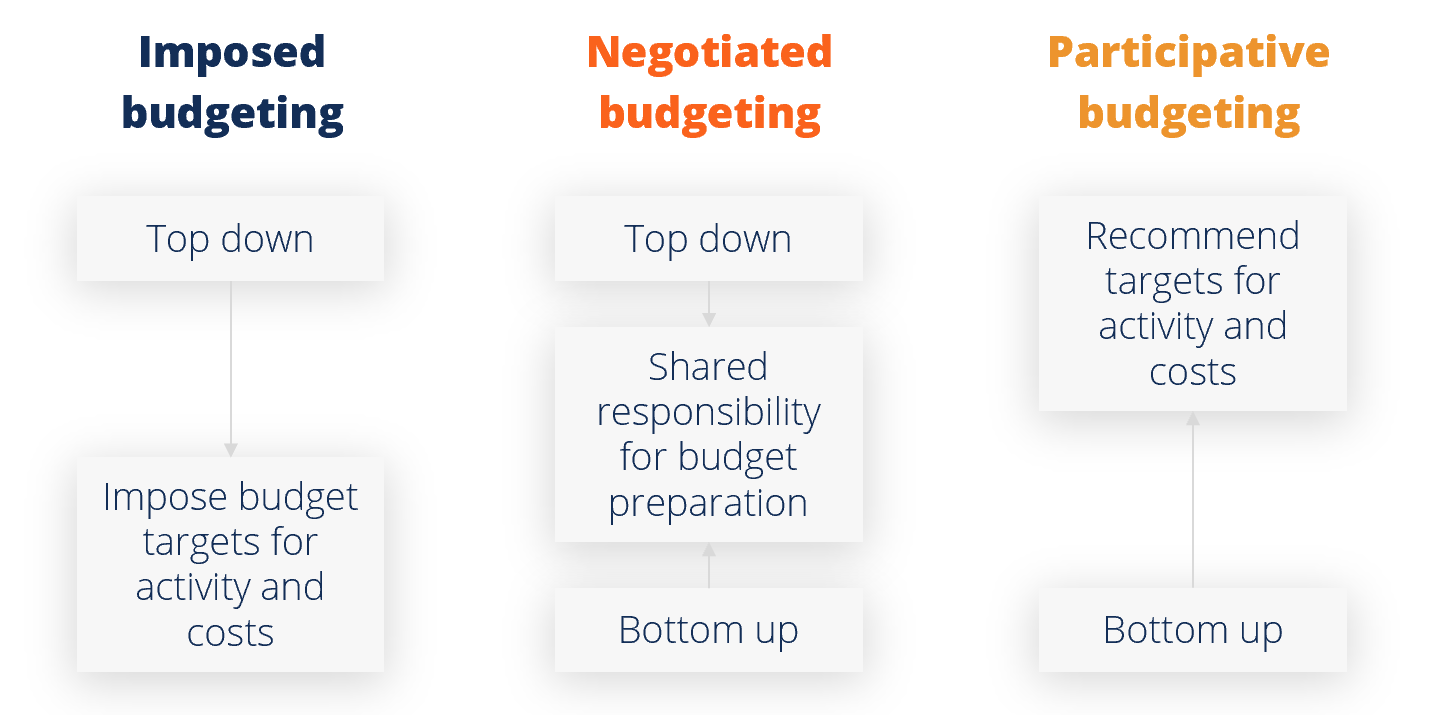

Top-down vs bottom-up budgeting approaches both have their merits and drawbacks. Often, organizations may adopt a hybrid or negotiated approach, with elements of both top-down and bottom-up budgeting.

As an example, upper management may outline some of the most important company targets, while allowing individual departments the potential to develop their own detailed budgets that will contribute to these targets.

Regardless of which process a company chooses, there are some crucial tips to consider when implementing a formal budgeting process.

Thank you for reading CFI’s guide on Bottom-up vs Top-down Budgeting. To keep advancing your career and skills, the following CFI resources will be useful: