Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

An event where a monetary contract is terminated when a delivery obligation or redemption is completed

Called away is an investment term used to describe an event where a monetary contract is terminated when a delivery obligation or redemption is completed. The delivery obligation refers to the distribution of an underlying asset – such as a bond – to the other party in the monetary contract.

In most cases, a called-away situation occurs with options and callable bonds. Generally, investment instruments that include the option to be “called away” face drawbacks, such as lack of control through unpredictability.

For an underlying asset to be called away, it must first match one of the three specific situations described in detail below.

For our example, let’s assume that an investor entered into a short sale agreement with their broker.

Within the agreement, the investor borrows 250 shares of Apple (AAPL) from their personal holdings and decides to sell the shares on the financial market.

The sale price is locked in, but the investor is now obligated to give back the 250 Apple shares to their broker from which they borrowed. Considering the investor wants the largest return, they decide to wait until the price of Apple drops. While waiting, the broker requests for their 250 shares to be returned.

The shares are then “called away,” where the investor is now forced to purchase 250 Apple shares and return them to their broker, regardless of the price.

In the financial world, a callable bond or redeemable bond is a financial instrument that is issued by an organization to an investor.

A callable bond is different from a regular bond in the sense that the organization that issued the bond holds the option to redeem (buy back) the bonds from the investor before the maturity date.

If an organization decides to redeem the bonds they issued to the investor, the bonds would be called away, and the bonds would be sold back to the company at a predetermined price.

The most common situation for a call away occurs under call option transactions. They allow an investor the option to buy a number of shares in a company at a set price. If the share price rises above the strike price, the option is exercised, and the shares are then called away. We explain the concept in detail in the example below.

In order to understand the dynamics of a called away scenario, it is beneficial to present a real-world situation where it may occur in the financial market. As mentioned, we will describe a situation where a call option is exercised.

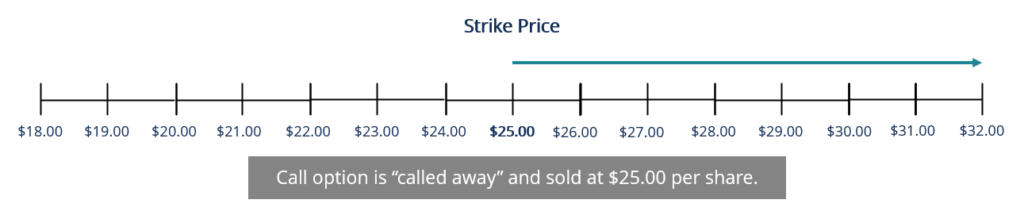

Let’s say that there is a company by the name of ABC, and their stock is trading at $23.00 in October of 2019. We own some of ABC’s shares, but we do not think there will be more than a 10% increase in price until January 2020.

Based on that assumption, we decide to sell a 10% out-of-the-money (OTM) call option (with a $25.00 strike) that expires in January 2020. We get a small premium (income) from the sale.

For the call option to stay “out-of-the-money” or “OTM,” the underlying price of the stock must trade below the strike price of the call for the entire period. In this case, below $25.00.

If, however, ABC shares begin to trade above the strike price of $25.00, the option will be exercised by the holder, and our shares will be “called away.”

When the shares are “called away,” they are taken from our account due to the contractual obligation of the call option.

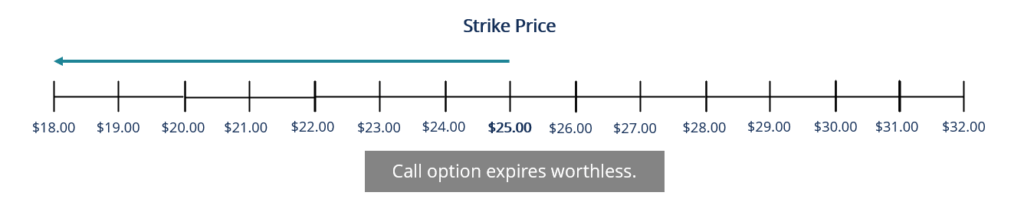

On the other hand, if the ABC shares trade below the strike price through January 2020, the call option will not be exercised and will expire worthless.

We will be able to keep the premium from selling the option, and we still hold the initial shares.

To keep learning and advance your career, the following resources will be helpful: