Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment.

An individual who places their assets in a trust to be delivered to a beneficiary

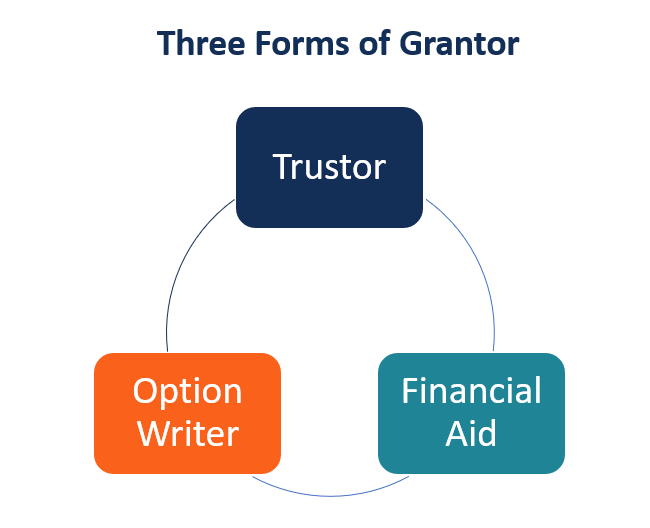

A grantor can be used in three distinct forms:

First, a grantor is an individual who is responsible for the creation of a trust by placing their assets in the trust to be held by a trustee and eventually delivered to a beneficiary. A grantor can also be referred to as a trustor or a settlor.

A second use of the title grantor refers to the seller or writer of a call option or put option. Options are financial instruments that are classified as derivatives, as they derive their value from an underlying asset, typically a stock.

The last use of the term grantor refers to an individual or entity that provides financial aid in the form of grants.

As mentioned above, the term grantor can be used to refer to an individual who creates a trust by placing their assets within a trust to be delivered to a beneficiary. A trust is simply a financial instrument that is designed to hold assets such as money, investments, and property, usually for the purpose of being delivered to a beneficiary in a timely and smooth manner.

Transferring assets can be a complex and lengthy process without using a trust. Since a trust can be set up with a contractual arrangement of when and how to disperse assets, the trustor can be comfortable knowing that their funds are being transferred in the way that is originally intended.

Reasons for utilizing a trust include:

Again, as mentioned, another term for grantor can be used to refer to the writer or seller of an option. Options refer to contracts that give the option holder the right to buy or sell a specific asset at a specific price (known as the strike price) for a period of time.

Characteristics of an option:

The underlying asset is usually some form of a financial asset; however, it can be a variety of different assets, such as:

The writer or seller of an option possesses the obligation to buy or sell the asset according to if and when the buyer of the option exercises their option to either purchase or sell the underlying asset.

For example, if someone purchases a call option on Stock ABC, they have the right to purchase the stock at the strike price. If they exercise the option, then the seller of that call option must sell Stock ABC at the strike price.

If the seller owns Stock ABC, they can simply sell the shares that they currently own. However, if the seller does not own Stock ABC, they must purchase Stock ABC in the open market to sell to the option holder. If the seller does not own Stock ABC, this is referred to as writing a naked position.

A grantor can lastly be referred to as an individual or entity that provides a financial grant. A grant is an award or benefit given from one entity to another individual or entity for the purpose of facilitating a goal or incentivizing an action or performance. Grants can be thought of as gifts, given that they do not need to be paid back to the grantor.

Typical scenarios where grants are issued are:

Within stock options and some other forms of grants, there are lock-up or vesting periods where the grantee (receiver of funds) must wait before receiving the grant.

The grantor in such cases would be:

Thank you for reading CFI’s guide to Grantor and its different forms. To keep learning and developing your knowledge base, please explore the additional relevant resources below: