Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

An agreement between two counterparties to buy or sell a fixed income instrument at a specified date, price, and amount in the future

A fixed income forward contract refers to an agreement between two counterparties to buy or sell a fixed income instrument at a specified date, price, and amount in the future. The contracts are used for speculation or hedging purposes by locking in the fixed income delivery price today.

Fixed income is a general term for investments that generate fixed dividends or interest payments and a final principal repayment at maturity. Common fixed income securities include government and corporate bonds and Treasury bills (T-bills).

Investors can make a profit from fixed income investments through the fixed payments and price appreciation. Prices are affected by three major factors – inflation, interest rates, and the bond’s rating.

Fixed income investment prices are negatively correlated to inflation. Because coupon payments and the principal repayment are fixed, increases in inflation will erode purchasing power and therefore returns.

Fixed income investment prices are also negatively correlated to interest rates. At inception, fixed income instruments are priced based on the prevailing market interest rates. As time goes on, the market interest rate changes, and the fixed income investments value must change to account for it.

If the market interest rate increases, the fixed income investment prices will decrease because new bonds issued will now pay higher coupon amounts, and investors are stuck holding lower-yielding securities. Vice versa, if the interest rate decreases, existing fixed income investment prices will increase.

Within fixed income securities, ratings are specific to bonds. Ratings convey the creditworthiness of the bond and are issued by credit agencies, such as S&P and Moody’s. High-quality bonds (investment grade) are safe investments and therefore come with high ratings, while low-quality bonds (non-investment grade or junk) bonds are considered risky and are given low or no ratings at all.

The rating exerts a direct impact on the bond’s interest rate; investment-grade bonds pay lower interest while junk bonds pay higher interest to compensate for the additional risk. If a bond gets downgraded, all future bonds from that issuer will be required to have higher interest.

A forward contract is a derivative instrument used to speculate or hedge fixed income price movements. At initiation, parties of the contract agree on a delivery price – the price at which to exchange the fixed income instrument for on the future date.

Forward contracts are similar to futures contracts, the difference being that forwards are traded over-the-counter (OTC), meaning that it is non-standardized and customizable, while futures are traded on regulated exchanges.

Investors can speculate on future prices and use a fixed income forward contract to lock in the price today for a profit. For example, an investor may believe that interest rates will drop, or a bond’s rating will get upgraded in the future, which will cause the bond to increase in value.

Therefore, they enter a fixed income forward contract to buy the bond in the future and lock in the delivery price today. If the speculation proves right, the investor could buy the bond in the future for cheaper than its market value.

Investors may also hedge their investments with a fixed income forward contract. For example, an investor currently holds a bond but is worried about increasing interest rates or a rating downgrade in the future, which will decrease the bond’s price.

They can enter into a forward contract to sell the bond in the future at a set delivery price determined today. If the bond decreases in value in the future, they can sell the bond at a higher delivery price relative to the market price.

Forward contracts are a zero-sum game because one party’s profits are another party’s losses. Two parties enter the contract with opposing expectations of the fixed income’s future value, and only one result will take place.

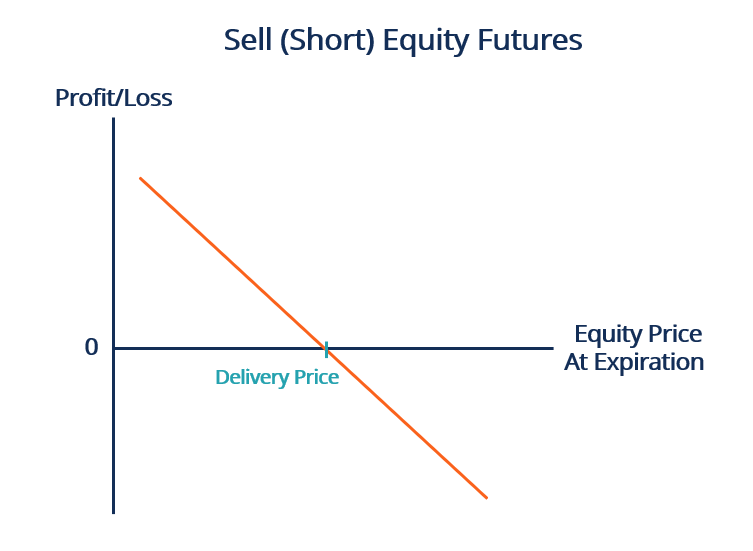

As shown in the graph above, the party that is buying makes a profit when the market price of the fixed income instrument at expiration is higher than the delivery price. It means that the buyer can purchase the fixed income for cheaper than what it sells for on the market.

On the other hand, the buyer incurs a loss when the market price at expiration is cheaper than the delivery price locked into the contract. The seller’s outcomes are the exact opposite of the buyer’s.

CFI offers the Capital Markets & Securities Analyst (CMSA)® certification program for those looking to take their careers to the next level. To keep learning and advance your career, the following resources will be helpful: