Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Measures the number of people who have filed for unemployment benefits

Jobless claims, reported weekly by the U.S. Department of Labor, measure the number of people who filed for unemployment benefits.

There are two types of jobless claims:

Of the two types of jobless claims, the initial claims reading is considered of greater importance and is regarded as a leading economic indicator (meaning there is a predictive power of the reading on future economic conditions). It is because there tends to be a negative relationship between initial claims and the employment rate – as initial claims decline/increase, the employment rate tends to increase/decline.

A rising/declining employment rate can signal greater/lower disposable income, leading to higher/lower consumption, resulting in the belief of a strong/weak economy. Furthermore, the fact that the jobless claims figure is published weekly lends itself as a favorable leading economic indicator to use by analysts and economists.

The jobless claims reading is commonly compared to consensus estimates, of which material deviations can generate a market reaction.

Confusion may arise from whether a better-than-expected jobless claims reading refers to a higher or lower actual reading versus expected:

The market reaction to the jobless claims reading depends on the current business cycle and monetary/fiscal policy expectations. In general, the market reaction tends to be positive when jobless claims are lower than expected.

For example, in September 2021, initial jobless claims were 340,000 for the week versus a consensus of 345,000, prompting optimism regarding the U.S. labor market. As a result, markets reacted positively, with the S&P 500 and Nasdaq Composite climbing to new respective records.

Recall that jobless claims measure the number of people who filed for unemployment benefits. According to the U.S. Department of Labor, to generally qualify for unemployment benefits, the individual must:

It is important to note that there is potential for the jobless claims reading to point to an incorrect inference on the state of the labor market. It is because numerous types of people are excluded from the reading, such as:

As an extreme example, there may be a low jobless claims reading coupled with a low employment rate if workers have been claiming unemployment benefits for so long that they run out of benefits to claim. In such a case, a low jobless claims reading may indicate a healthy labor market, when in fact the labor market may be under extreme distress as workers struggle to find work over an extended period of time.

It is important to use other leading economic indicators in conjunction with the jobless claims reading when seeking to predict the outlook of the economy.

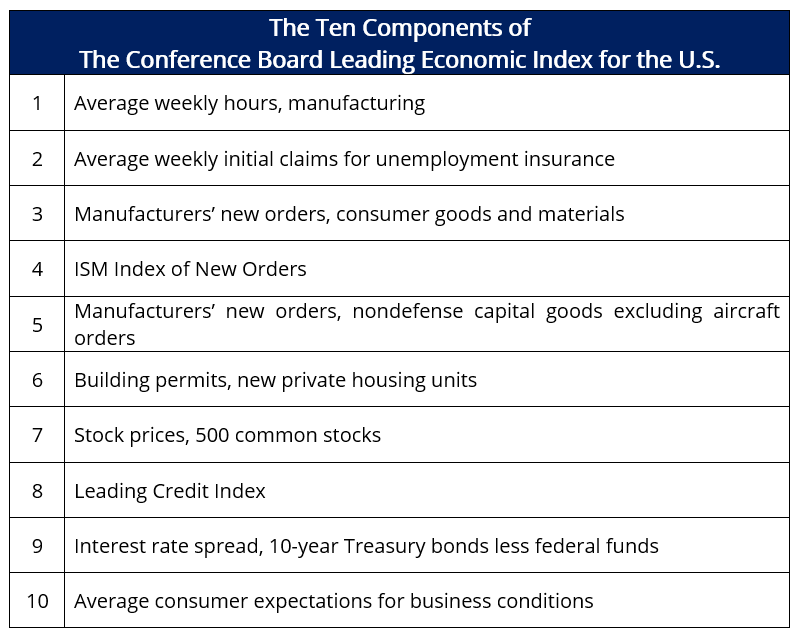

As mentioned, initial jobless claims are considered a leading economic indicator. In fact, the initial jobless claims reading form one of the ten components of The Conference Board’s Composite Index of Leading Indicators, outlined below:

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: