Retail Industry Comps Template

Retail Industry Comps Template

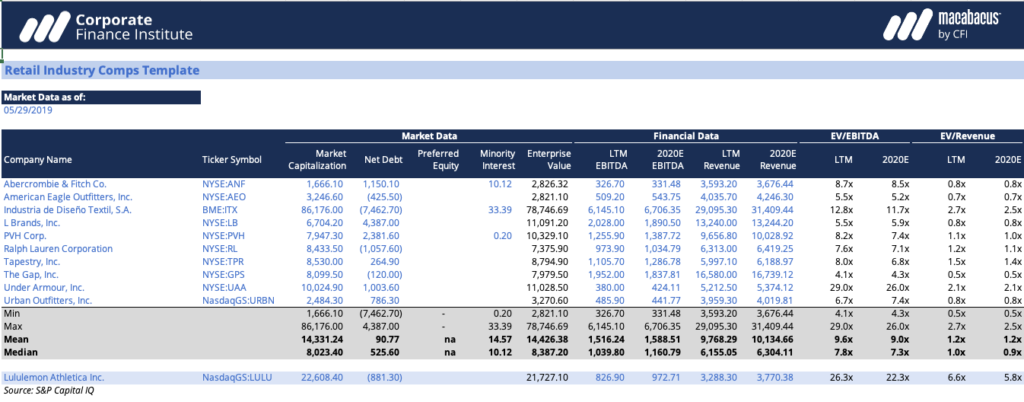

Comparable company analysis, often referred to as “comps,” is a valuation method that uses financial ratios of similar businesses to value a company. CFI’s retail industry comps template provides a number of comparable companies for Lululemon Athletica Inc.

Comparable Company Analysis

Comparable company analysis is a commonly used method of valuation. Comps analysis looks at similar businesses to the company being valued and compares different financial ratios. This is a relative valuation method rather than an intrinsic method of valuation such as a discounted cash flow analysis.

Comps analysis is very useful since it involves fewer assumptions than many other valuation methods. It is also relatively simple and easy to use. In this retail industry comps template, you can easily see what metrics such as the EV/EBITDA and EV/Revenue are for the industry.

Download the Free Template

Enter your name and email in the form below and download the free template now!

Choosing Comparable Companies

One of the most important steps in doing a comparable company analysis is selecting the companies that will be used for the analysis. It is vital to choose companies that are relevant to the business you are trying to value. There are several factors that can be taken into consideration when choosing a company. CFI’s retail comps template considers these factors when looking at Lululemon Athletica Inc:

- Industry Classification

- Size

- Geography

- Growth Rate

- Profitability

- Capital Structure

Since this template is industry-specific, industry classifications are already matched. It is important to note that industry classifications can be broken down into subcategories. For example, Lululemon is in the clothing industry, however, it is a retailer. Other retailers such as Inditex are therefore an appropriate match.

Furthermore, Lululemon focuses on sportswear. Companies like Under Armour, which produce sports clothing are also considered. Other factors must also be taken into account, for example, Nike is not included in the list of comparables even though they offer sportswear. This is because a significant portion of their revenue comes from shoes, which Lululemon does not focus on.

Size and geography are straightforward to match, however, growth rate, profitability, and capital structure involve further assessment of each company’s financials. This template prioritizes size and geography and also includes the following characteristics:

- Similar size and geographical coverage

- Similar size and different geographical coverage

- Different size and similar geographical coverage

- Companies with similar business models

Additional Resources

For more resources, check out CFI’s Business Templates Library to download numerous free Excel modeling, PowerPoint presentations, and Word document templates. Also, see all our financial modeling resources and Excel resources.

Excel Tutorial

To master the art of Excel, check out CFI’s Excel Crash Course, which teaches you how to become an Excel power user. Learn the most important formulas, functions, and shortcuts to become confident in your financial analysis.

Launch CFI’s Excel Crash Course now to take your career to the next level and move up the ladder!