Journal Entry Template

Download our free journal entry template

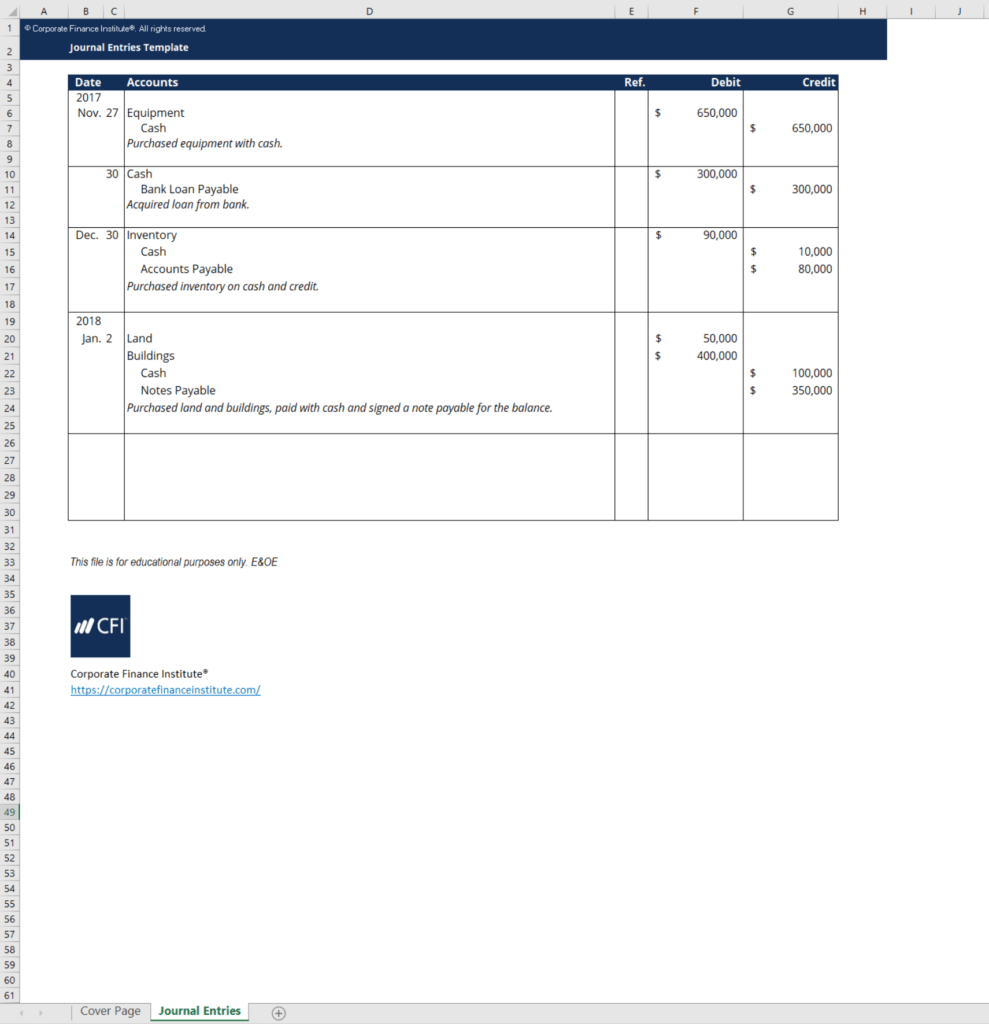

Journal Entry Template

This journal entry template will help you construct properly formatted journal entries and provide a guideline for what a general ledger should look like.

Here is a preview of CFI’s journal entry template:

Download the Free Journal Entry Template

Enter your name and email in the form below and download the free template now!

Entering Journal Entries

A journal is the company’s official accounting record of all transactions that are documented in chronological order. While most modern companies use accounting software to enter journal entries, journals were the primary way of recording transactions in the past. While no longer common, understanding how to do a manual journal entry is still important when learning the fundamentals of accounting.

For every single journal entry, debits and credits must be equal to maintain balance in the accounting equation (assets = liabilities + shareholders’ equity). Therefore, when conducting journal entries, you will need to keep in mind four factors:

- Which accounts are affected by the transaction

- Whether each account is increased or decreased

- How much each account is changed by

- Ensuring that the accounting equation maintains balance

The best way to remember how to do journal entries and how each account is affected is through practice. This idea can be extended to all accounting fundamentals, as there are many accounting rules that need to be upheld.

Without proper journal entries, a company’s can quickly find its financial statements in disarray, with many inaccuracies. Use CFI’s journal entry template to help you practice and maintain accuracy with your journal entries.

Example of a Journal Entry – Purchasing Inventory

Purchased inventory costing $75,000 for $5,000 in cash and the remaining $70,000 on the account.

DR Inventory 75,000

CR Cash 5,000

CR Accounts Payable 70,000

More Free Templates

For more resources, check out CFI’s Business Templates Library to download numerous free Excel modeling, PowerPoint presentations, and Word document templates.

Also, see all our financial modeling resources and Excel resources.

Additional Resources

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

The Financial Modeling Certification

Analyst Certification FMVA® Program

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

The Financial Modeling Certification

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?

Excel Tutorial

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

The Financial Modeling Certification

Launch CFI’s Excel Crash Course now to take your career to the next level and move up the ladder!

Accounting Crash Courses

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

The Financial Modeling Certification

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.