Get In-Demand Finance Certifications

Download our free t-account template

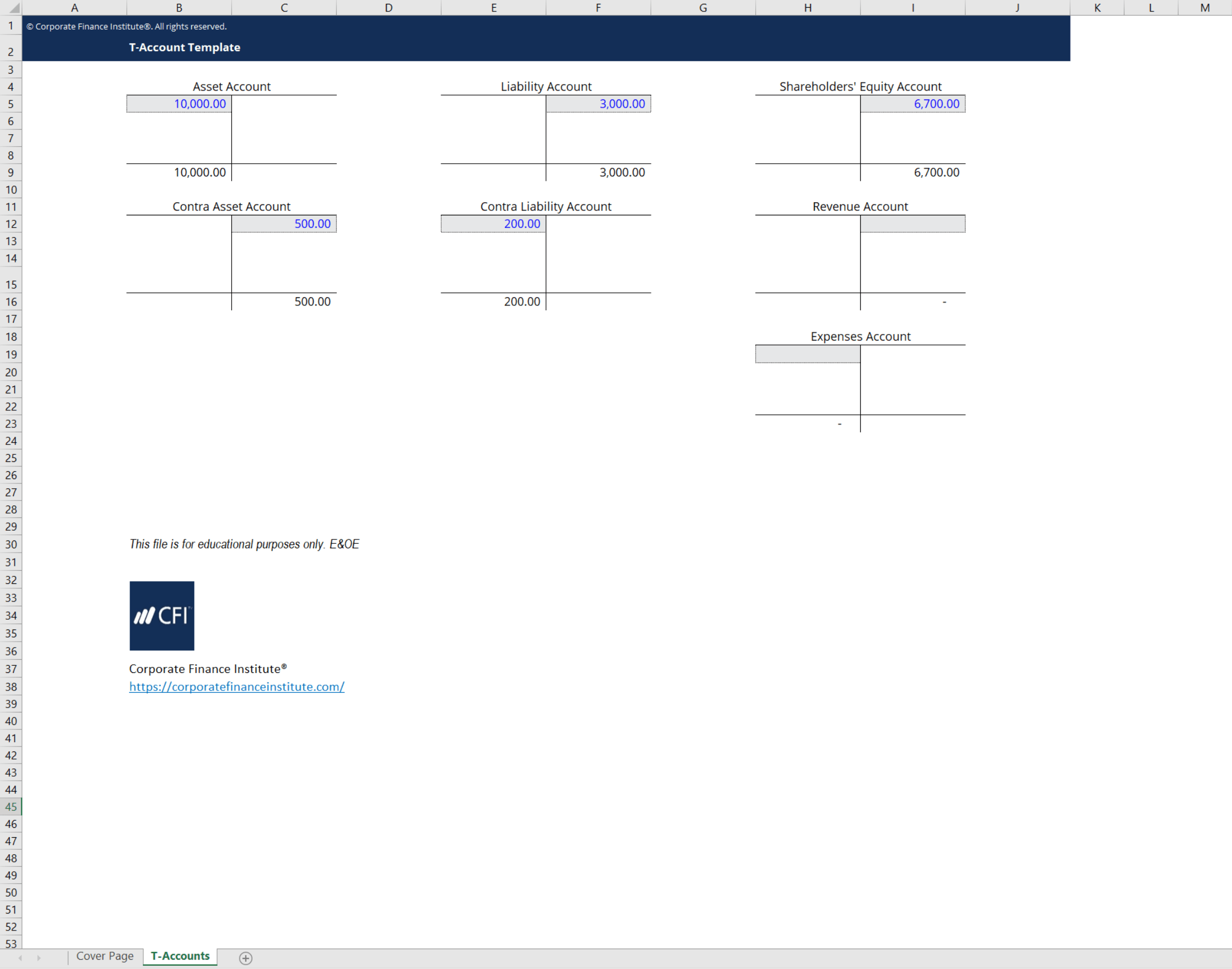

This t-account template helps you organize and balance the debits and credits for your transactions and journal entries. Use this template to visualize the accounting perspective of how transactions affect a business’ different accounts.

Here is a preview of what the t-account template looks like:

Enter your name and email in the form below and download the free template now!

T-Accounts are a graphical representation of individual accounts on a company’s ledger. They are shaped like a ‘T’ to help visualize how transactions, debits, and credits affect a company’s accounts. By graphically showing the debits and credits, t-accounts help determine what type of account each individual item is and how a transaction changes its balance.

For example, by looking at the t-account template preview above, you can see an asset account and a liability account. You will notice that asset accounts primarily hold a balance on the left of the t-account. Conversely, liability accounts hold a balance on the right. This is because asset accounts hold a debit balance while liability accounts maintain a credit balance. Building on this example, we can look at how a transaction would affect an asset account and liability account. Consider a transaction where the company purchases $1,000 of equipment on credit. This would affect the above t-accounts like so:

As you can see, the equipment account is an asset account so the balance is depicted on the left as a debit balance. Conversely, the accounts payable account is a liability account so the balance is shown on the right. Using t-accounts is a great way to understand and keep track of journal entries! Use CFI’s t-account template to make this even easier!

Thank you for reading CFI’s guide to T-Account Template. For more resources, check out our business templates library to download numerous free Excel modeling, PowerPoint presentations, and Word document templates.

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

Launch CFI’s Excel Crash Course now to take your career to the next level and move up the ladder!

CFI is a global provider of financial modeling courses and of the FMVA Certification. CFI’s mission is to help all professionals improve their technical skills. If you are a student or looking for a career change, the CFI website has many free resources to help you jumpstart your Career in Finance. If you are seeking to improve your technical skills, check out some of our most popular courses. Below are some additional resources for you to further explore:

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.