Get Certified for

Business Intelligence (BIDA®)

Develop analytical superpowers by learning how to use programming and data analytics tools such as VBA, Python, Tableau, Power BI, Power Query, and more.

A Microsoft-owned business analytics service that offers a wide range of data visualization and data warehousing services

The tagline for Power BI, “Bring Your Data to Life,” very clearly demonstrates the purpose of the Microsoft-owned business analytics tool. Power BI is an assortment of several data analytics-based services and systems that primarily focuses on visualizing business data and making it more interactive for organizations.

Created by Microsoft, Power BI is a cloud-based service provider offering data visualization and data warehouse services aimed at making data more interactive for the user. The application includes a wide range of data analytics services such as data preparation, custom visualization, data discovery, data warehousing, data reporting, interactive data sharing, data organization, and many others.

Owing to its substantial popularity, Power BI is available across different usage platforms. Power BI Desktop is used to access the analytics tool using a Windows-based desktop. It can also be accessed online using Power BI online SaaS, which is the application’s online software service. In addition, it can also be accessed using Android and iOS devices using the Power BI applications developed for the purpose.

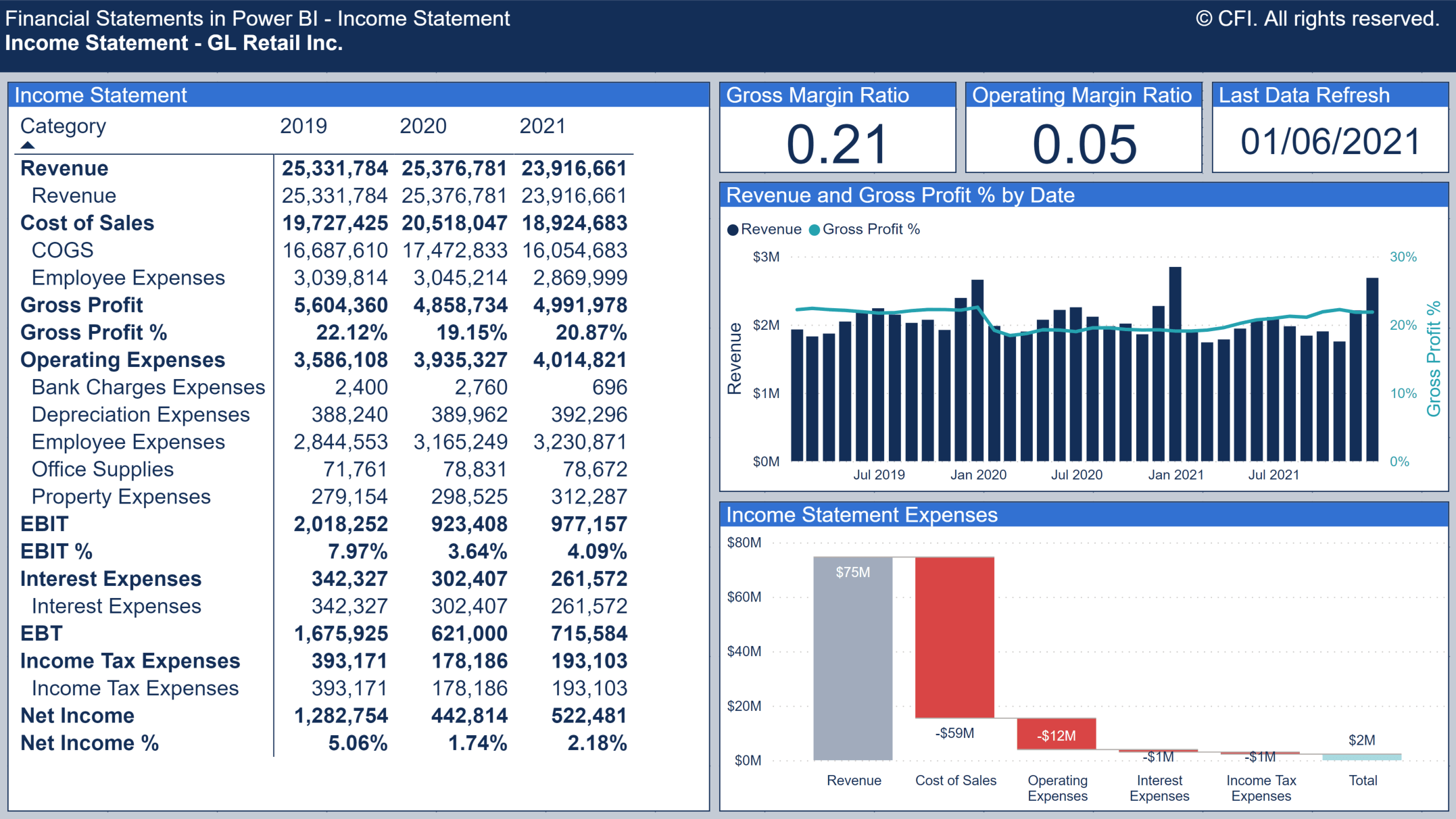

Power BI is a very efficient tool for business data organization. There are generally different kinds of limitations regarding the volume, nature, and complexity of data, and its reporting and organization across various data management mediums. However, this application offers exceptional financial data management services, with absolutely no limitations on the reporting of financial data, no matter how large the company is or how complex its data.

Power BI offers exceptional data projection systems. Financial projections are an integral part of a business’ operations, and several vital decisions are drawn essentially from financial projections. Hence, it is an integral part of any organization’s data management processes.

The application offers a data projections function called “what-if parameters” that create interactive data projections and are very efficient for comparison. It is a vital tool to draw up projection statements of any number and kind of assumptions.

Power BI comes with a built-in time intelligence feature. It also provides the ability to arrange data in accordance with different data dimensions and parameters. Using such features, it is very easy to spot data trends or data patterns over several years or across the market competition. They are very useful in drawing important conclusions about business operations and making important financial decisions about profitability, budgeting, business expenses, etc.

Power BI runs on powerful data analysis algorithms, which fuels the efficient working of the Quick Insights feature of the software. The tool provides data implications and draws various facts and conclusions from the dataset provided by the user. It is a very useful tool for a financial planner who would want some insight or draw conclusions from the financial statements for the year, and so on.

Power View is an essential feature of Power BI that allows generating interactive charts, graphs, and data maps. It helps generate visually interactive charts and graphs from the financial dataset and consolidating that information to draw conclusions and make important financial decisions.

Power BI is a collaborative platform, i.e., it is easily shareable and accessible across different users, while, at the same time, offering high security and protective measures. Hence, the finance department of the business or financial management teams of projects can collaborate. They can work together in sharing financial datasets, publishing financial reports and dashboards, exchanging vital data conclusions, and working collaboratively and efficiently.

The aforementioned uses of Power BI serve the purpose of financial data management and analysis exceptionally well. However, Power BI is not limited to just such uses; it offers a wide array of services for data management. It is considered an integral tool of financial management for large businesses and corporations, where financial data is in large numbers and is much higher in complexity.

To learn more about the dashboarding tool, check out CFI’s Power BI Fundamentals course! Learn more about telling meaningful stories with data, organizing and manipulating large and complex datasets, and creating powerful dashboards.

To keep advancing your career, the additional CFI resources below will be useful: