Corporate Finance Institute (CFI) is the global leader in online finance education, trusted by millions of professionals and organizations worldwide. Our expert-led courses and industry-recognized certifications equip professionals with the practical skills and knowledge needed to succeed in their careers.

Delivering the Finance Skills and Tools to Succeed

2M+

Professionals Worldwide

5,000+

On-Demand Lessons

200+

Courses

Strongly recommend to everyone who…

Strongly recommend to everyone who wants to receive new careers opportunities and enhance their knowledge in finance. CFI FMVA is perfect opportunity for everyone to obtain neccessary and strong background in financial modeling and valuation of…

AP

Excellent Course!!!

This course was very detailed and structured. I would definitely recommend this Certification for any budding Financial Analyst.

The program fully performs what it promises

I believe the program fully performs what it promises, bridging the gap between work and higher education. For me it means an added value that I cannot describe in words. The program focuses on technical knowledge,…

Excellent Finance Education

CFI delivers an outstanding online education for any aspiring finance professional. The well-arranged dashboard, the top-notch produced video lectures, interactive exercises, and quizzes, keep the participant engaged and motivated throughout the whole program. The CFI programs…

I am very satisfied with the FMVA Course

I am very satisfied with the FMVA certification, now I am able to build a 3 statements model from scratch. I know how to build an adavanced financial modeling,make a DCF Analysis (Discount cash flow analysis).How…

Excellent courses, well worthy of all my input

Before starting the CFI courses, I have zero financial background, but I know I love mathematics, I believe in my reasoning and analytical skills. So I went forward to take all the fundamental courses before start…

JY

Who We Are

Our History

-

2016CFI founded

-

2017Financial Modeling & Valuation Analyst (FMVA®) was launched

-

2019LSG acquired by CFI

-

2020

-

2020Over 1 million students joined CFI

-

2021Productivity software Macabacus joins the CFI family

-

2021Commercial Real Estate Finance Specialization was launched

-

2021Business Intelligence & Data Analyst (BIDA®) was launched

-

2022

-

2023Environmental Social & Governance Specialization was launched

-

2023FinTech Industry Professional (FTIP®) was launched

-

2023Cryptocurrencies and Digital Assets Specialization was launched

-

2023Business Intelligence Analyst Specialization was launched

-

2023Data Science Analyst Specialization was launched

-

2023Leadership Effectiveness Certificate Program was launched

-

2023Data Analysis in Excel Specialization was launched

-

2024Over 2 million students joined CFI

-

2024

-

2025

-

2025London Institute of Banking & Finance (LIBF) accredits FMVA, CBCA, CMSA, BIDA, FPWMP, FTIP Certification programs

What we do

We believe that anyone with the ambition to have a rewarding career in finance can achieve success when equipped with the right skills, knowledge, and support.

As the largest online finance & banking training platform for individuals, we empower millions of finance and banking professionals worldwide to achieve their highest professional potential by providing the resources they need to advance their careers.

We aspire to provide meaningful value to every finance professional at each stage in their career journey.

Trusted by finance professionals at

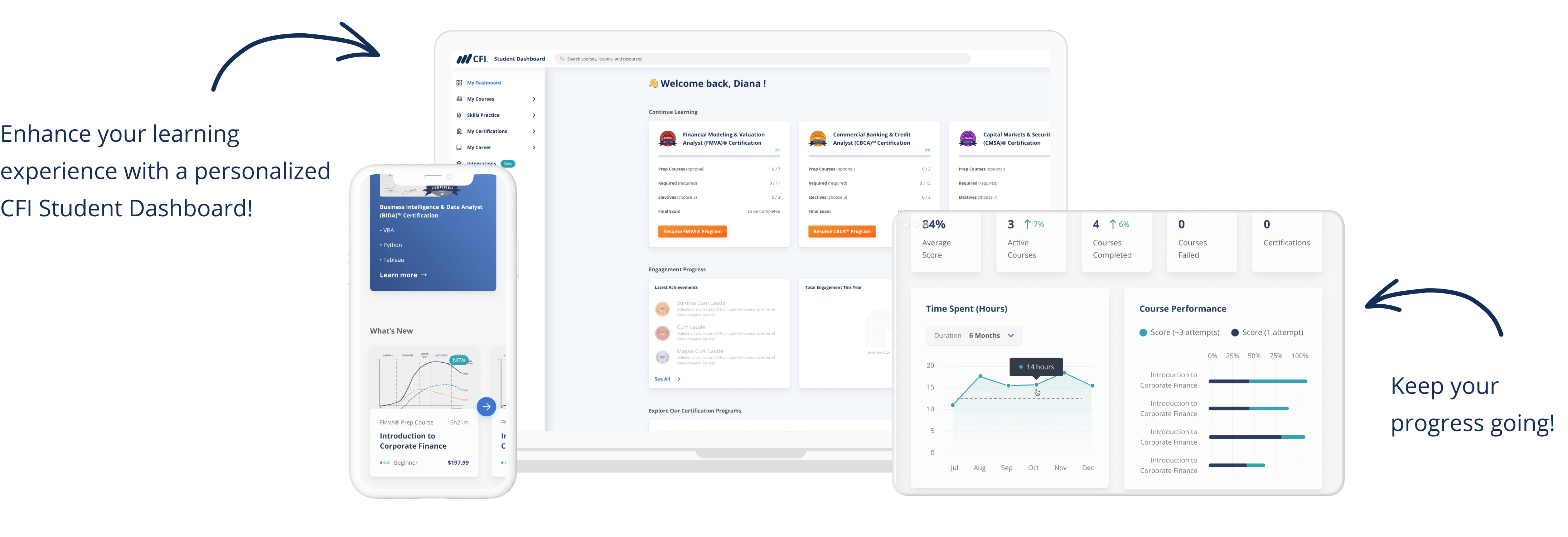

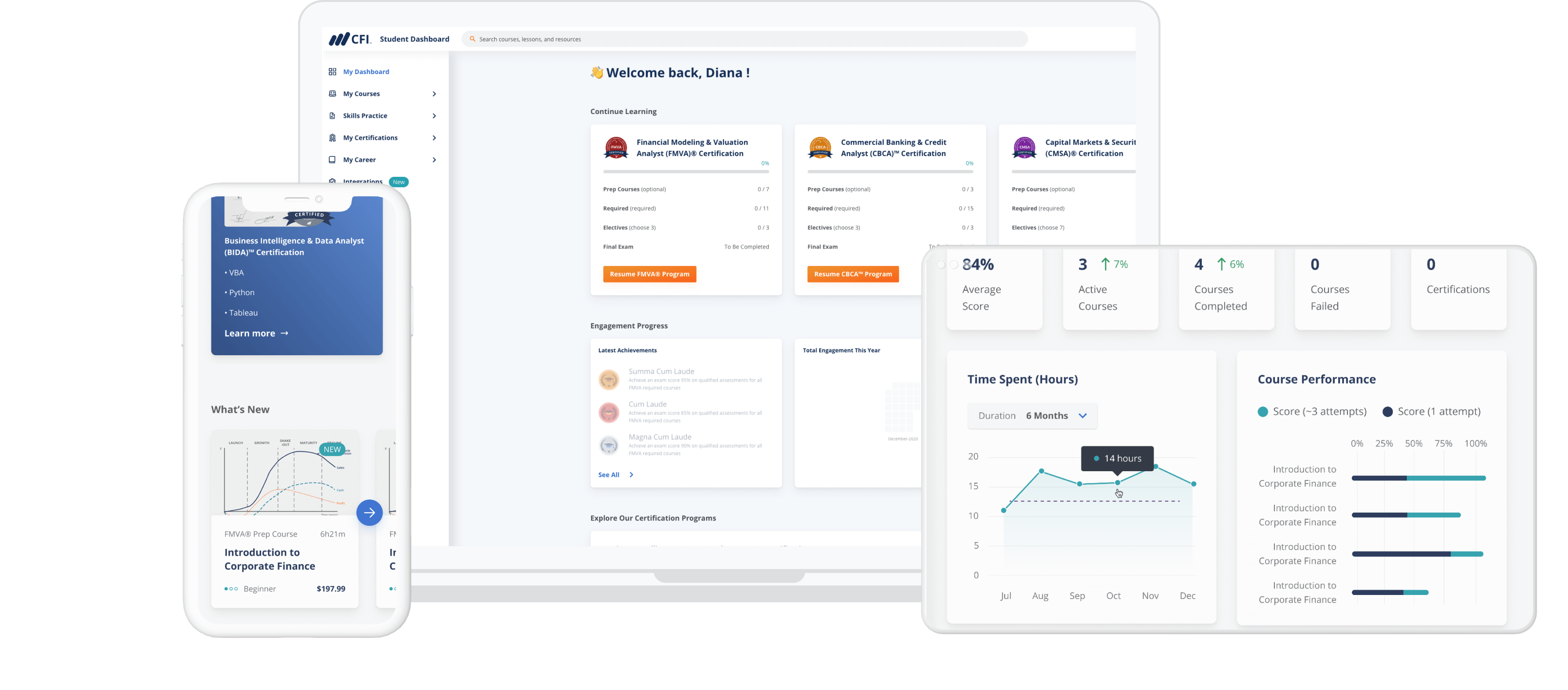

We provide practical, on-demand training for finance and banking professionals

CFI empowers professionals of any level with accredited certifications, hands-on lessons, tools, and resources created by experienced professionals who've worked and taught at leading finance and banking organizations across the world.

What CFI Students Have to Stay

In-Demand Certifications to Make Anyone a Go-To Expert

Trusted by 2 Million+ professionals worldwide.

"Abhishek Choudhry (CBCA)"

The best course to have in depth knowledge of Credit analysis. I would recommend this course to all who are in process to learn credit analysis.

"World-class skills set"

FMVA certification is challenging, robust and interesting that equips an accounting/finance professional with world-class skills set to advance their careers excel in their endeavors!

"Ajiboye Afeez (FMVA)"

The FMVA program is the best professional certification course I have ever done. The course is hands on experience with relevant industry examples.

"Andrii (CBCA)"

All courses of the CBCA program were provided in a very clear and easily understandable way. The lecturers were covering the subjects in a very effective manner. The design of the presentations looks very pleasant too.

"Anthony Santillanes (FMVA)"

I would absolutely recommend CFI’s training for anyone who’s looking to rapidly increase their ability to add value through a certification program.

"Daelan Subban (CBCA)"

The CBCA certification program offers an exceptional opportunity to explore financial theory and practice from the perspective of commercial lending and credit analysis.The course content is both comprehensive and easily digestible which make for a highly effective and efficient learning experience. Course instructors are excellent.

"David Kamenya (FMVA)"

CFI’s FMVA is the epitome of practical financial analysis and with it, you do not need years of practice to know the content. You are fully baked by the time you finish the course.