Overview

DCF Valuation Modeling Course Overview

DCF Valuation is one of the most common valuation techniques used in modern finance today. This technique is flexible in that it can be used for very early-stage growth companies as well as established companies operating in more mature industries. Although DCF Valuation is one of the soundest valuation techniques, errors in DCF models are actually quite common. Finance professionals often make mistakes related to the calculation and pairing of the company’s cash flows and its discount rate. Errors related to the timing of cash flows or the valuation date are also quite common. Finally, many struggle with the right level of detail for income tax calculations and fail to correctly break out the current and deferred taxes in both levered and unlevered income tax schedules.

DCF Valuation Modeling Learning Objectives

Upon completing this course, you will be able to:

- Understand how DCF Valuation compares to Comparable Trading Analysis and Precedent Transaction Analysis and the pros and cons of each valuation technique.

- Review the importance of upfront model design and the best layout for a DCF Valuation Model, which has been optimized for presentation and printing.

- Discuss common errors made with income taxes and the need for both a levered and unlevered income tax schedule in the model.

- Understand the importance of pairing the right cash flows (UFCF) with the correct discount rate (WACC) and review the steps for calculating each of these in detail.

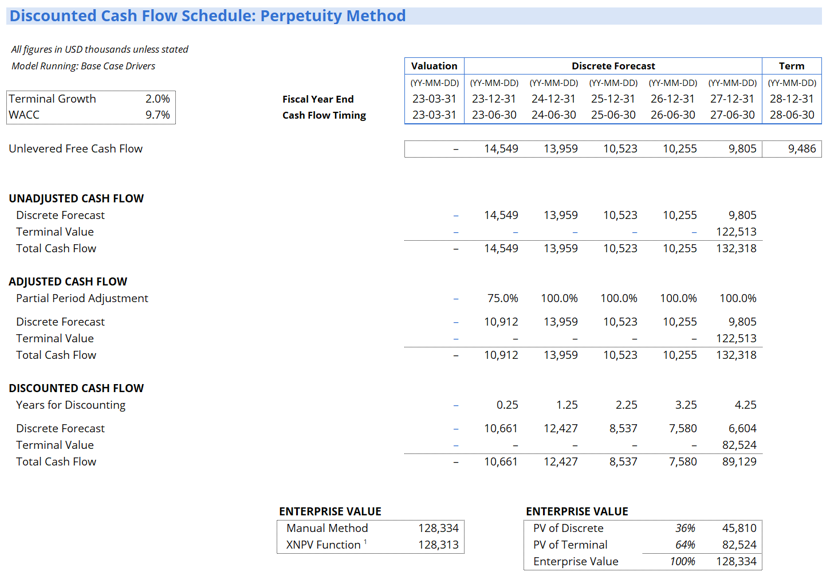

- Build separate schedules for both the perpetuity method and the multiple method for calculating the terminal value and discuss common errors related to timing.

- Design and build a dashboard for stakeholders using one and two-dimensional data tables to illustrate the model’s sensitivity to critical valuation inputs.

Recommended Prerequisite Courses

These preparatory courses are optional, but we recommend you complete the stated prep course(s) or possess the equivalent knowledge prior to enrolling in this course:

Who Should Take This Course?

This course is most suitable for anyone working in valuation, including investment banking, equity research, private equity, and corporate development.

Prerequisite Courses

Recommended courses to complete before taking this course.

DCF Valuation Modeling

Level 3

4h 55min

100% online and self-paced

Field of Study: Finance

Start LearningWhat you'll learn

DCF Model Theory

Compact DCF Model

Valuation Techniques

[Optional] Macabacus

Tax Schedules

Other Inputs

DCF Schedule

Qualified Assessment

This Course is Part of the Following Programs

Why stop here? Expand your skills and show your expertise with the professional certifications, specializations, and CPE credits you’re already on your way to earning.

Financial Modeling & Valuation Analyst (FMVA®) Certification

- Skills Learned Financial modeling and valuation, sensitivity analysis, strategy

- Career Prep Investment banking and equity research, FP&A, corporate development

Investment Banking & Private Equity Modeling Specialization

- Skills You’ll Gain Accounting, Advanced Financial Modeling, Excel, Financial Statement Analysis, Forecasting, Valuation, and more.

- Great For Investment Banking, Private Equity, Equity Research, and more