Overview

Leveraged Buyout LBO Modeling Course Overview

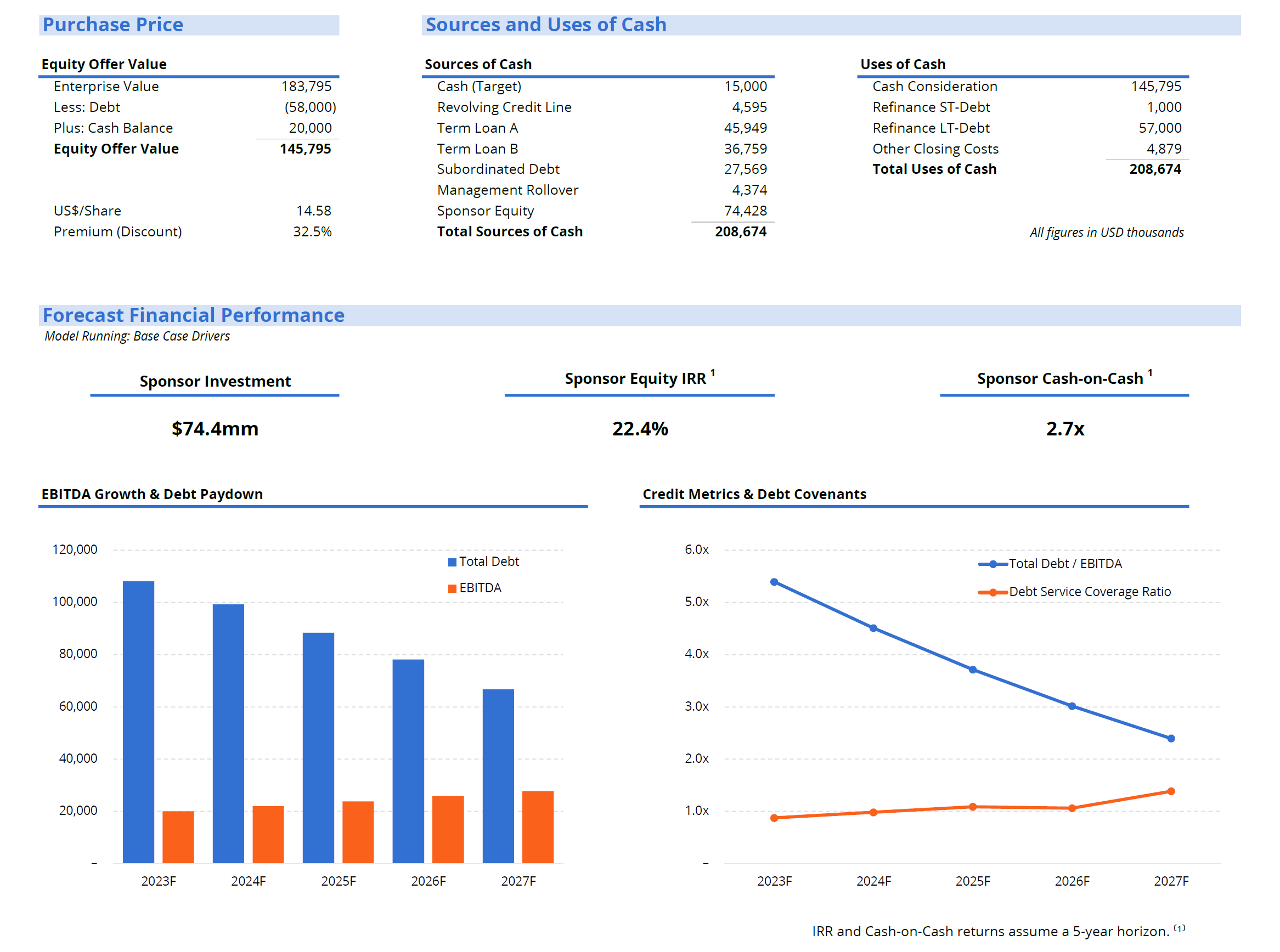

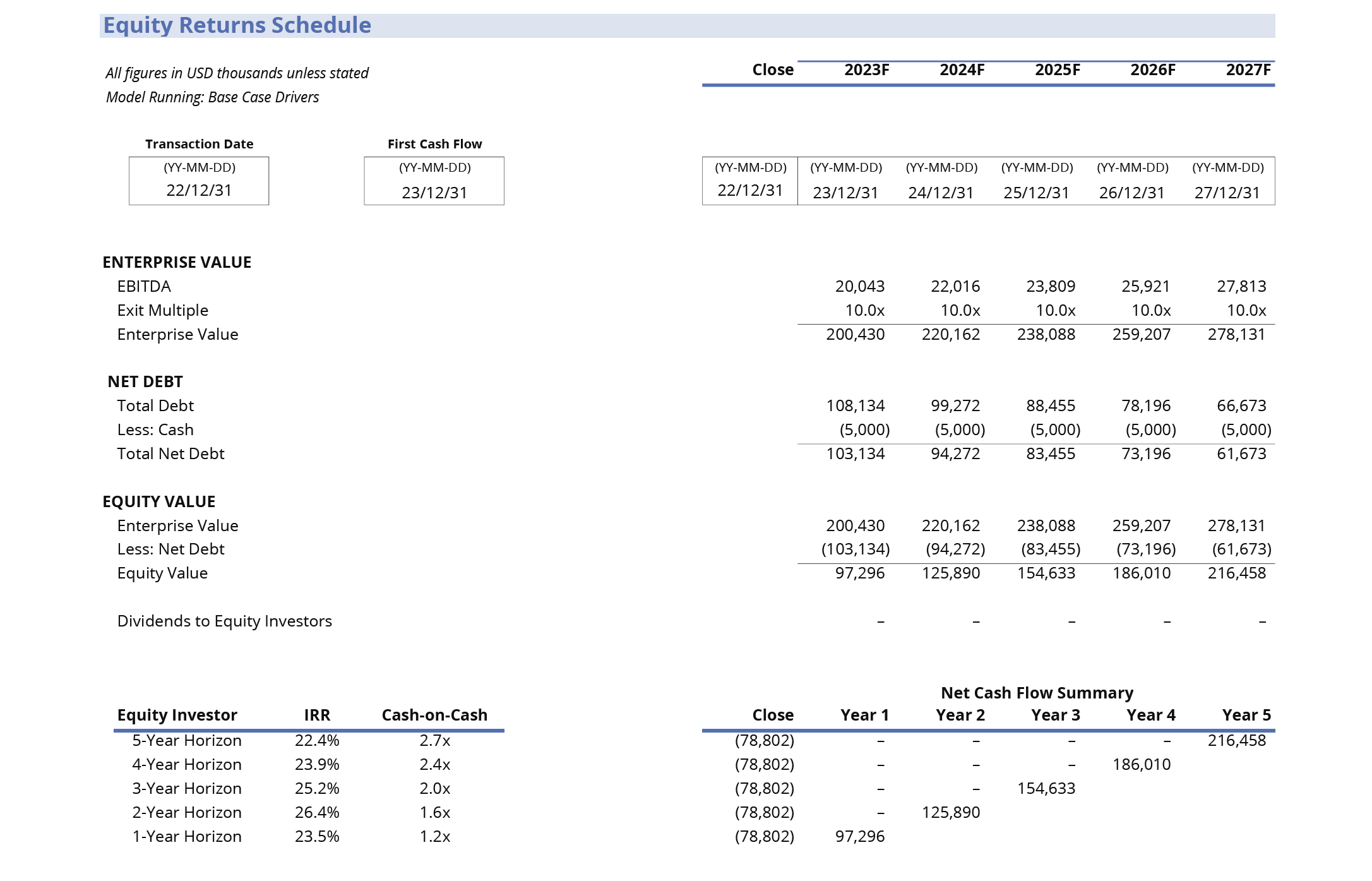

A leveraged buyout model – or LBO – is one of the most common models built at investment banks and private equity firms. This advanced class covers modeling best practices, creating multiple scenarios for assumptions, modeling the income statement and cash flow statement, as well as a complex capital structure. Additionally, we cover the calculation of IRR and cash-on-cash returns, credit metrics and covenants, error checks, and a dashboard with multiple types of charts and sensitivity analysis.

Leveraged Buyout LBO Modeling Learning Objectives

By the end of the course, you should be able to:- Define a leveraged buyout (LBO) and build a detailed LBO model.

- Identify the characteristics of good candidates for LBO transactions.

- Examine a number of typical LBO exit strategies used by private equity firms.

- Outline the typical capital structure of an LBO transaction in terms of leverage and types of capital.

- Explain the characteristics of each piece of capital and its position and priority in the capital stack.

- Construct a full LBO model and evaluate the merits of the transaction by examining the equity returns.

Who Should Take this Leveraged Buyout LBO Modeling Course?

This LBO modeling course is most suitable for professionals working in investment banking and private equity, although it may also be useful for professionals in corporate development or other areas of finance.

Recommended Prep Courses

These preparatory courses are optional, but we recommend you complete the stated prep course(s) or possess the equivalent knowledge prior to enrolling in this course:Prerequisite Courses

Recommended courses to complete before taking this course.

Prerequisite Skills

Recommended skills to have before taking this course.

- Excel

Leveraged Buyout (LBO) Modeling

Led by

Jeff Schmidt

Level 5

4h 33min

100% online and self-paced

Field of Study: Finance

Start LearningWhat you'll learn

Lesson

Multimedia

Exams

Files

Output Schedules - Equity Returns

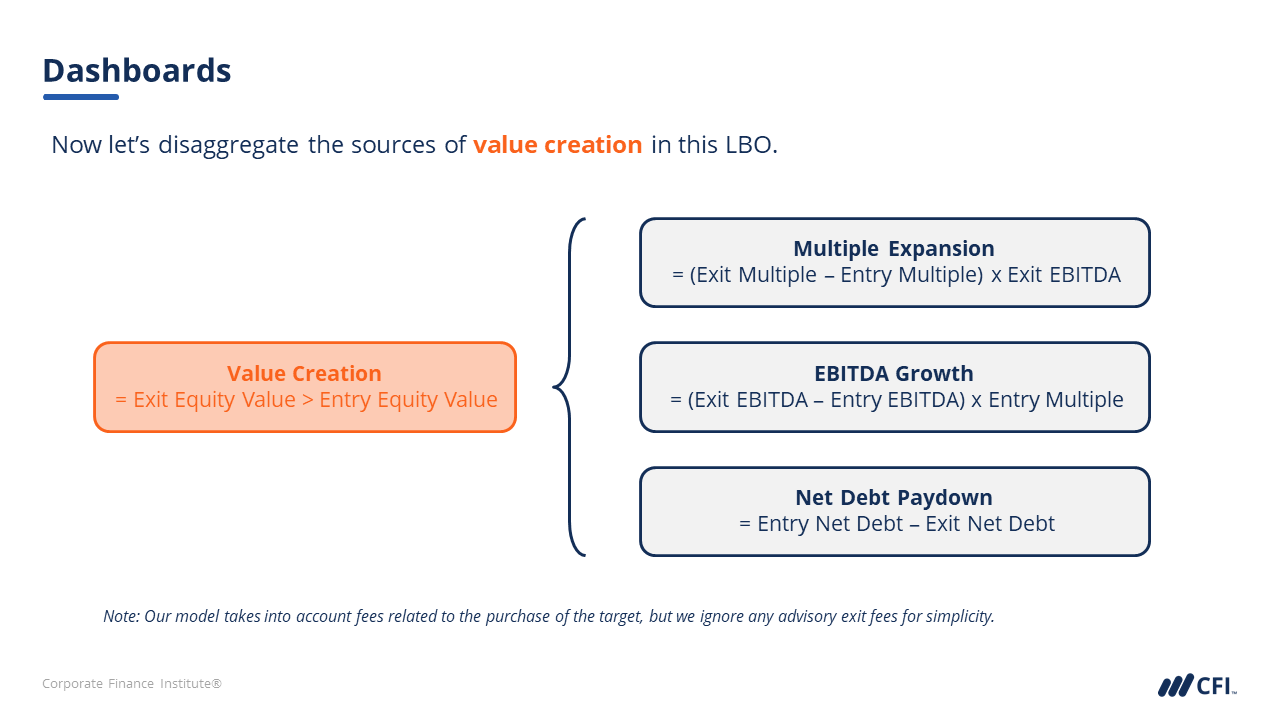

Dashboards

Model Circularity & Model Checks

Model Review

Model Review Using Native Excel Tools

[Optional] Model Review Using Macabacus Tools

Excel Trace Precedents and Trace Dependents

[Optional] Macabacus Precedents and Dependents

Find the Errors

[Optional] Macabacus Visualization Tools

Flexing the Model

Interactive Exercise 13

Download the Completed Full LBO Model

Course Summary

Qualified Assessment

This Course is Part of the Following Programs

Why stop here? Expand your skills and show your expertise with the professional certifications, specializations, and CPE credits you’re already on your way to earning.

Investment Banking & Private Equity Modeling Specialization

- Skills You’ll Gain Accounting, Advanced Financial Modeling, Excel, Financial Statement Analysis, Forecasting, Valuation, and more.

- Great For Investment Banking, Private Equity, Equity Research, and more

What Our Members Say

Awesome LBO Model!

Awesome LBO model with very well explained definitions and use of it. Great exercises to build the model! Delbert Adivnovak

Amazing learning experience

Very clear step by step training course on LBO models. Highly recommended! FAUSTO SCIABICA

Excellent stuff!

Taught me from ground up all I needed to know about Leverage Buy Outs and modelling them as well!....Very glad I took this!.. Zahid Sameer

lbo modelling

great course a real inspiration Marko Maschek

Frequently Asked Questions

If you haven’t found your answer from our FAQ, please send us a message.

If you haven’t found your answer from our FAQ, please send us a message.