Overview

Widgets Inc. – Adjusting a Business Owner’s Net Worth Overview

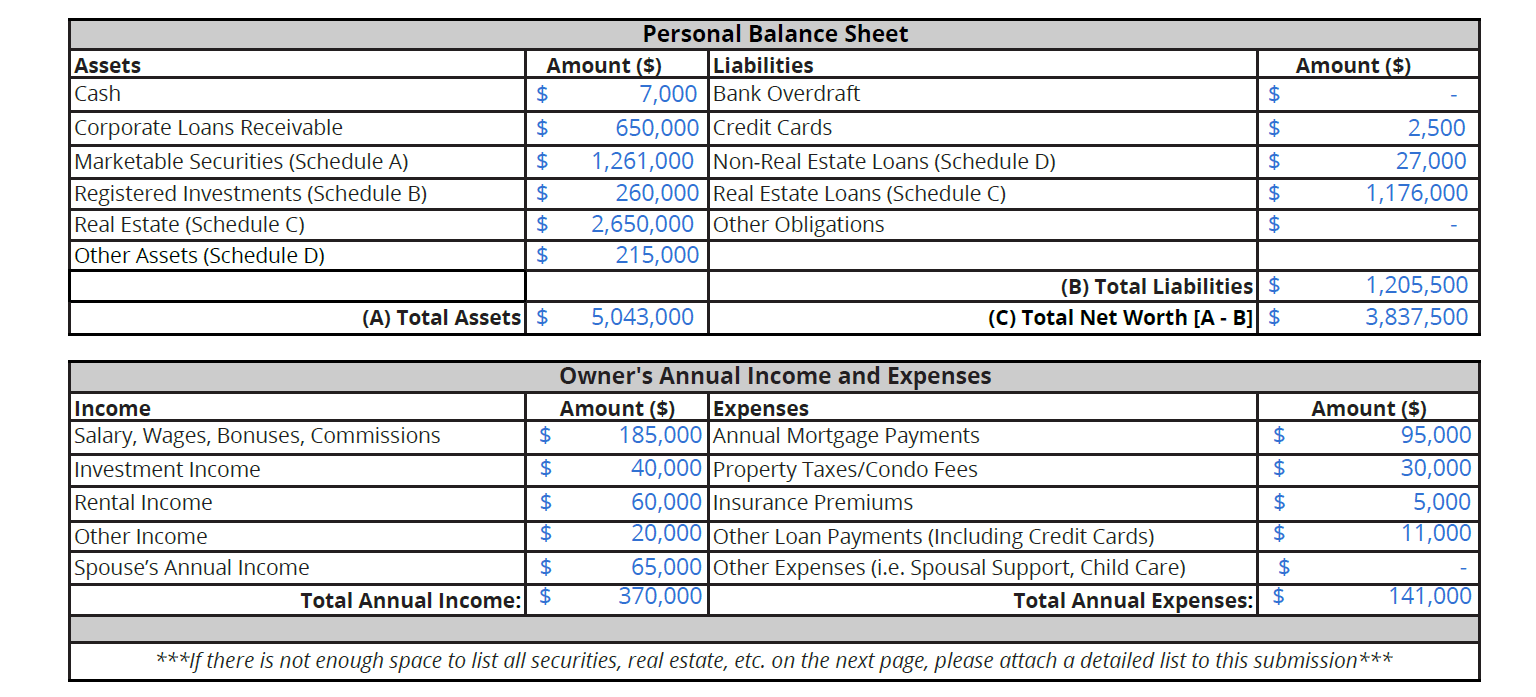

Understanding a business owner’s personal financial situation is a critical skill in managing risk for commercial lenders. In this practice lab, we’ll step into the shoes of an SME lender and seek to holistically understand a business owner’s personal finances (within the context of a prospective borrowing request). We’ll dig through the company’s financial results and the owner’s personal net worth statement to try and identify potential risks.

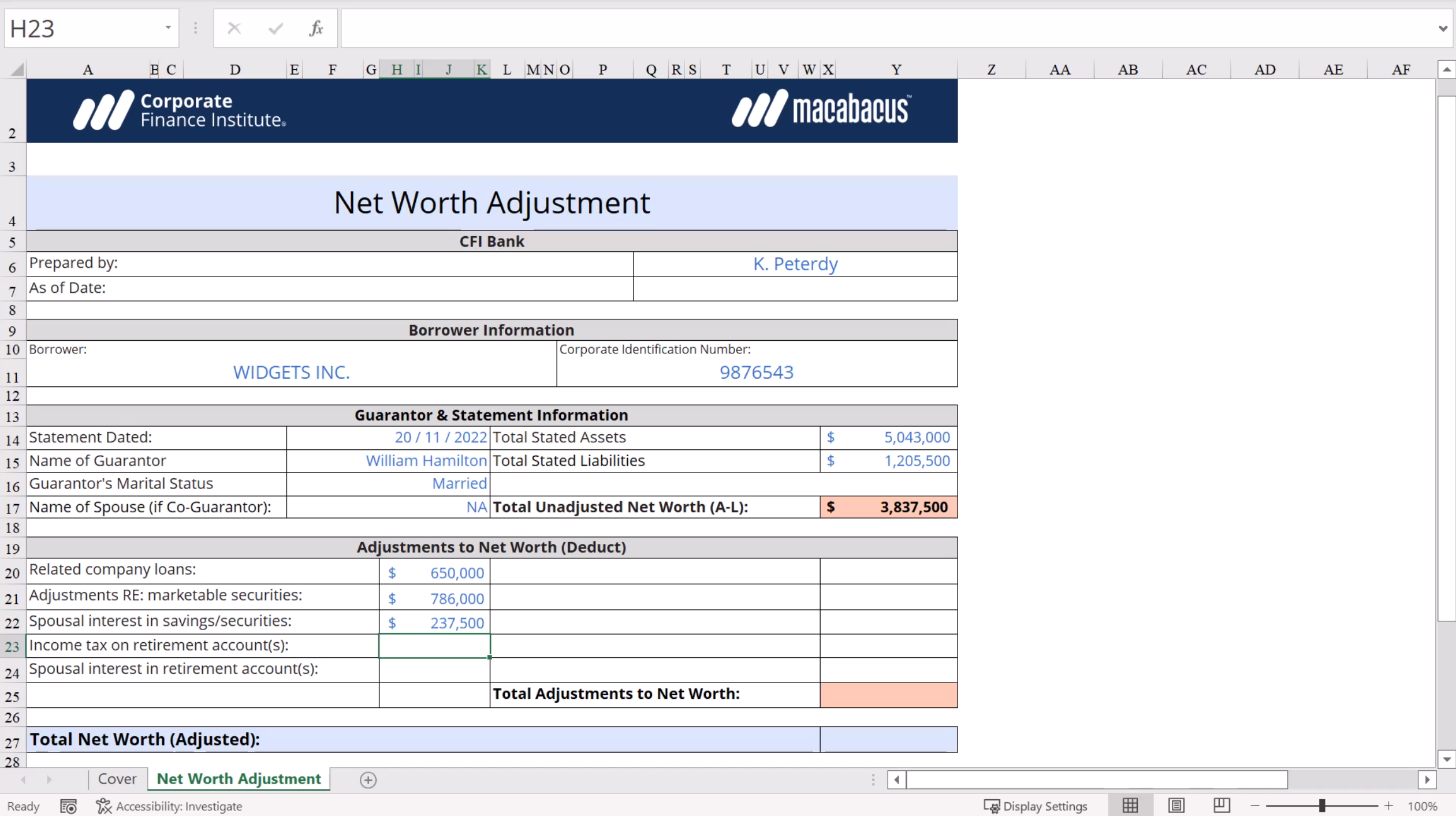

Next, we’ll work through an adjustment template, line-by-line, in order to arrive at a responsible set of insights and a prudent set of adjustments.

Widgets Inc. – Adjusting a Business Owner’s Net Worth Learning Objectives

Upon completing this practice lab, participants will be able to:- Recognize how a business owner’s corporate cash flow and personal earnings are intertwined.

- Quickly identify risks / potential red flags in a business owner’s personal financial situation.

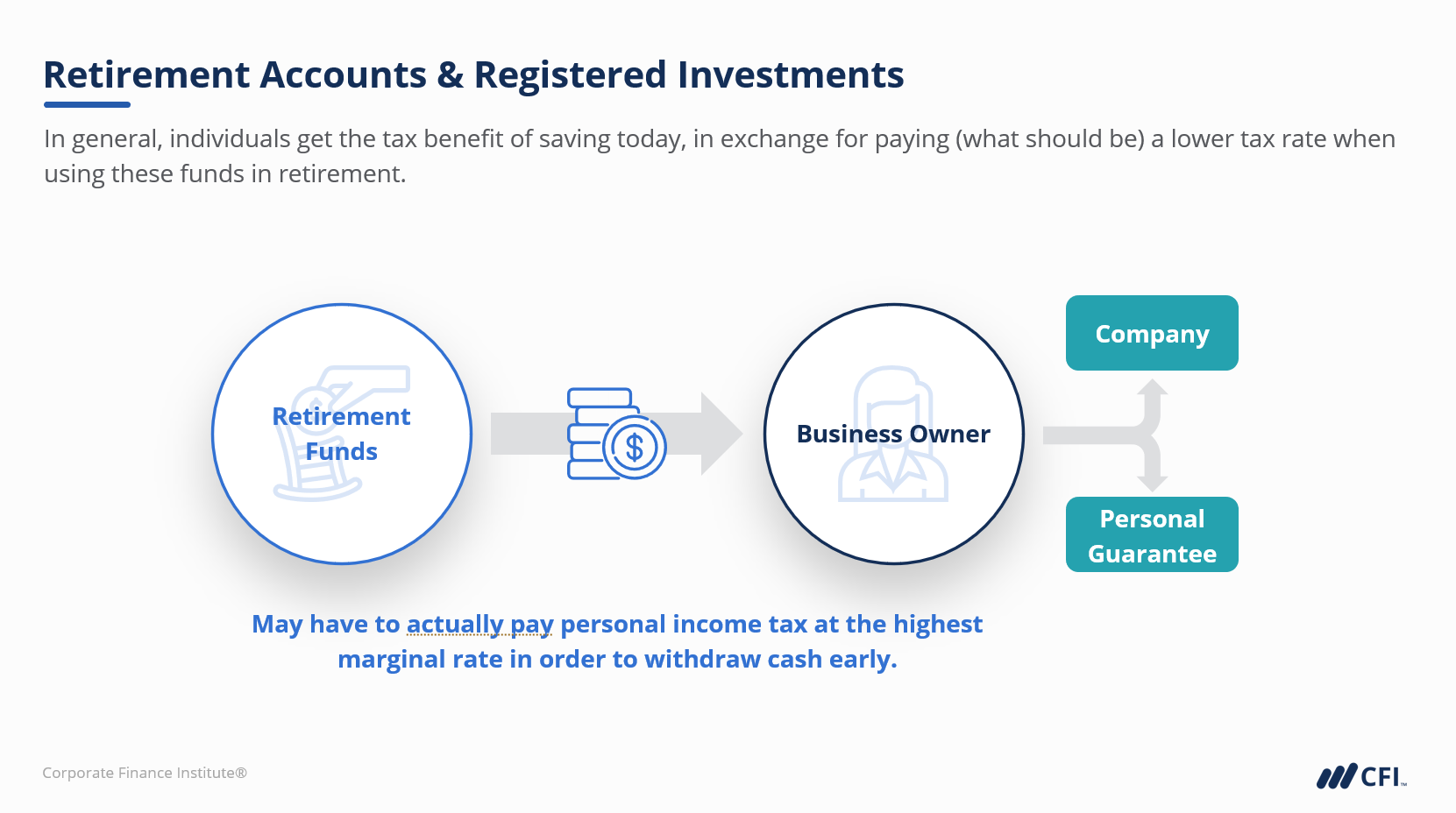

- Make appropriate adjustments to reflect an owner’s actual ability to tap into liquid, unencumbered personal assets to inject cash into the corporation or to make whole on a personal guarantee.

Who Should Take This Lab?

This lab is a great building block for early career business and commercial bankers, including relationship managers, analysts, and adjudicators. Other credit professionals like asset-based lenders, commercial real estate lenders, equipment finance professionals, and commercial loan brokers will also get enormous value.

Prerequisite Courses

Recommended courses to complete before taking this course.

Prerequisite Skills

Recommended skills to have before taking this course.

- Financial accounting

- Critical thinking

Widgets Inc. - Adjusting a Business Owner’s Net Worth

Level 2

42min

100% online and self-paced

Field of Study: Finance

Start LearningWhat you'll learn

Analysis

Alternative Scenario & Summary

Qualified Assessment

This Course is Part of the Following Programs

Why stop here? Expand your skills and show your expertise with the professional certifications, specializations, and CPE credits you’re already on your way to earning.

Commercial Banking & Credit Analyst (CBCA®) Certification

- Skills Learned Financial Analysis, Credit Structuring, Risk Management

- Career Prep Commercial Banking, Credit Analyst, Private Lending