Overview

Boss Brewing Inc. – Connecting Capital Structure & Credit Structure

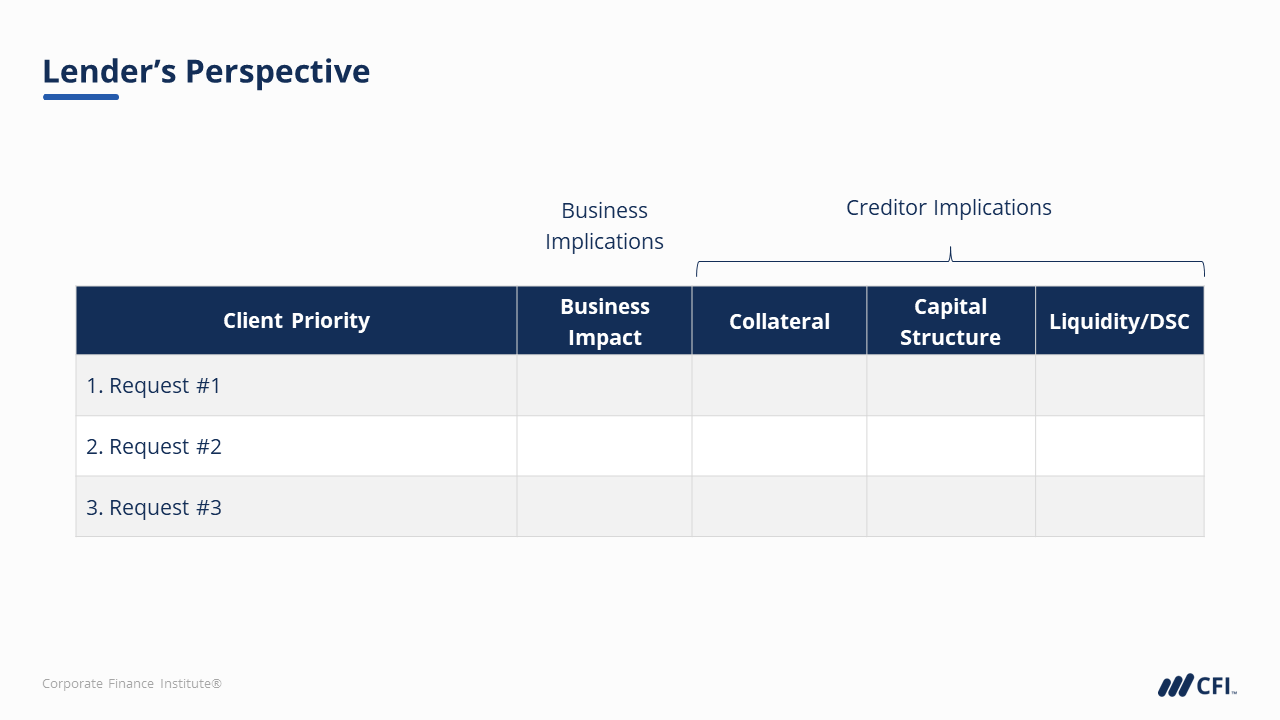

Understanding a borrowing request and its associated risks is a critical skill for commercial lenders. In this practice lab, we’ll step into the shoes of a SME lender to analyze a borrowing request from both the lender and borrower’s perspectives, with an eye to understanding how the proposed credit structure may impact the client’s capital structure and other important financial ratios.

We’ll analyze the client’s financial statements and look to identify how their priorities may differ from those of the lender, before working towards a proposal that will satisfy the needs of both parties.

Boss Brewing Inc. – Learning Objectives

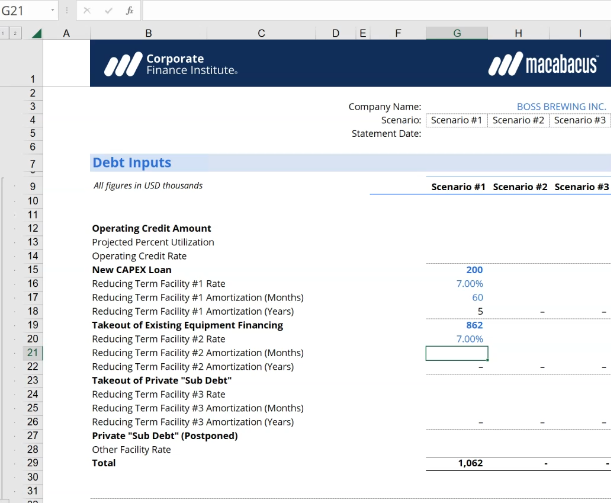

Upon completing this practice lab, participants will be able to:- Appreciate how dramatically the intended purpose of loan proceeds can impact a borrower’s capital structure.

- Compare multiple borrowing scenarios and calculate key lending ratios.

- Think critically about how credit structure and capital structure are connected.

- Make appropriate recommendations around a credit structure that satisfies both client needs and bank guidelines.

Who Should Take This Lab?

This lab is a great building block for early career business and commercial bankers, including relationship managers, analysts, and adjudicators. Other credit professionals like asset-based lenders, commercial real estate lenders, equipment finance professionals, and commercial loan brokers will also get enormous value.Prerequisite Courses

Recommended courses to complete before taking this course.

Boss Brewing Inc. – Connecting Capital Structure & Credit Structure

Level 3

55min

100% online and self-paced

Field of Study: Finance

Start LearningWhat you'll learn

Introduction

Priority List

Boss Brewing Scenarios

Sources and Uses of Funds

This Course is Part of the Following Programs

Why stop here? Expand your skills and show your expertise with the professional certifications, specializations, and CPE credits you’re already on your way to earning.

Commercial Banking & Credit Analyst (CBCA®) Certification

- Skills Learned Financial Analysis, Credit Structuring, Risk Management

- Career Prep Commercial Banking, Credit Analyst, Private Lending