Overview

Introduction to InsurTech Course Overview

InsurTech, or insurance technology, is disrupting the traditional insurance industry by leveraging technology to make the insurance process more efficient and cost-effective. In this course, we’ll first define what InsurTech is and its importance before exploring the history and evolution of insurance distribution. We’ll then identify the main areas of InsurTech, guided by technological and economic trends, and how they differ from traditional practices. Next, we’ll examine some of the InsurTech innovations that are impacting pricing, underwriting, and claims, including data science, telematics, drones, and robotics. We’ll also look at important metrics such as frequency, severity, loss ratio, and combined ratio. Finally, we’ll explore the future of InsurTech, including embedded insurance, changing customer expectations, and diversifying risk through new products and services.

Introduction to InsurTech Learning Objectives

Upon completing this course, you will be able to:- Define what InsurTech is and its importance

- Explain the history and evolution of insurance

- Identify the main areas in InsurTech and how they differ from traditional practices

- Identify InsurTech innovations and impact to pricing, underwriting, and claims

- Explain the future of InsurTech

Who Should Take This Course?

This is a beginner-level course suitable for insurance professionals, data analysts, and aspiring entrepreneurs who are interested in leveraging technology to transform the traditional insurance industry.

Prerequisite Courses

Recommended courses to complete before taking this course.

Introduction to InsurTech

Led by

Matt Christopher

Level 1

1h 4min

100% online and self-paced

Field of Study: Specialized Knowledge

Start LearningWhat you'll learn

Lesson

Multimedia

Exams

Files

Overview of InsurTech

What Is InsurTech

Free Preview

The InsurTech Explosion

Free Preview

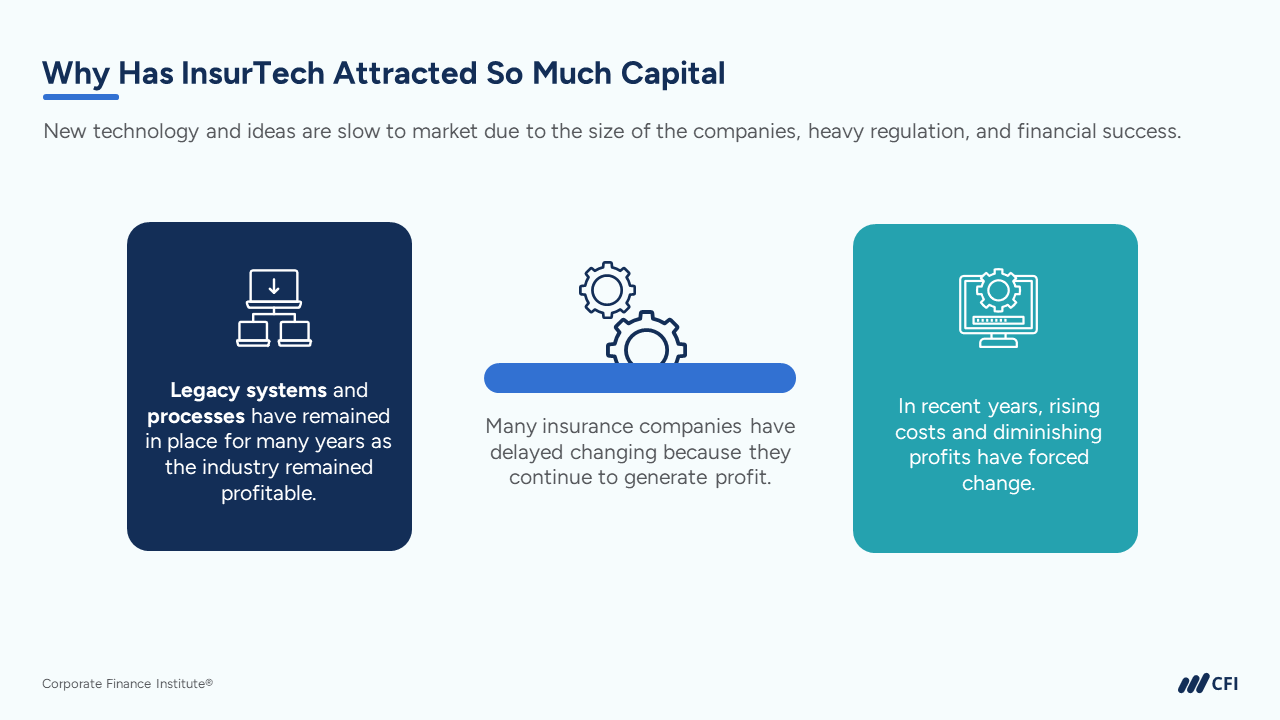

Why Has InsurTech Attracted So Much Capital

Free Preview

Interactive Exercise 1

Free Preview

Evolution of Insurance Distribution (1920s-1930s)

Free Preview

Evolution of Insurance Distribution (1990s – 2000s)

Evolution of Insurance Distribution Today

Interactive Exercise 2

Application Programming Interface (API)

Barriers to Entry

Managing General Agency

Interactive Exercise 3

InsurTech Innovations and Impact

Frequency

Severity

Impact of Pricing

Impact to Pricing – Example

Impact to Pricing – Risk Profile

Interactive Exercise 6

Impact to Pricing – Telematics

Impact to Underwriting

Impact to Underwriting – Acquisition

Impact to Underwriting – Managing the Book

Interactive Exercise 7

Loss Ratio

Combined Ratio

Understanding Loss Ratio and Combined Ratio

Impact to Claims

Impact to Claims - Example

Impact to Claims – AI Estimating

Interactive Exercise 8

Impact to Claims – Drones & Robotics

Impact to Claims – Fraud Prevention

Impact to Claims – Video

Impact to Claims – Incident Detection

Interactive Exercise 9

Impact to Claims – Roadside Assistance

Impact to Claims – Digital Payments

Loss Adjustment Expense

Interactive Exercise 10

Course Summary

Qualified Assessment

This Course is Part of the Following Programs

Why stop here? Expand your skills and show your expertise with the professional certifications, specializations, and CPE credits you’re already on your way to earning.

FinTech Industry Professional (FTIP®)

- Skills Learned Financial Technology Fundamentals, Data Science and Machine Learning, Cryptocurrencies and Blockchain

- Career Prep Data Science and Machine Learning, Data Analyst, Business Analyst, Software Developer

What Our Members Say

Very insightful course. I have no background in Insurance and how it works, but this course has enlightened me on the topic of insurance and InsurTech.

Onyedika Nwoji

Very Informative and well summarized

I totally loved this course! Rajalakshmi Arumugam

Strong Foundation

Must complete this course for understanding how InsureTech Works Suman Kumar

Insure tech introduction

Great content and presentation. Exam questions should be atleast 20. venugopal rajamanuri

Frequently Asked Questions

If you haven’t found your answer from our FAQ, please send us a message.

If you haven’t found your answer from our FAQ, please send us a message.