Overview

ESG Risk Management Course Overview

ESG has become THE ultimate test of management effectiveness in today’s business arena. Corporate finance teams around the world will face increasing pressures and expectations to guide their organizations through the litany of ESG risks, regulations, and requirements. This course equips you with the knowledge and tactics needed to navigate your organization through these risks and institutionalize a company-wide ESG risk management system. As finance teams become the “unsung heroes” of corporate transformations around the world, this course will give you the capabilities and confidence needed to lead your organization in the ‘age of ESG.’

ESG Risk Management Learning Objectives

Upon completing this course, you will be able to:- Explain why and how ESG issues present risks to a business

- Provide examples of both ESG risk management failures as well as best practices

- Identify and categorize risk types based on company context

- Describe the specific ESG risks facing financial service providers

- Execute the fundamentals of ESG risk management

Who Should Take This Course?

This course is essential for financial professionals, corporate leaders, sustainability experts, and policy makers aiming to navigate the evolving landscape of ESG risk management. It offers deep insights into identifying, categorizing, and mitigating ESG risks tailored to the specific needs and realities of various organizations. By mastering these skills, participants will be well-equipped to lead their organizations effectively in the age of ESG, ensuring sustainable, compliant, and resilient business practices.

Courses we recommend you take in advance

These prerequisite courses are optional, but we recommend you complete the stated prep course(s) or possess the equivalent knowledge prior to enrolling in this course:Prerequisite Courses

Recommended courses to complete before taking this course.

Prerequisite Skills

Recommended skills to have before taking this course.

- Critical thinking

ESG Risk Management

Led by

Noah Miller

Level 2

1h 19min

100% online and self-paced

Field of Study: Specialized Knowledge

Start LearningWhat you'll learn

Lesson

Multimedia

Exams

Files

Determining Material Issues & Associated Risks

The Implications for ESG Risk Exposure

The Fundamentals of ESG Risk Management

Review of Enterprise Risk Management Framework

Establish Risk Appetite

Identify Risks

Assess Risks

Respond to Risks

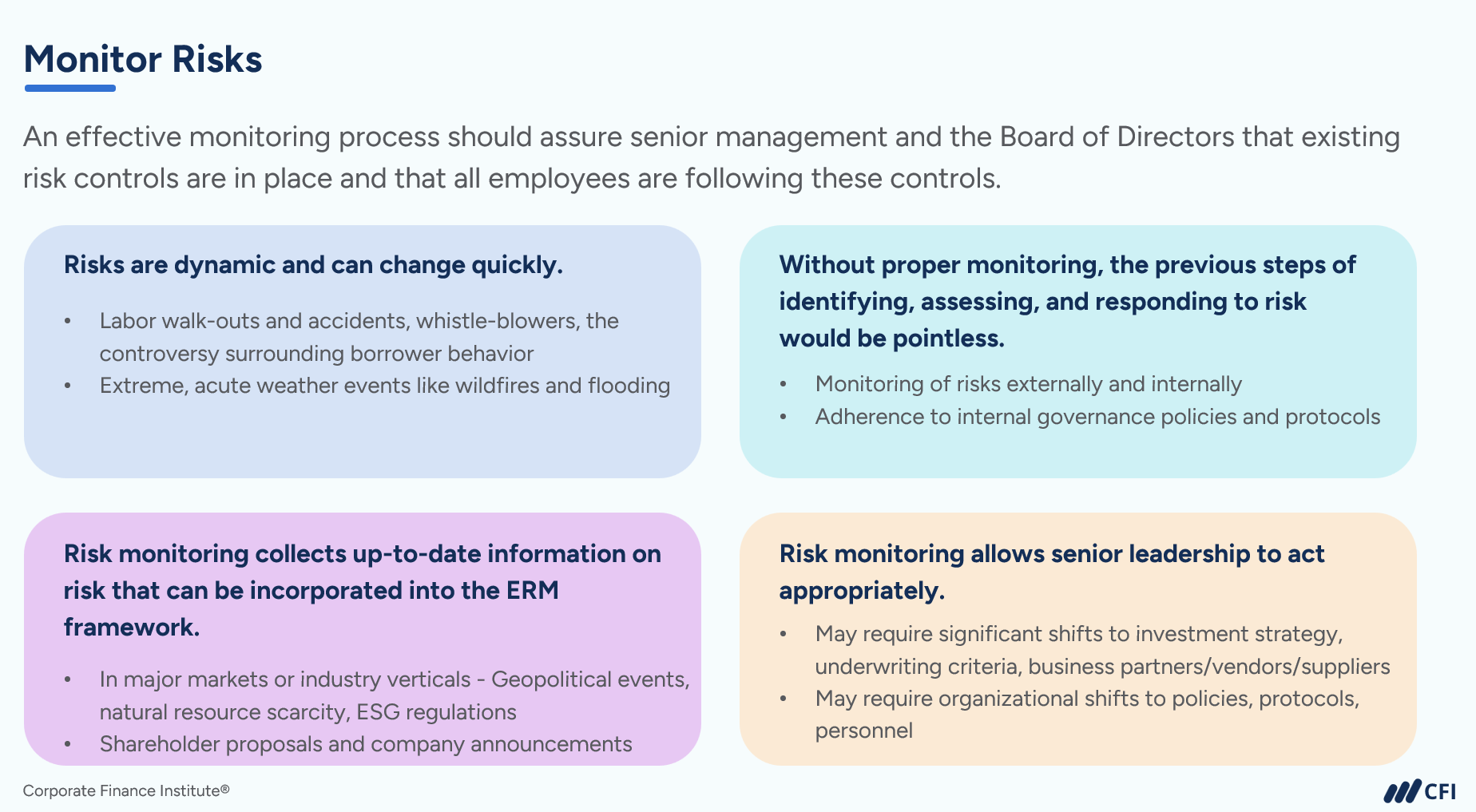

Monitor Risks

ESG Risk Management Best Practices

Examples of ESG Risk Management Best Practices

Citigroup’s Loan Portfolio Climate Risk Assessment

BMO’s E&S Risk Management Framework

HSBC’s Financed Emissions Measurement Methodology

The Future of ESG Risk Management

Interactive Exercise 3

Summary

Qualified Assessment

This Course is Part of the Following Programs

Why stop here? Expand your skills and show your expertise with the professional certifications, specializations, and CPE credits you’re already on your way to earning.

Environmental Social, and Governance Specialization

- Skills Learned ESG Analysis, ESG Integration, ESG Investing, ESG & Business Intelligence

- Career Prep Asset Management, Management Consulting, Business Analyst, Credit Analyst, Corporate Development, Senior Leadership

Risk Management Specialization

- Skills You’ll Gain Risk Identification, Regulatory Analysis, Risk Measurement, Risk Mitigation

- Great For: Market Risk Analyst, Credit Risk Analyst, Compliance Officer, consulting, Enterprise Risk Manager, Audit

What Our Members Say

Truly enhancing

This course is truly enhancing and worth for time & money Lee Anselmo Blackman

Excellent way to lean about ESG Risk

Good course, appropriate depth and length - I think this could be updated with some other bankused in examples e.g Triodos instead of HSBC Richard Green

Comprehensive detailed and full of valuable information

I enjoyed every lesson. Great content that explores both the risks and opportunities linked to evolving environments, societies, and economies. Linda Etuhole Nakasole

clear, lucid manner of delivery

Shanti Sunder

Frequently Asked Questions

If you haven’t found your answer from our FAQ, please send us a message.

If you haven’t found your answer from our FAQ, please send us a message.