Overview

Operational Risk Management in Banks Course Overview

Operational risk is a critical component of any comprehensive risk management framework. Operational failures can not only lead to large financial losses, but they can also lead to exceedingly damaging reputational harm. This course will give learners the skills and knowledge they need to navigate and apply effective operational risk frameworks, such as those set out by the Basel Committee on Banking Supervision.

Operational Risk Management in Banks Course Learning Objectives

Upon completing this course, you will be able to:- Define operational risk using the same language as banks and global banking regulators.

- Rank operational risk events based on frequency and impact.

- Give real-world examples from the financial services industry of different types of operational risk failures.

- Categorize operational risk events into categories based on the Basel framework.

Who Should Take This Course?

Finance professionals who want a career in Risk Management or specifically Operational Risk or Enterprise Risk Management.Courses we recommend you take in advance

The prerequisites are optional, but we recommend you complete these courses or possess the equivalent knowledge prior to enrolling in this course:Prerequisite Courses

Recommended courses to complete before taking this course.

Operational Risk Management in Banks

Led by

Ryan Spendelow

Level 3

1h 15min

100% online and self-paced

Field of Study: Finance

Start LearningWhat you'll learn

Lesson

Multimedia

Exams

Files

Understanding Operational Risk

Chapter Introduction

Free Preview

Operational Versus Other Types of Risk

Free Preview

Operational Risk Simulation

Free Preview

Operational Risk Simulation Poll

Frequency Versus Impact

Interactive Exercise 1

Operational Risk Ratings

People Processes Systems and External Events

Volkswagen Emissions Scandal Case Study

Interactive Exercise 2

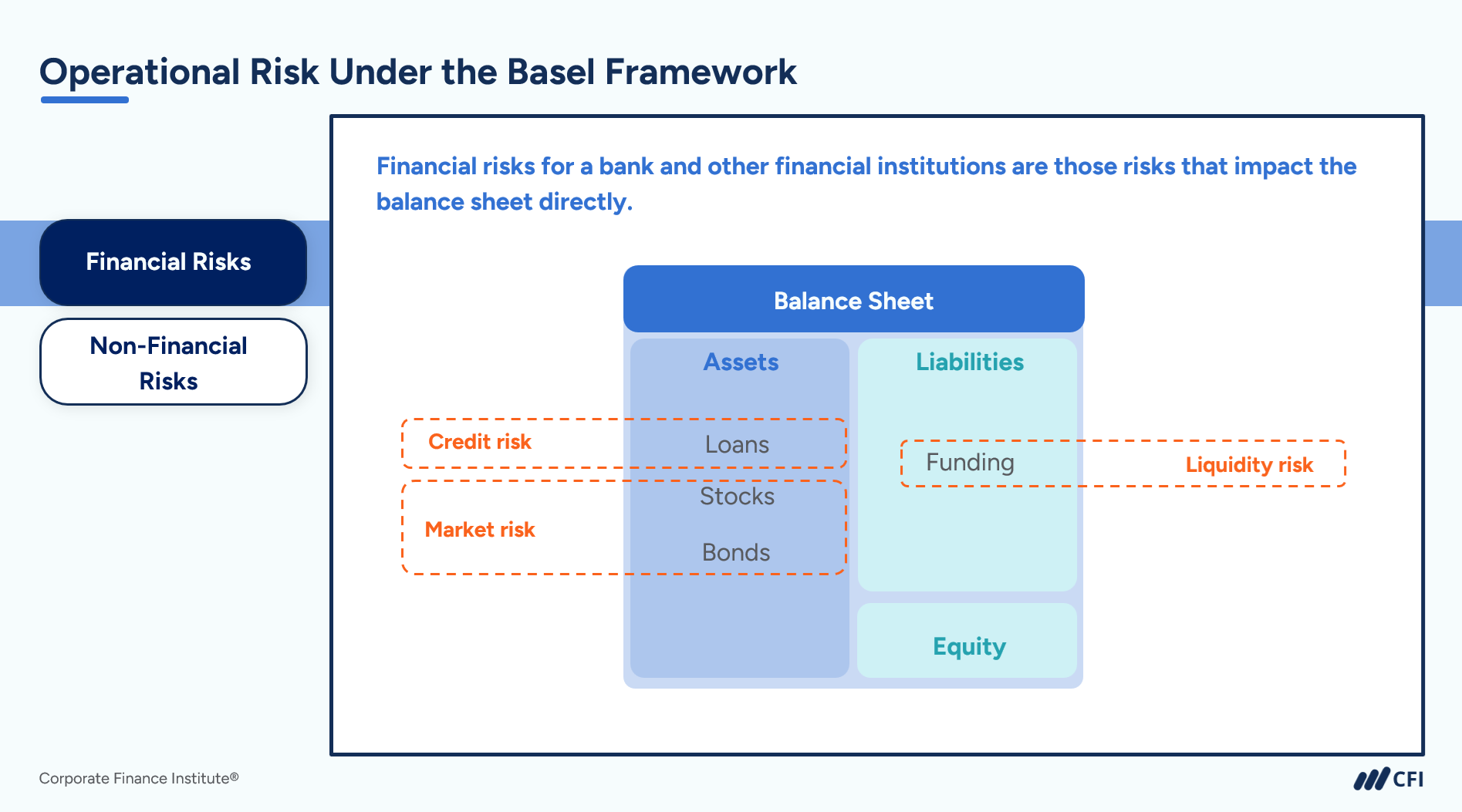

Operational Risk Under the Basel Framework

Categorizing Operational Risk

Chapter Introduction

The Seven Operational Risk Categories

Interactive Exercise 3

The FTX Fraud

Fraud in Financial Services

Interactive Exercise 4

Internal Fraud

Interactive Exercise 5

Capital One Data Breach

External Fraud

System Security – Data Breaches

Interactive Exercise 6

System Security – Ransomware Attacks

Interactive Exercise 7

Employment Practices and Workplace Safety

Interactive Exercise 8 - Poll

Clients, Products, and Business Practices

Interactive Exercise 9

Clients, Products, and Business Practices Subcategories

Damage to Physical Assets

Business Disruption and System Failures

Interactive Exercise 10

Interactive Exercise 11

Execution, Delivery, and Process Management

Interactive Exercise 12

Summary

Qualified Assessment

This Course is Part of the Following Programs

Why stop here? Expand your skills and show your expertise with the professional certifications, specializations, and CPE credits you’re already on your way to earning.

Risk Management Specialization

- Skills You’ll Gain Risk Identification, Regulatory Analysis, Risk Measurement, Risk Mitigation

- Great For: Market Risk Analyst, Credit Risk Analyst, Compliance Officer, consulting, Enterprise Risk Manager, Audit

What Our Members Say

Excellent practical approach

Great mix of practical and theoretical approaches to applying a course. Raul De Gracia Saraceni

Very good at refreshing Your Memory

As a double-degree financial and banking I might addd that the courses are very intuitive and refreshes the curiculum learnes, even in some instances it is more clearly presented in a more understandable way Daniel Budak

OPERATIONAL RISK MANAGEMENT IN BANKS

GOOD CONTENT AND GOOD DELIVERY. EXAM QUESTIONS ARE TOO FEW AND SIMPLE. SHOULD IMPROVE THE EXAM RIGOUR TO BRING CREDIBILITY TO THE CERTIFICATIONS. venugopal rajamanuri

Insightful learning on Operational Risk

This course teaches the importance of operational risk in financial institutions and its impact on performance and reputation. It covers frameworks like those from the Basel Committee on Banking Supervision. Real-life examples helped me to understand the consequences of operational failures. Linda Etuhole Nakasole

Frequently Asked Questions

If you haven’t found your answer from our FAQ, please send us a message.

If you haven’t found your answer from our FAQ, please send us a message.