Overview

Cash-to-Accrual Accounting Course Overview

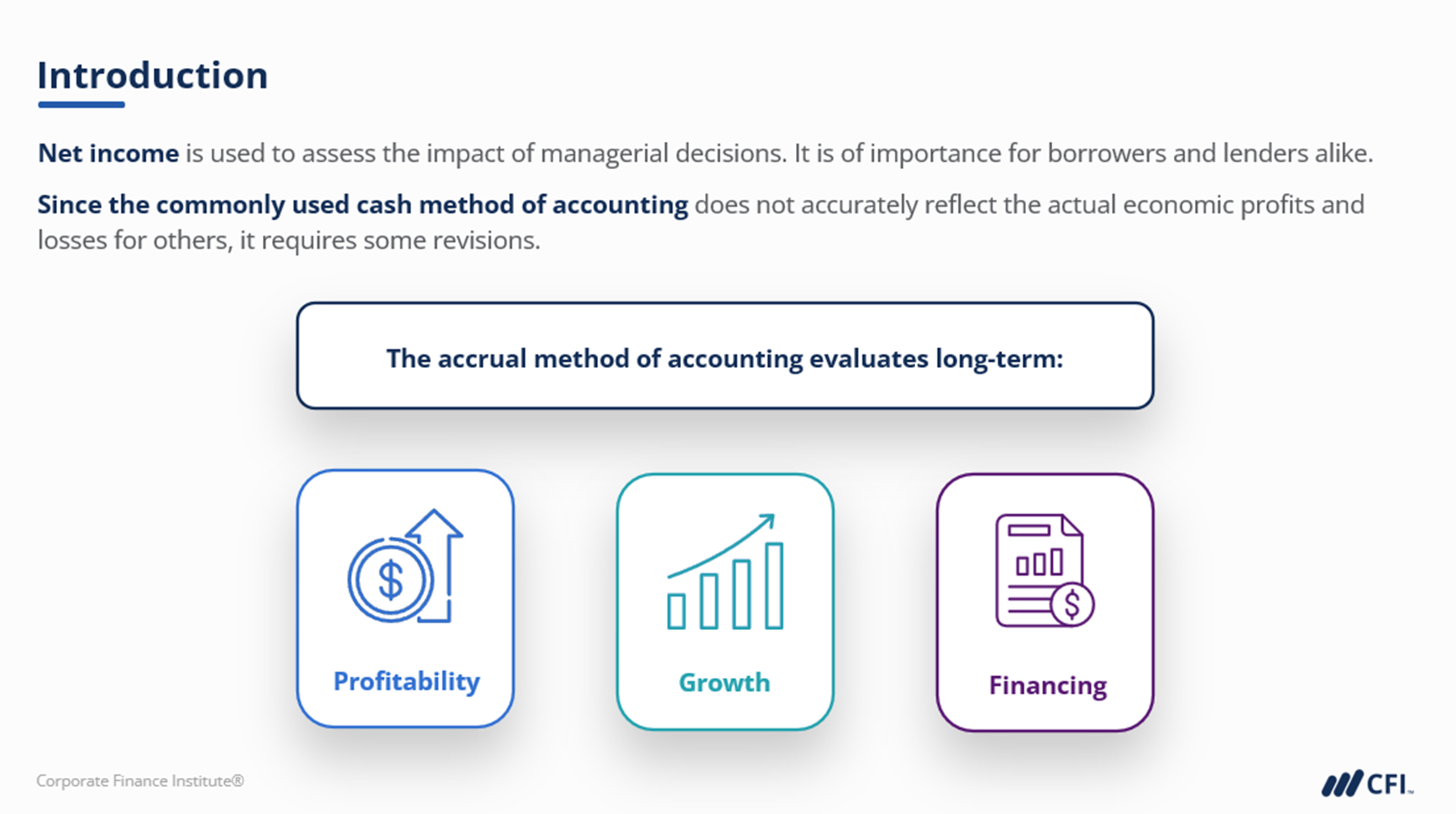

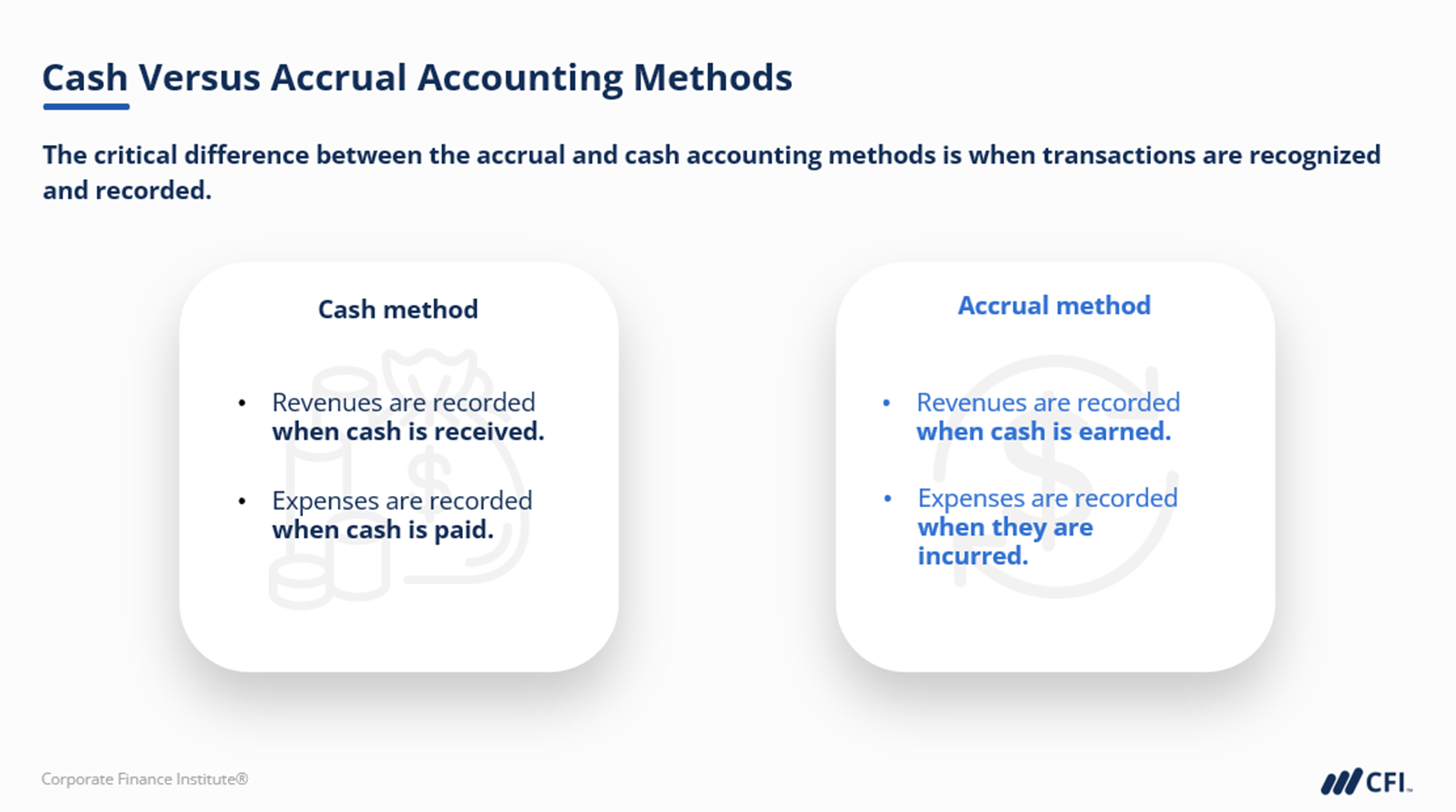

Cash is king? Not when it comes to accrual information! Learn why cash-only information presents an incomplete picture for many users of financial data and how professionals work under such circumstances.

Cash-to-Accrual Learning Objectives

Upon completing this course, you will be able to:- Differentiate the rationale for using cash and accrual information

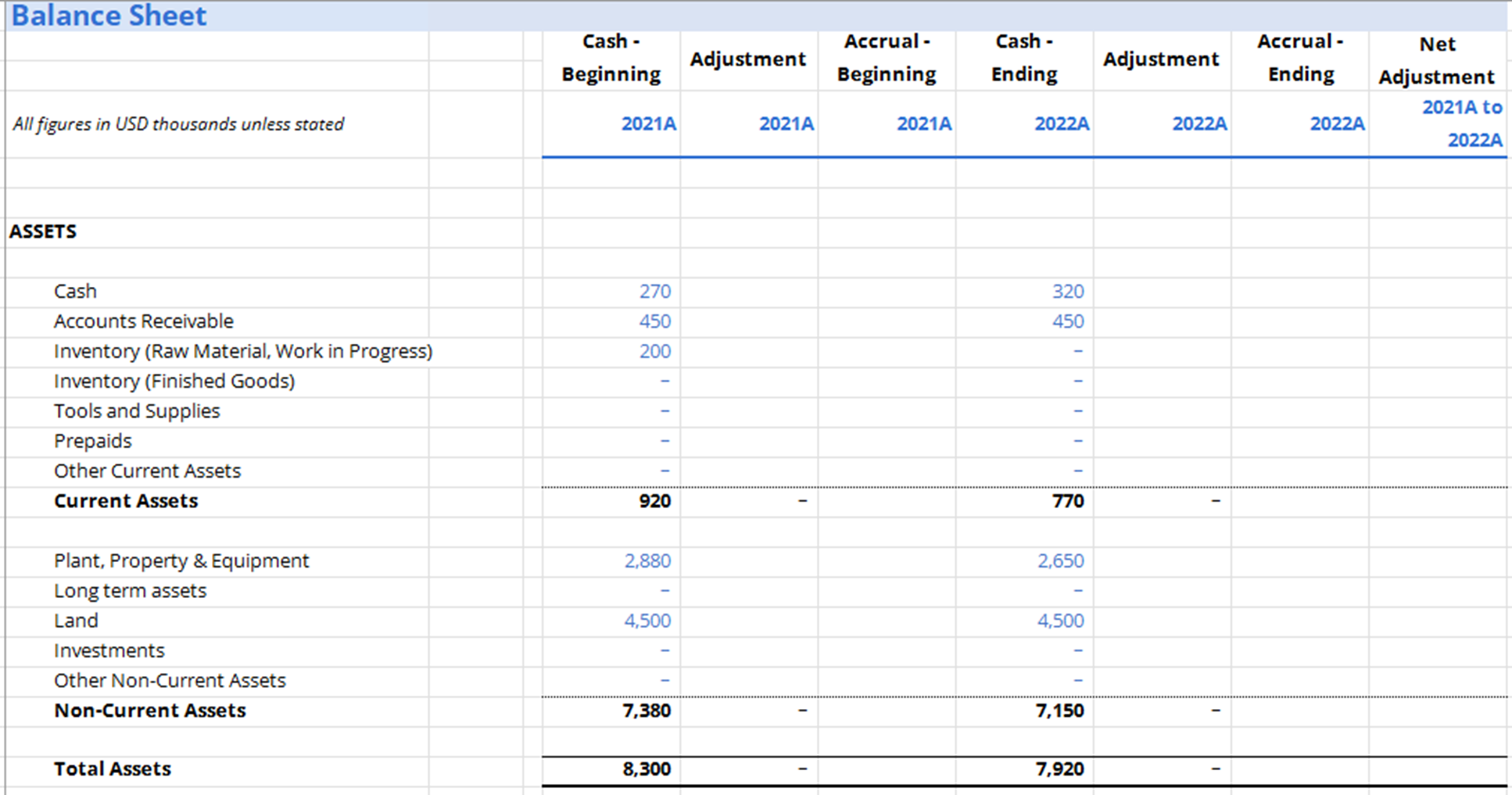

- Establish the approach to convert cash receipts and disbursements to relevant accrual data

- Practice and adjust assets, liabilities, revenues, and expenses to get cash statements closer to an equivalent set of accrual statements

- Link the different financial statements and distinguish their differences when looking at financial metrics

Who Should Take This Course?

This course is for all general business owners who work with lenders and financial professionals working with prospects and clients who rely on cash-based statements.

Cash-to-Accrual Accounting

Led by

Gabriel Lip

Level 2

1h 13min

100% online and self-paced

Field of Study: Finance

Start LearningWhat you'll learn

Lesson

Multimedia

Exams

Files

Cash Receipts

Adjust Cash Receipts

Adjust Accounts Receivable

Adjust Accounts Receivable - Excel Video

Adjust Accounts Receivable - Summary

Interactive Exercise 3

Adjust Inventory

Adjust Inventory - Excel Video 1

Adjust Inventory - Excel Video 2

Adjust Inventory - Summary

Interactive Exercise 4

Adjust Unearned Revenue

Cash Disbursements

Adjust Cash Disbursements

Adjust Consumable Assets

Adjust Consumable Assets - Excel Video 1

Adjust Consumable Assets - Excel Video 2

Adjust Consumable Assets - Summary

Interactive Exercise 5

Adjust Accounts Payable

Adjust Accounts Payable - Excel Video

Adjust Accounts Payable - Summary

Interactive Exercise 6

Other Cash and Non-Cash Expenses

Adjust Interest Payable

Adjust Interest Payable - Excel Video 1

Adjust Interest Payable - Excel Video 2

Adjust Interest Payable - Summary

Interactive Exercise 7

Adjust Taxes Payable

Adjust Taxes Payable - Excel Video

Adjust Taxes Payable - Summary

Interactive Exercise 8

Adjust Depreciation

Adjust Depreciation - Excel Video 1

Adjust Depreciation - Excel Video 2

Adjust Depreciation - Summary

Interactive Exercise 9

Adjust Deferred Tax Assets and Liabilities

Adjust Deferred Tax Assets and Liabilities - Excel Video

Conclusion and Impact

Course Summary

Qualified Assessment

This Course is Part of the Following Programs

Why stop here? Expand your skills and show your expertise with the professional certifications, specializations, and CPE credits you’re already on your way to earning.

Commercial Banking & Credit Analyst (CBCA®) Certification

- Skills Learned Financial Analysis, Credit Structuring, Risk Management

- Career Prep Commercial Banking, Credit Analyst, Private Lending

What Our Members Say

VERY SIMPLE AND UNDERSTANDABLE COURSE BUT DIFFICULT TO GET TRICK QUESTIONS

VERY INTERESTING AND AMAZING COURSE ALIYU ABUBAKAR

Brief and understandable

This course is brief and understandable, on how cash-based method and accrual-based accounting differ from one another. Atinafu Asefa

Best Financing Learning Platform

CFI is the best platform; many have created courses, but you really feel the value they added to financial teaching.

Great Work CFI! Yaseen Ghori

Great and happy to learn

This course is great. It teaches us the basic accounting method and adjustment from cash to accrual. It's quite tricky and hard when we try to adjust the different accounting method. But once we understand, it's very helpful in real world Arvin winatha

Frequently Asked Questions

If you haven’t found your answer from our FAQ, please send us a message.

If you haven’t found your answer from our FAQ, please send us a message.