Overview

Making Effective Business Decisions Course

This course equips financial professionals — especially those in Financial Planning & Analysis (FP&A) — with the tools and frameworks needed to assess capital investments confidently. You’ll learn to differentiate between various types of investments, apply financial modeling techniques like Net Present Value (NPV) and Internal Rate of Return (IRR), and navigate challenges such as opportunity costs, allocated overhead, and risk assessment.

Making Effective Business Learning Objectives

- Identify different types of investments a company can make.

- Develop a structured approach that ensures relevant information is included in the analysis.

- Understand key investment decision-making principles.

- Overcome challenges when calculating the financial impact of strategic investments.

Who Should Take This Course?

This course is ideal for FP&A professionals, financial analysts, and business decision makers who are responsible for evaluating capital investments and making data-driven financial recommendations. It is also ideal for aspiring FP&A professionals looking to develop a structured approach to business analysis and using tools like NPV and IRR.Prerequisite Courses

Recommended courses to complete before taking this course.

Prerequisite Skills

Recommended skills to have before taking this course.

- Excel

Making Effective Business Decisions

Led by

Jeff Schmidt

Level 3

2h 7min

100% online and self-paced

Field of Study: Finance

Start LearningWhat you'll learn

Lesson

Multimedia

Exams

Files

Types of Investments

Introduction to Business Decisions

Free Preview

Types of Investments

Free Preview

Maintenance Investments – Replacement Investments

Free Preview

Maintenance Investments – Regulatory Investments

Free Preview

Growth Investments – Expansion Investments

Growth Investments – New Products and Services

Growth Investments – Mergers & Acquisitions

Summary – Maintenance vs Growth Investments

Interactive Exercise 1

Developing a Structured Approach

Capital Allocation Process

Capital Allocation Process – Idea Generation

Capital Allocation Process - Analysis

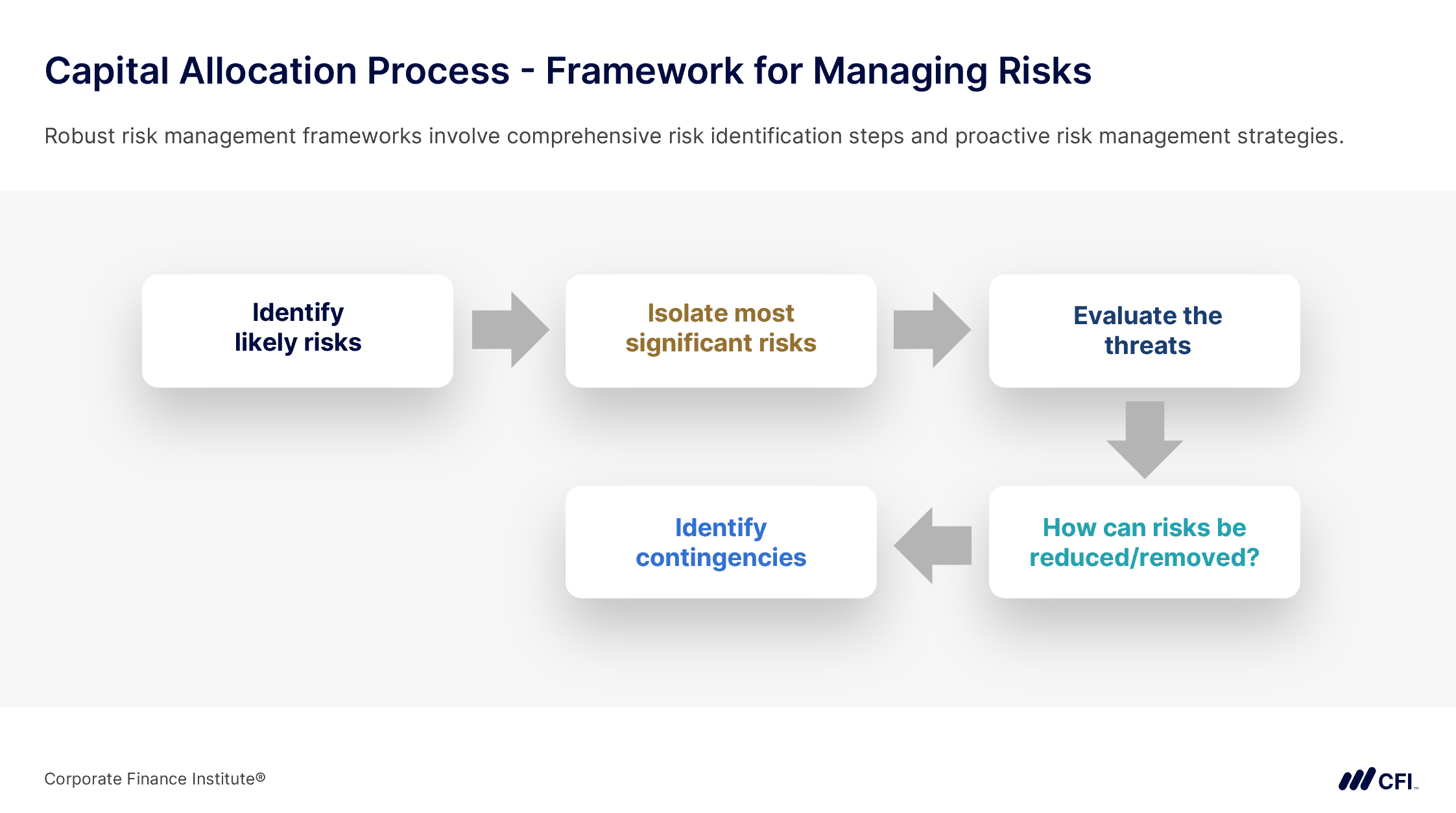

Capital Allocation Process - Framework for Managing Risks

Capital Allocation Process – Potential Risks

Interactive Exercise 2

Capital Allocation Process - Planning

Capital Allocation Process - Monitoring

Summary – Developing a Structured Approach

Interactive Exercise 3

Investment Decision-Making Tools (NPV/IRR)

Understanding Capital Investment Decisions

Capital Constraints & Investment Evaluation Tools

Understanding Net Present Value (NPV)

Downloadable Course Files

NPV Tour

XNPV Tour

Interactive Exercise 4

NPV Debrief

Understanding Internal Rate of Return (IRR)

IRR Tour

Interactive Exercise 5

IRR Debrief

Understanding Profitability Index (PI)

Ranking Conflicts in Investment Decisions

Ranking Tour

Interactive Exercise 6

Ranking Debrief

Solver

Solver Add-in

Using the Solver Add-in

Interactive Exercise 7

Other Considerations in Investment Decision Making

Considering Intangible Benefits in Investment Decisions

The Balanced Scorecard Approach

Other Factors – Externalities

Other Factors – Excess Capacity

Other Factors – Allocated Costs

Other Factors – Project Life

Other Factors – Optionality

Approximately Right vs Precisely Wrong

Interactive Exercise 9

Comprehensive Example

Comprehensive Example Introduction

CapEx and Operating Expense Tour

Interactive Exercise 10

CapEx and Operating Expense Debrief

Working Capital and Equipment Tour

Interactive Exercise 11

Working Capital and Equipment Debrief

Project Analysis Tour

Interactive Exercise 12

Project Analysis Debrief

Project Analysis Debrief Continued

Sensitivity Analysis and Probability Weighted

Course Summary

Frequently Asked Questions

If you haven’t found your answer from our FAQ, please send us a message.

If you haven’t found your answer from our FAQ, please send us a message.