Overview

Budgeting and Forecasting

This financial budgeting course will teach you about the entire budgeting process from start to finish, including how to create a disciplined culture of budgeting in your organization, the various methods for building budgets, techniques to analyze results, and how to increase the chances of organizational performance improvements.

This interactive and applied budgeting course enables participants to:

- Adopt a disciplined approach to developing budgets

- Forecast results with quantitative and qualitative methods

- Effectively use variance analysis to track performance

- Present results with charts and graphs

Who should take this budgeting class?

This online budgeting class is designed for those who are responsible for financial management, budgeting, and forecasting within their organizations. This may include professionals working in financial planning and analysis (FP&A), accounting, treasury, financial reporting, corporate development, etc.

What you will learn in this budgeting 101 course

By the end of this budgeting 101 class, participants are able to:

- Understand the principles behind best practice financial management

- Explain the importance of budgeting within a strategic framework

- Build a robust budgeting process within their organization

- Know when and where to use various budgeting approaches such as zero-based budgeting

- Forecast future performance by better analyzing revenue and cost drivers

- Use effective variance reporting to track organizational performance

- Make use of Excel functions and tools that are particularly suited to the budgeting process.

Financial budgeting class content

Topics covered will include:

- Budgeting within a strategic framework

- Building a robust budgeting process

- Managing budget psychology

- A practical guide to developing budgets

- Common budgeting approaches (e.g. Incremental, value-based, zero-based, etc.)

- Forecasting techniques (moving average, regression analysis, etc.)

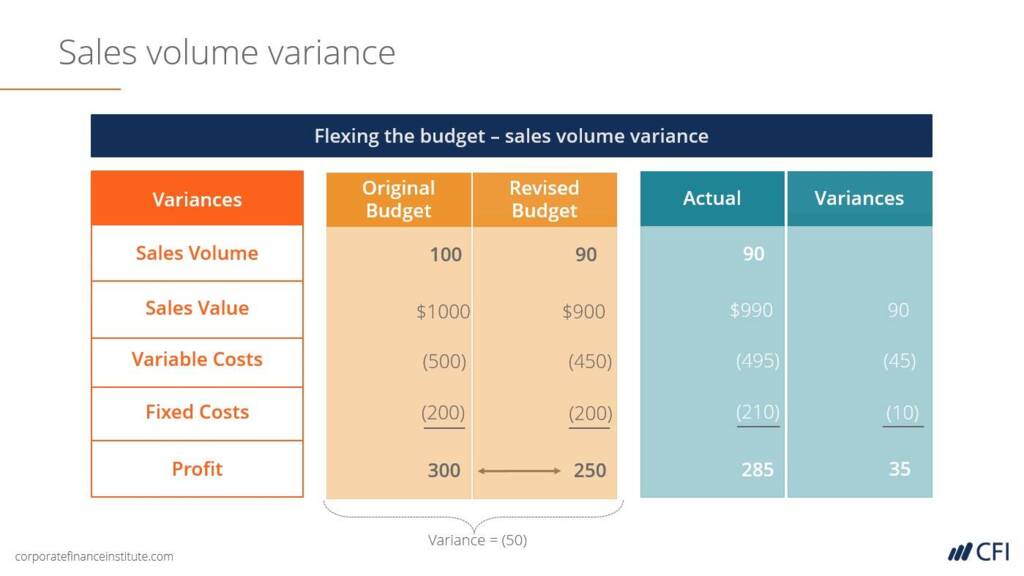

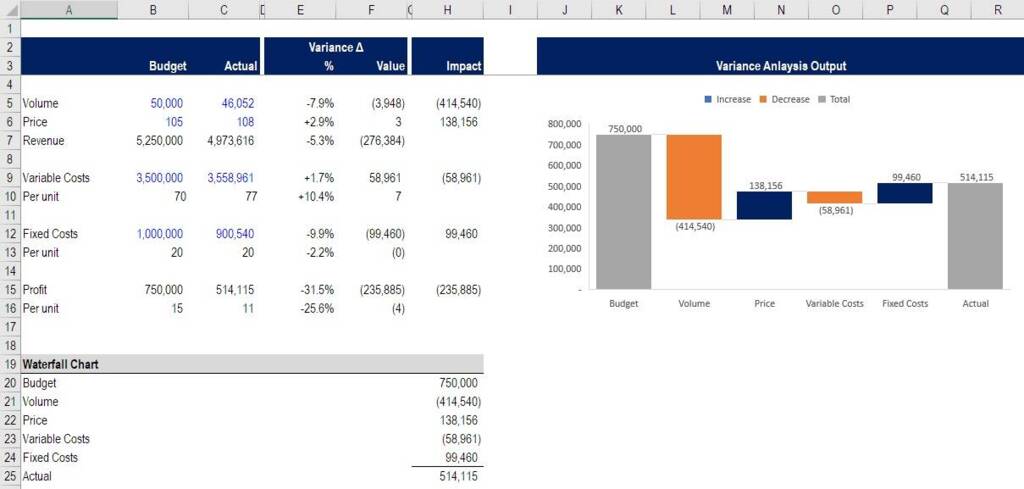

- Tracking budget performance with variance analysis (waterfall charts, etc.)

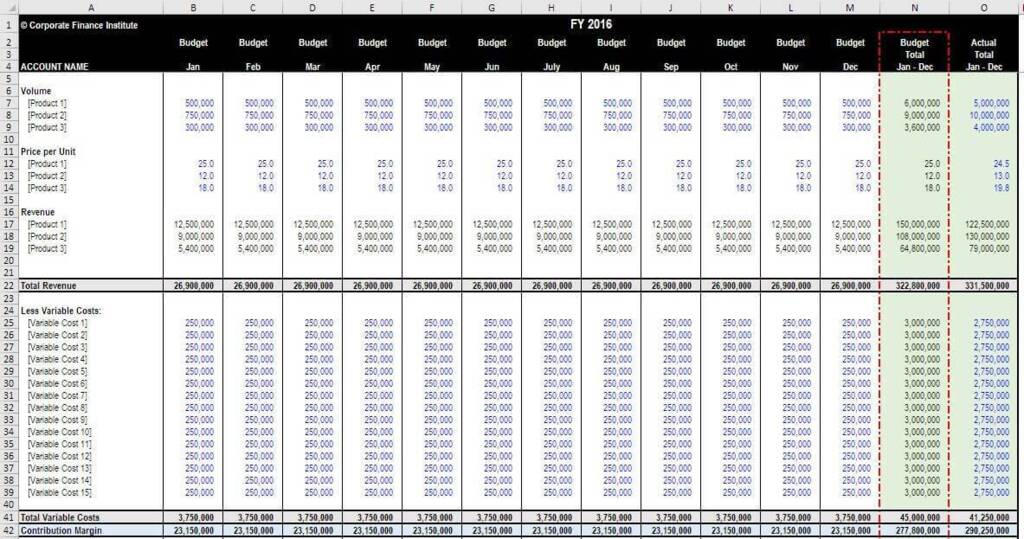

- Applied budgeting tools and techniques (Excel, solver, pivot tables, etc.)

CPE Information

For further CPE information, please read before purchasing:

https://corporatefinanceinstitute.com/about/cpe-information/

Publish Date: Sep 06, 2017

Last Revision: Jan 18, 2018

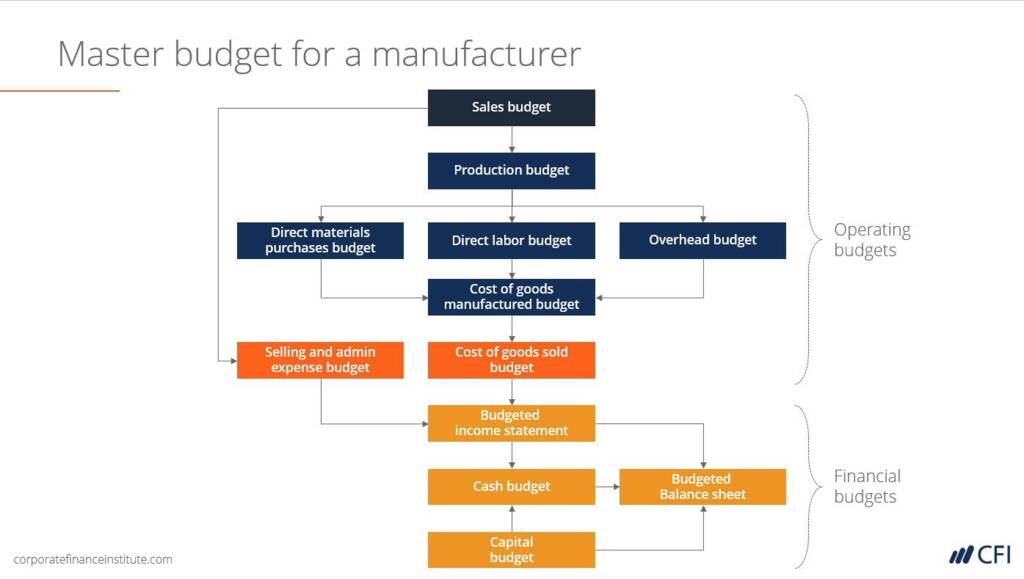

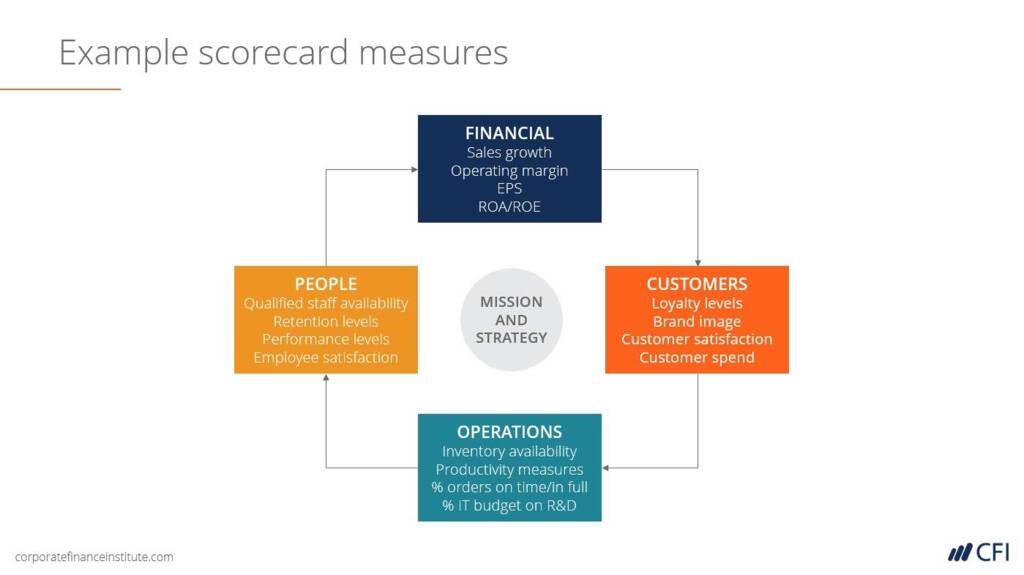

Budgeting 101 class screenshots

Prerequisite Courses

Recommended courses to complete before taking this course.

Prerequisite Skills

Recommended skills to have before taking this course.

- Excel

- Critical thinking

- Financial accounting

Budgeting and Forecasting

Level 3

2h 44min

100% online and self-paced

Field of Study: Finance

Start LearningWhat you'll learn

Building a Robust Budgeting Process

A Practical Guide to Developing Budgets

Forecasting Techniques

Tracking Budget Performance with Variance Analysis

Applied Budgeting Tools and Techniques in Excel

Qualified Assessment

This Course is Part of the Following Programs

Why stop here? Expand your skills and show your expertise with the professional certifications, specializations, and CPE credits you’re already on your way to earning.

Financial Modeling & Valuation Analyst (FMVA®) Certification

- Skills Learned Financial modeling and valuation, sensitivity analysis, strategy

- Career Prep Investment banking and equity research, FP&A, corporate development

Financial Planning & Analysis (FP&A) Specialization

- Skills Learned Accounting, Finance, Excel, Data Analysis, Financial Statement Analysis, Financial Modeling, Budgeting, Forecasting, Power Query, Power BI, and more.

- Career Prep Financial Analyst, Project Evaluator, FP&A Manager and more

Finance for Non-Finance Managers

- Skills You’ll Gain Accounting, Finance, Budgeting and Forecasting, Strategy

- Great For Operations, Marketing or Sales Managers, Department Heads/Team Leaders, Strategy Consultant, Non-Finance Executive Roles (e.g. COO, CTO) and more