Overview

Normalizing Income Statements Overview

Normalizing Income Statements is designed to teach learners how to adjust and interpret income statements for financial analysis and decision making. This course empowers learners with the skills necessary to transform financial statements, ensuring they accurately represent a company’s core operations and are ideal for use in diverse financial modeling and valuation contexts.

Normalizing Income Statements Learning Objectives

- Understand the concept of normalization

- Apply practical normalization techniques

- Interpret real-world financial documents

- Compute key financial metrics

Who Should Take This Course?

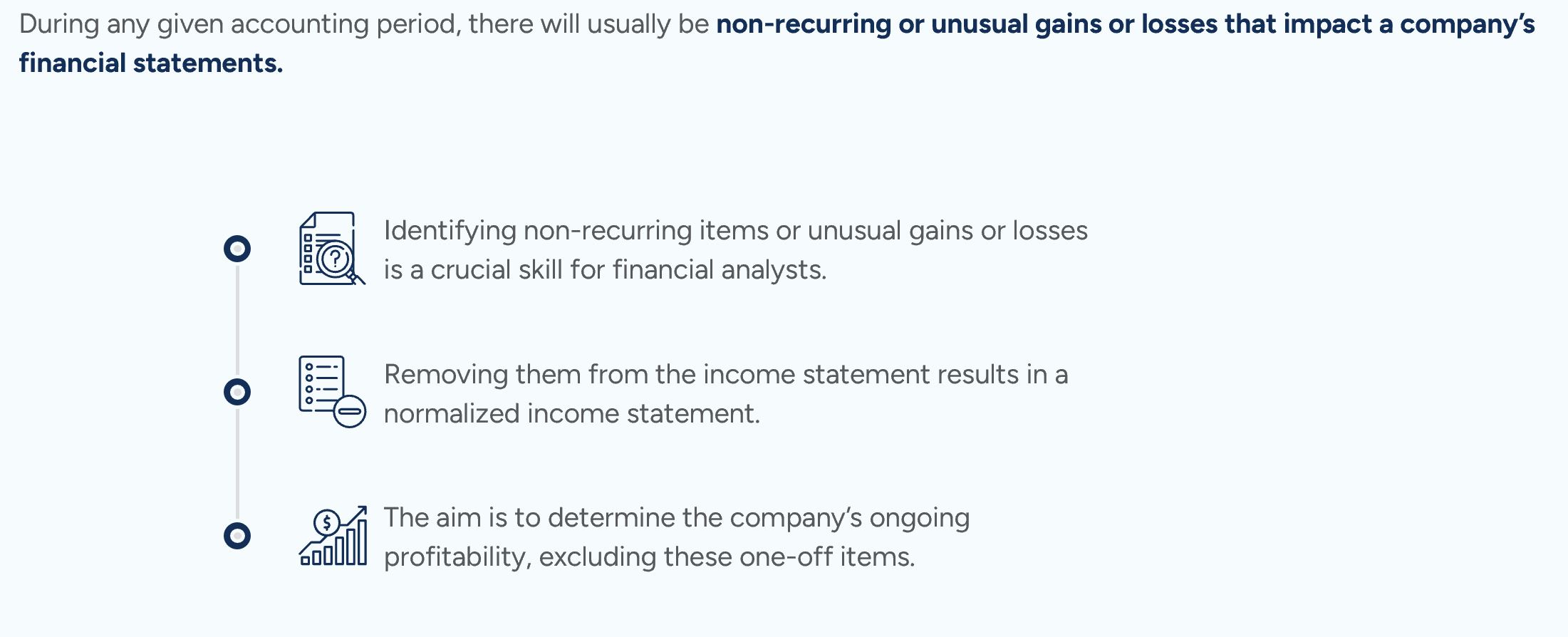

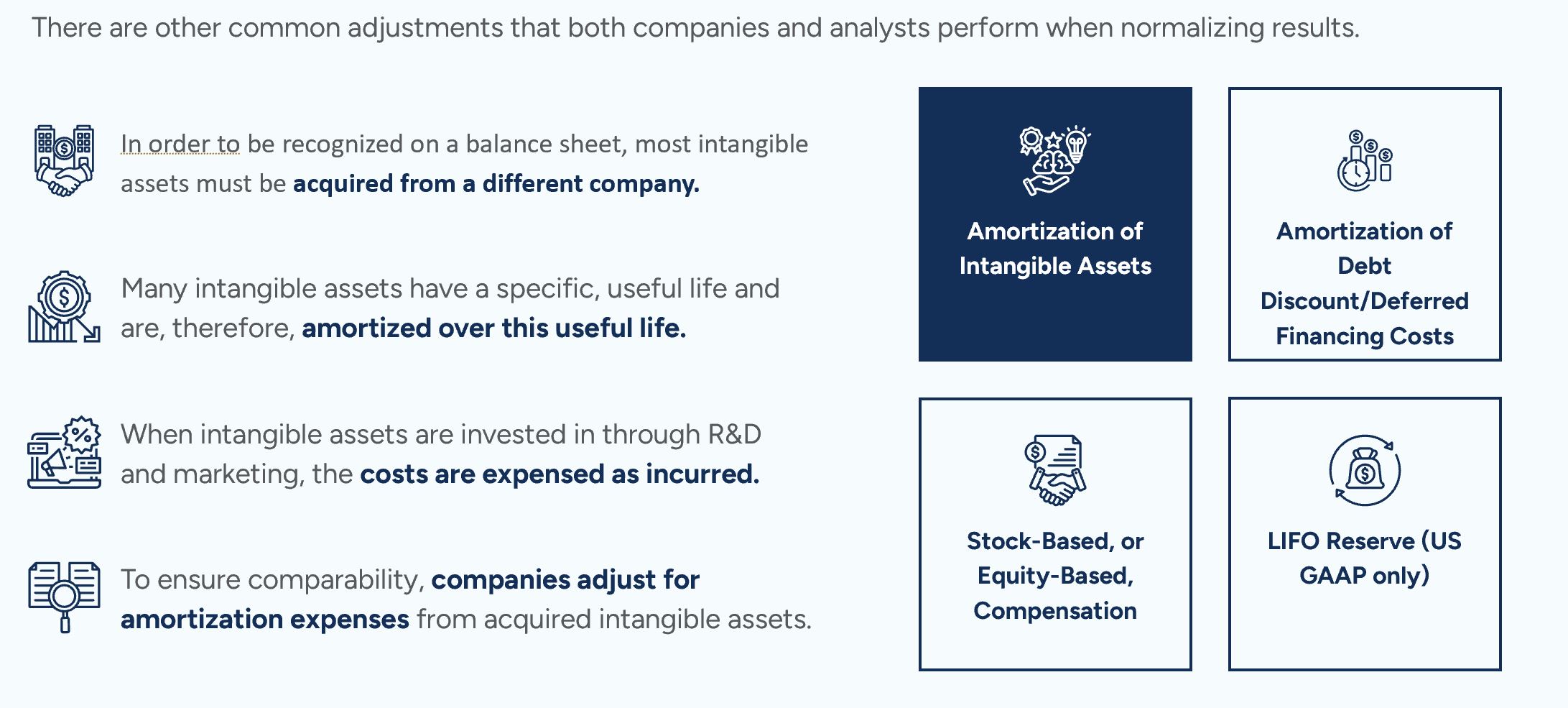

Unexpected, non-recurring items are bound to happen to any company. These can dramatically impact a company’s financial statements, skewing the underlying operating performance. Therefore, financial analysts need to be able to identify and adjust for these one-time items to better understand a company’s true performance. This course is perfect for anyone who uses and analyzes financial statements, including investment bankers, equity research analysts, and financial planning and analysis (FP&A) professionals.

Courses we recommend you take in advance

Normalizing Income Statements

Level 5

1h 30min

100% online and self-paced

Field of Study: Finance

Start LearningWhat you'll learn

The Essentials of Normalizing Income Statements

Practical Examples

This Course is Part of the Following Programs

Why stop here? Expand your skills and show your expertise with the professional certifications, specializations, and CPE credits you’re already on your way to earning.

Financial Modeling & Valuation Analyst (FMVA®) Certification

- Skills Learned Financial modeling and valuation, sensitivity analysis, strategy

- Career Prep Investment banking and equity research, FP&A, corporate development

Accounting for Financial Analysts Specialization

- Skills learned Accounting, Financial Analysis, Reading Financial Statements and more

- Career prep Financial Planning & Analysis (FP&A), Corporate Development, Investment Banking, Private Equity, Equity Research, and more.

Investment Banking & Private Equity Modeling Specialization

- Skills You’ll Gain Accounting, Advanced Financial Modeling, Excel, Financial Statement Analysis, Forecasting, Valuation, and more.

- Great For Investment Banking, Private Equity, Equity Research, and more