Overview

Accounting for Business Combinations & Other Equity Investments Overview

In CFI’s “Accounting for Business Combinations & Other Equity Investments”, we’ll demystify the core aspects of accounting for business combinations. You’ll discover how to undertake a business consolidation, apply the equity method to investments where a company exerts a significant influence as well as how to account for smaller equity investments. Throughout the course, we’ll engage in a series of practical mini case studies using Excel, allowing you to apply and solidify your understanding of these accounting techniques through hands-on practice.

Accounting for Business Combinations & Other Equity Investments Learning Objectives

Upon completing this course, you will be able to:

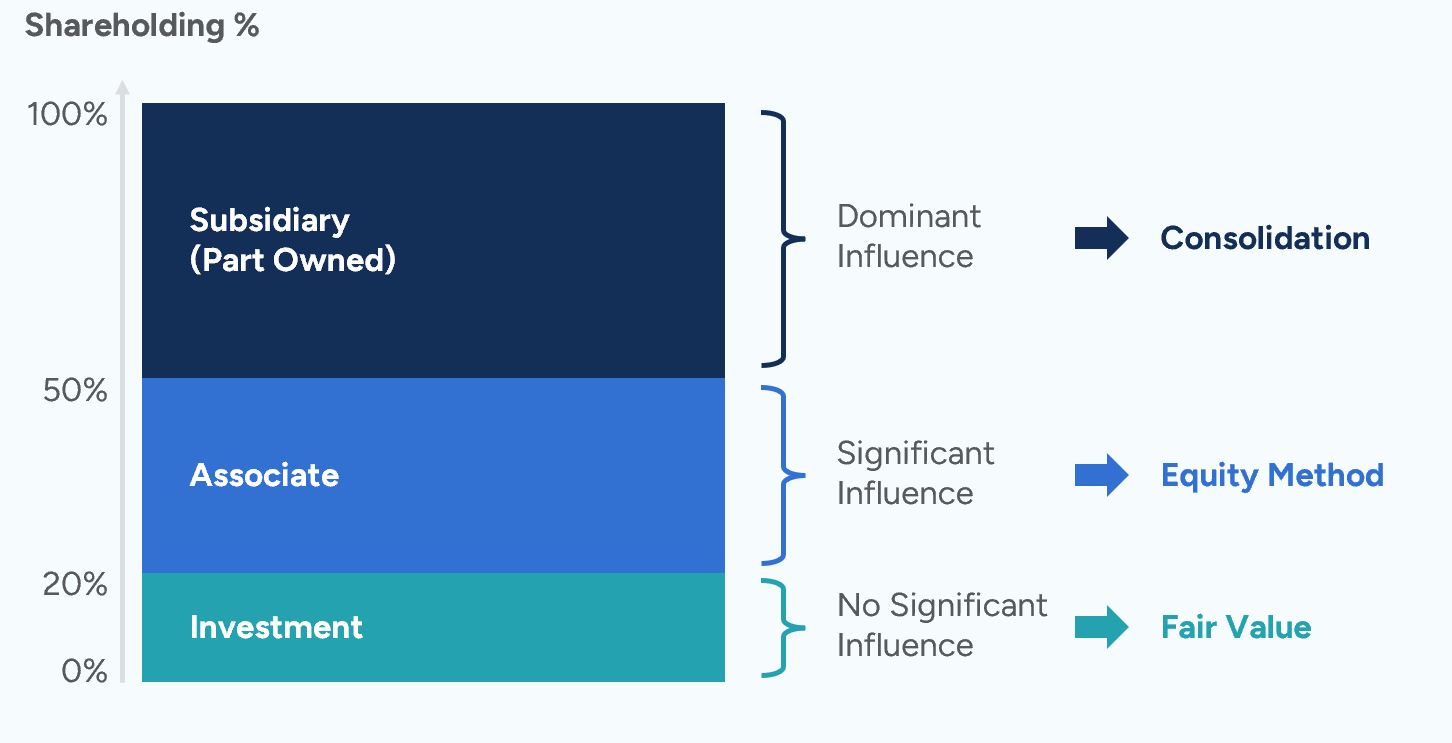

- Account for equity investments where one company owns more than 50% of another company’s equity.

- Calculate goodwill associated with a business combination.

- Account for equity investments where a company has significant influence over another company (owning between 20% to 50% of the company’s equity).

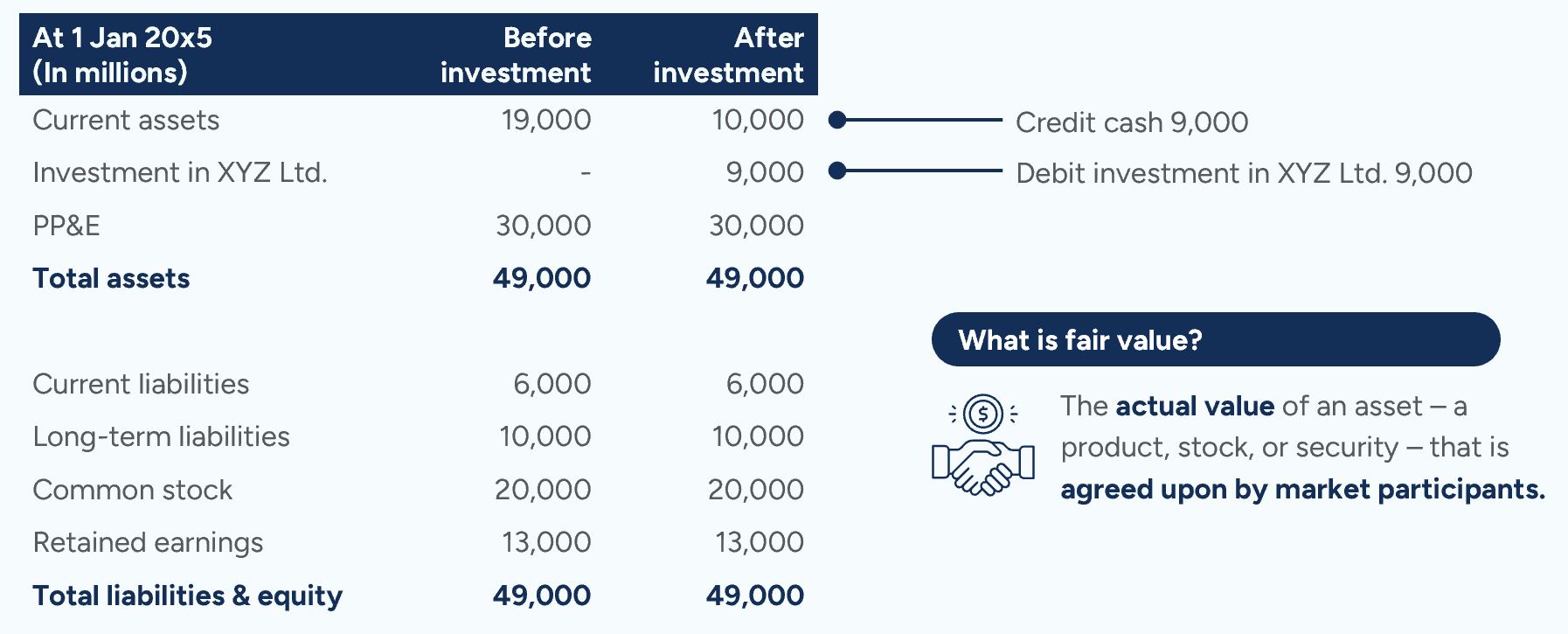

- Account for equity investments where a company owns less than 20% of the equity of another company.

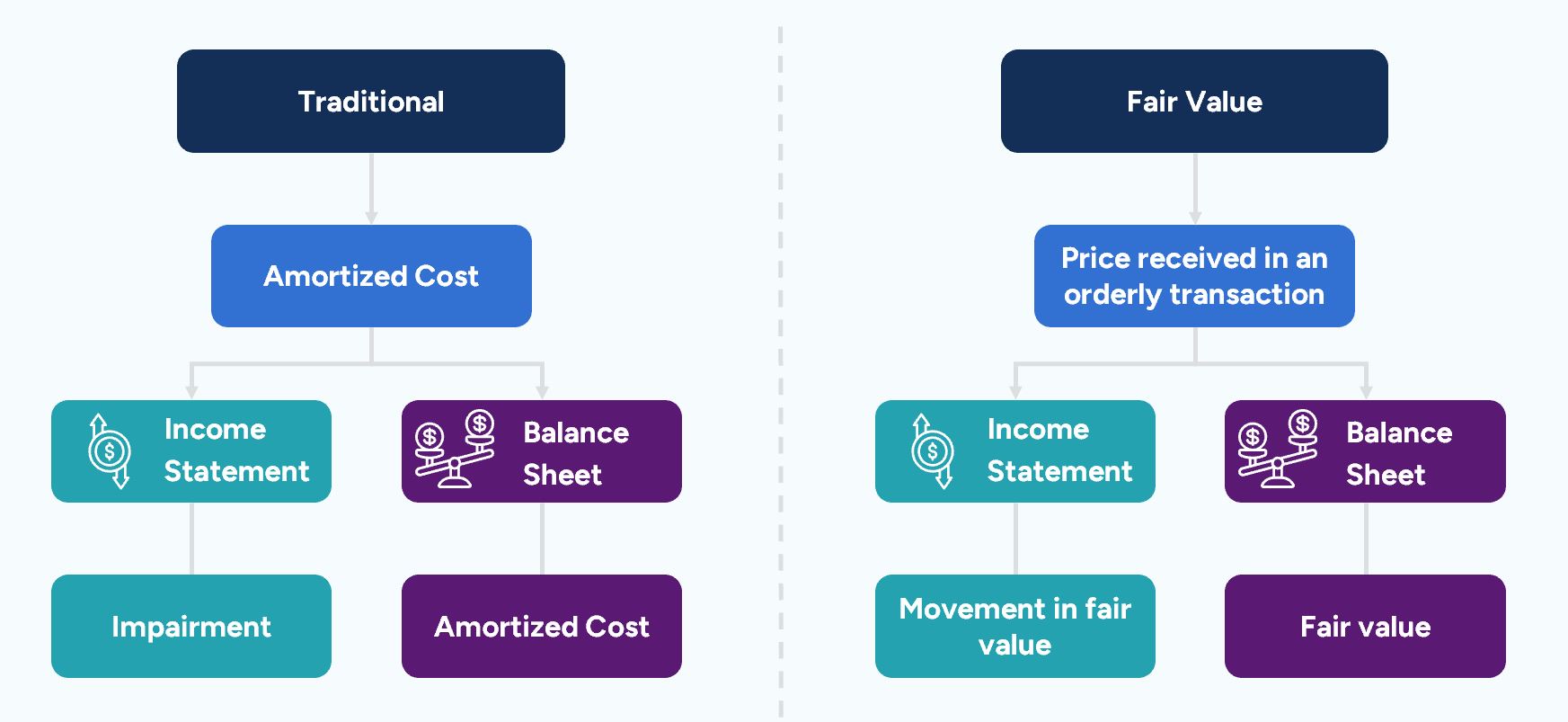

- Explain a key difference in accounting for equity investments under IFRS versus US GAAP.

Recommended Prep Courses

These preparatory courses are optional, but we recommend you complete the stated prep course(s) or possess the equivalent knowledge prior to enrolling in this course:

Who Should Take This Course?

This course teaches analysts about accounting rules for business consolidations and equity investments. It’s important for analysts to accurately assess the value of these investments to determine the correct valuation of both the investment and the companies involved.

Prerequisite Courses

Recommended courses to complete before taking this course.

Accounting for Business Combinations & Other Equity Investments

Level 3

1h 14min

100% online and self-paced

Field of Study: Finance

Start LearningWhat you'll learn

80% Control Consolidations

This Course is Part of the Following Programs

Why stop here? Expand your skills and show your expertise with the professional certifications, specializations, and CPE credits you’re already on your way to earning.

Accounting for Financial Analysts Specialization

- Skills learned Accounting, Financial Analysis, Reading Financial Statements and more

- Career prep Financial Planning & Analysis (FP&A), Corporate Development, Investment Banking, Private Equity, Equity Research, and more.