Overview

FP&A Professional Financial Statement Aggregation & Analysis Overview

CFI’s “FP&A Professional Financial Statement Aggregation & Analysis” course will help you understand how to construct financial statements using FP&A totals. We will also review best-in-class approaches to aggregating monthly figures up into quarterly and annual amounts.

FP&A Professional Financial Statement Aggregation & Analysis Learning Objectives

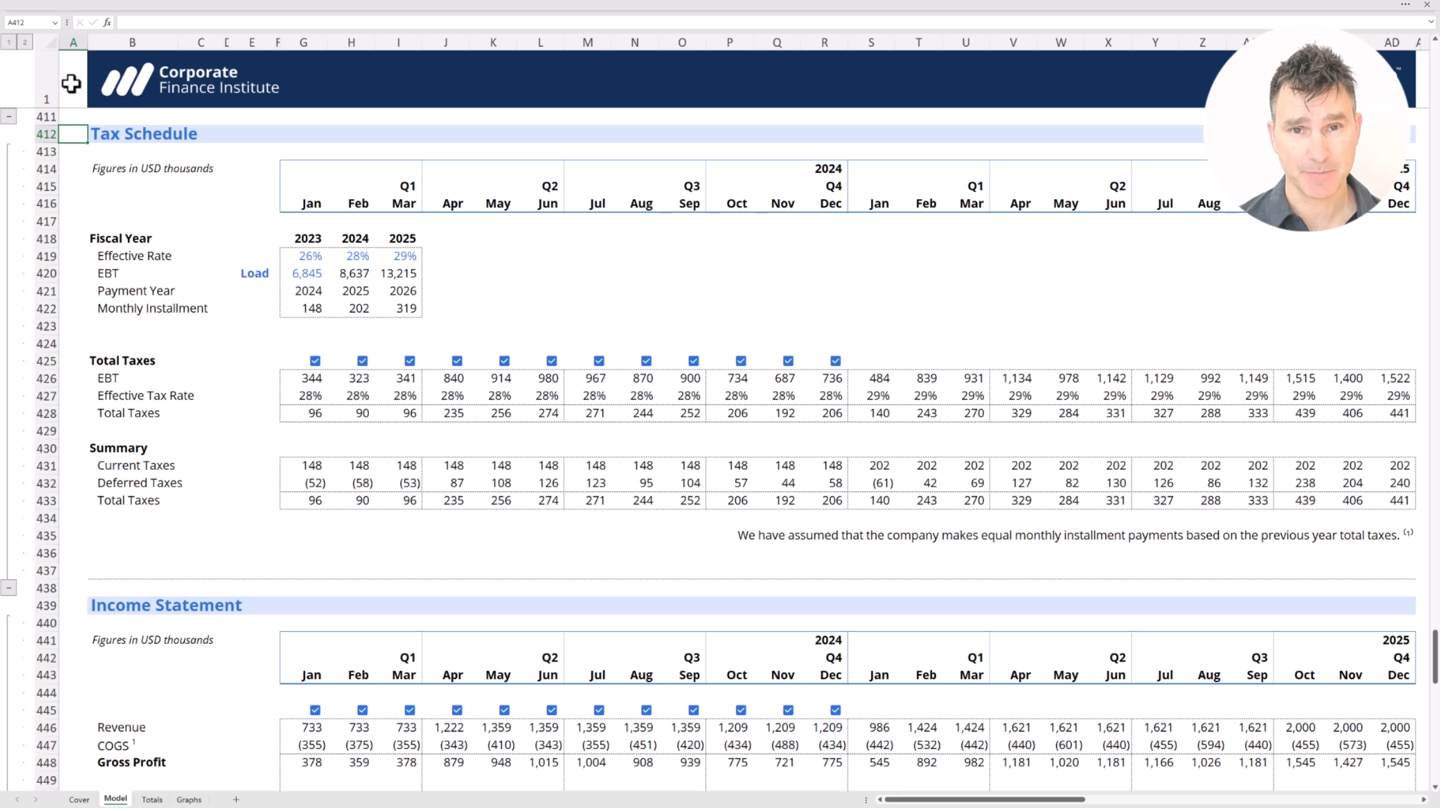

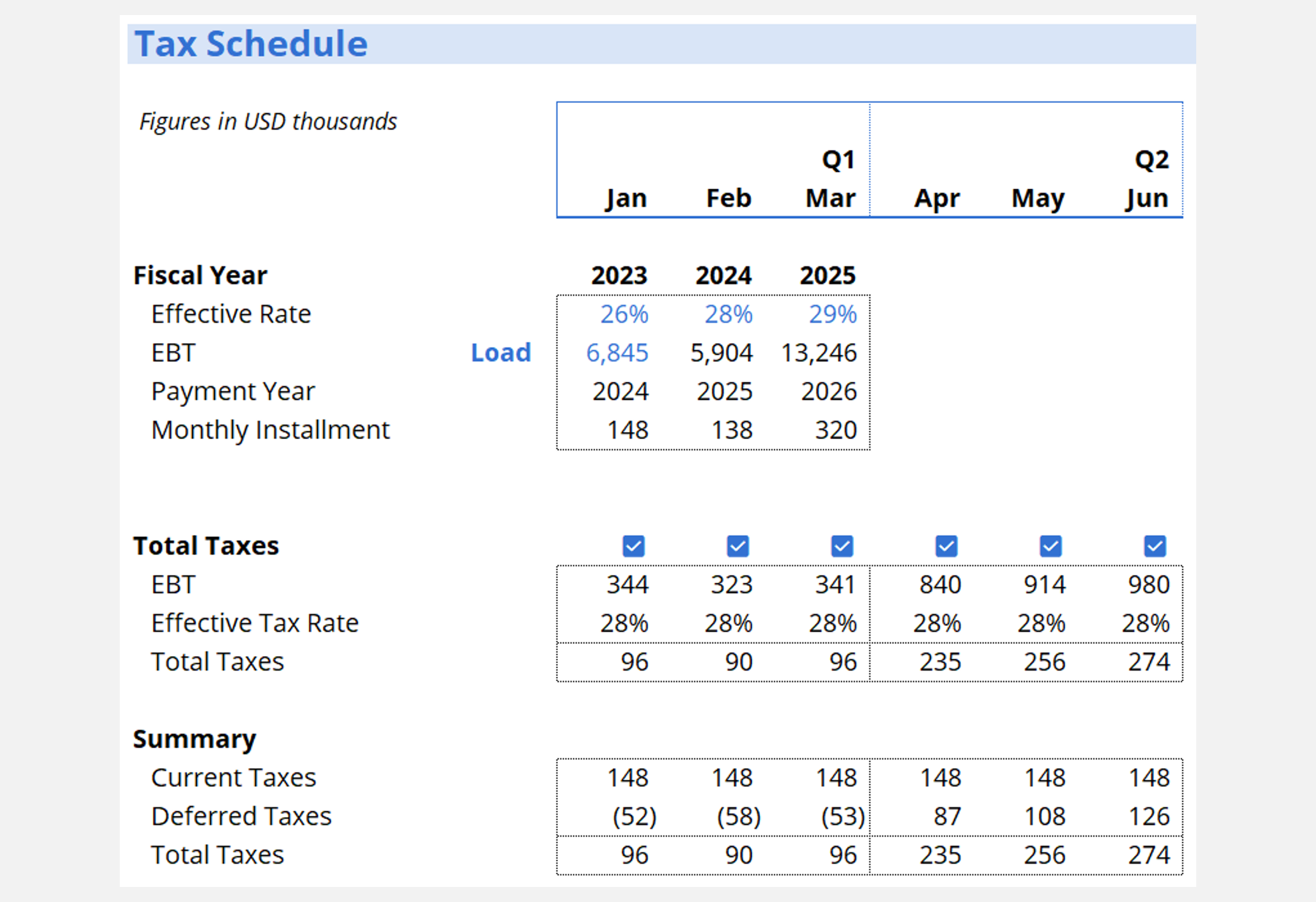

Upon completing this course, you will be able to:- Understand the difference between current & deferred income taxes and why both are needed in FP&A models.

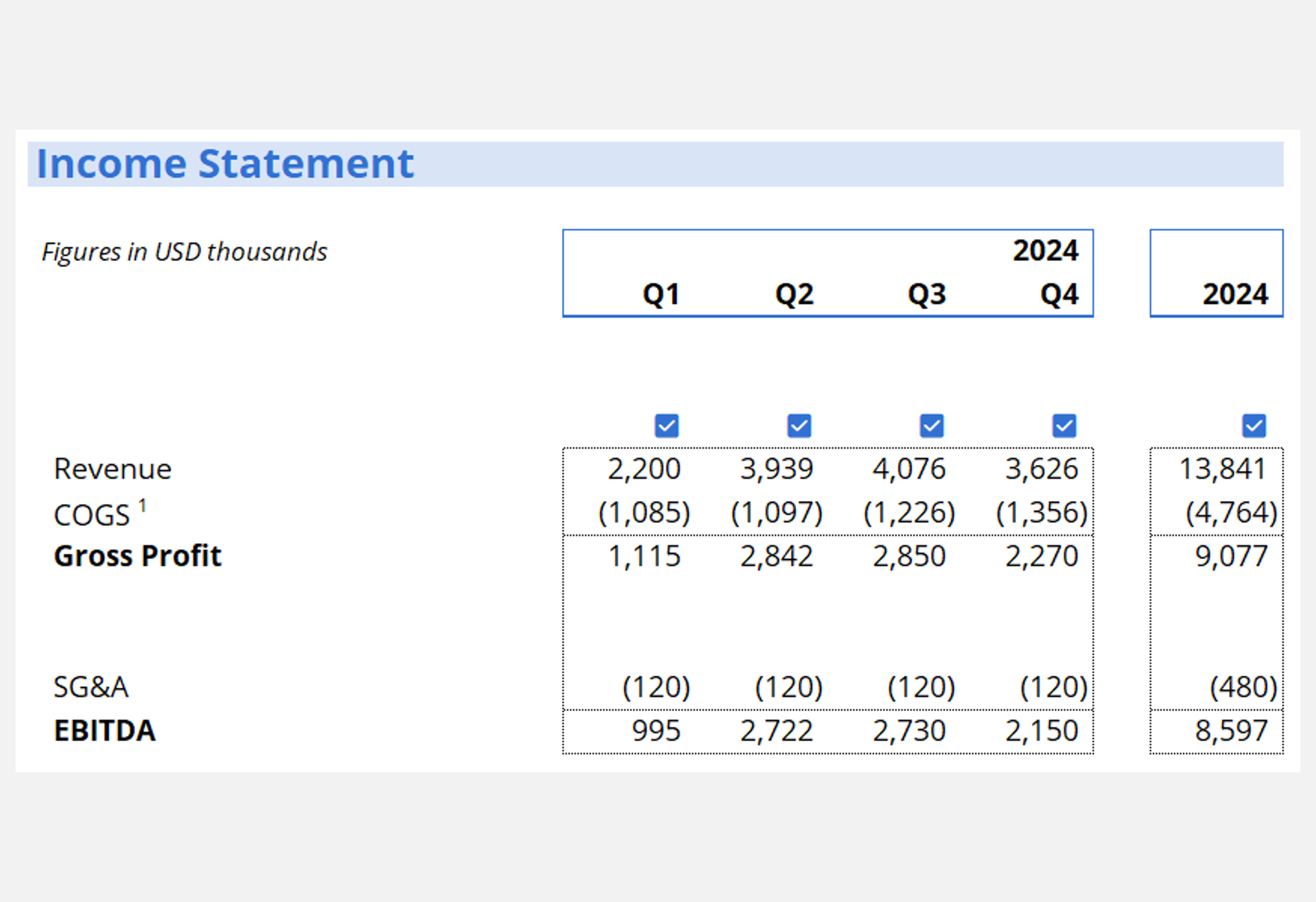

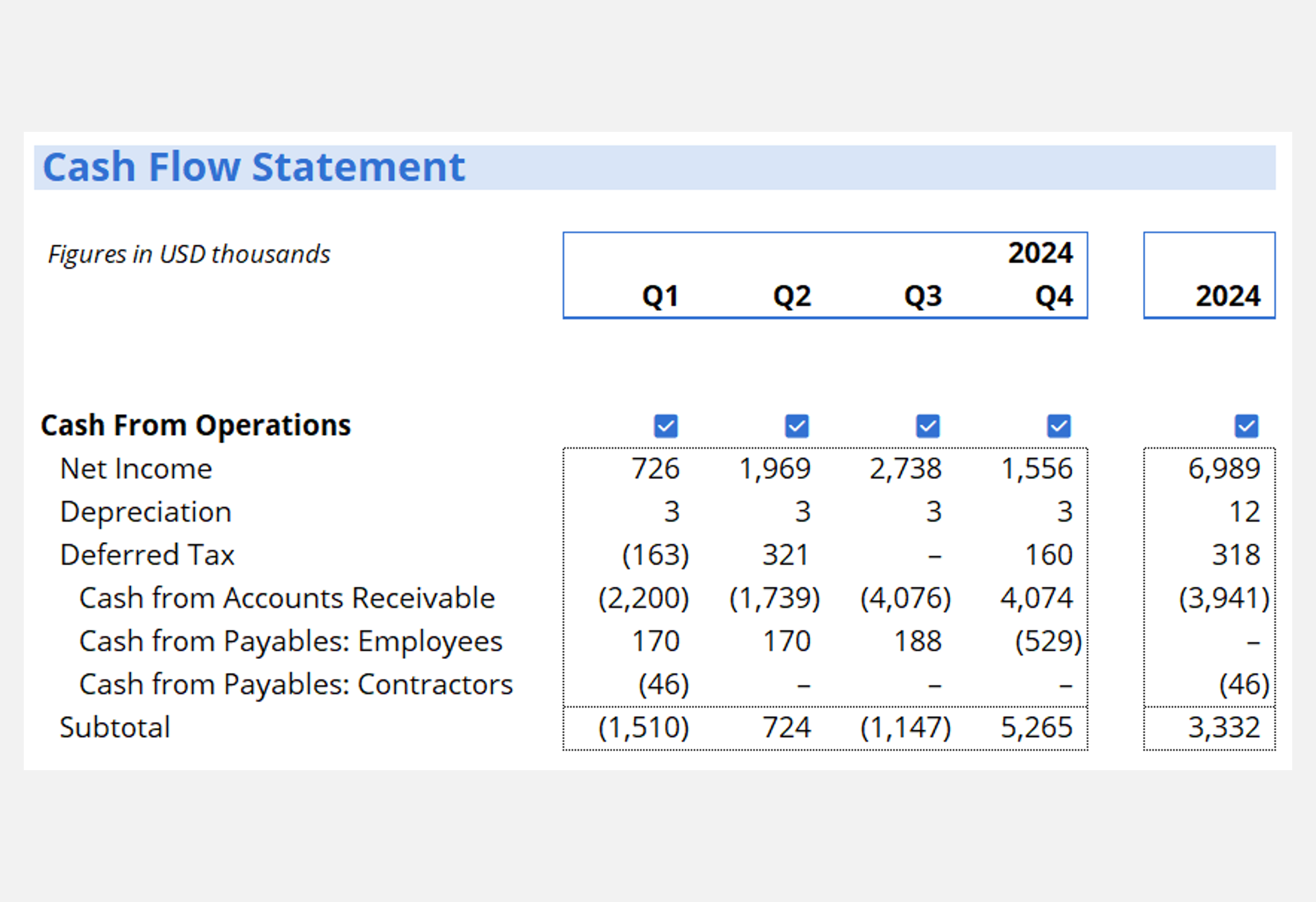

- Use consolidated monthly financial statements to determine the company’s health in terms of profitability and cash flow

- Use Excel functions to aggregate monthly figures into quarterly and annual estimate.

Who Should Take This Course?

This course is perfect for FP&A professionals at a beginner, intermediate, or even advanced level. This course is a part of a series of FP&A courses.

Prerequisite Courses

Recommended courses to complete before taking this course.

FP&A Professional Financial Statement Aggregation & Analysis

Led by

Duncan McKeen

Level 3

1h 10min

100% online and self-paced

Field of Study: Finance

Start LearningWhat you'll learn

Lesson

Multimedia

Exams

Files

Financial Statements

Course Summary

Qualified Assessment

This Course is Part of the Following Programs

Why stop here? Expand your skills and show your expertise with the professional certifications, specializations, and CPE credits you’re already on your way to earning.

Financial Planning & Analysis (FP&A) Specialization

- Skills Learned Accounting, Finance, Excel, Data Analysis, Financial Statement Analysis, Financial Modeling, Budgeting, Forecasting, Power Query, Power BI, and more.

- Career Prep Financial Analyst, Project Evaluator, FP&A Manager and more

What Our Members Say

This course is great and useful for my work and I would like to suggest CFI adding excel functions like XLOOKUP that still not applicable for student to learn as a bonus license.

Kong Chhay

Brilliant use of excel , neat and clean and super easy to learn , Highly Recommend this course

Kartik Goyal

I advice not to relent but study it with all seriousness

Patrick Fassay

Useful to learn and practice shortcuts

Duncan is an amazing teacher. In the last two years I have sharpened my financial and excel skills thanks to all the shortcuts and schedules he teaches through CFI. Highly recommended. Juan David Angel L.

Frequently Asked Questions

If you haven’t found your answer from our FAQ, please send us a message.

If you haven’t found your answer from our FAQ, please send us a message.