Overview

Microsoft Word Tutorial Course Overview

This Microsoft Word Tutorial – Business Documents course covers the most important functions, tools, tips, and best practices for document structure and design. This course is designed specifically for financial analysts or professionals working in the area of corporate finance who need to create Word documents at work.

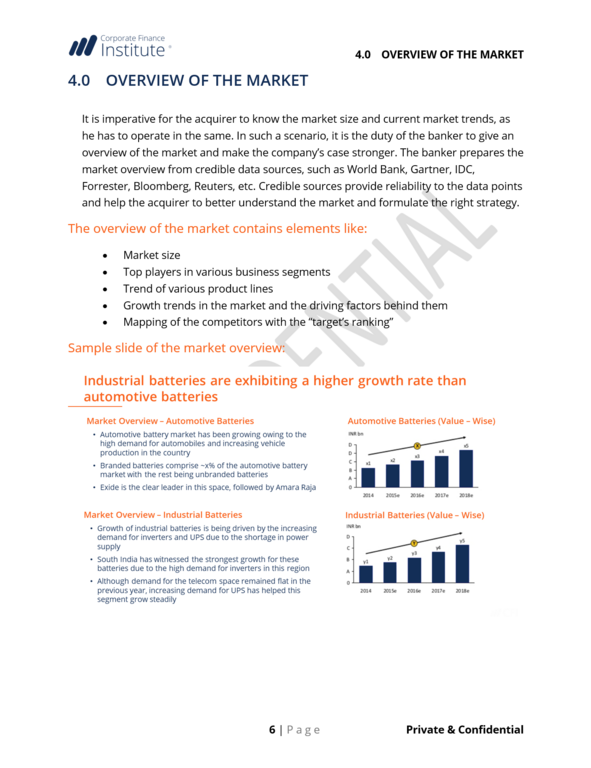

This course will walk through the process of creating a Confidential Information Memorandum (CIM), which is a document used in mergers and acquisitions (M&A) to convey important information about a business to a potential buyer. We’ll demonstrate the use of various functions and tools in Word to format the document in a clean, simple, and easy-to-follow way.

Course Learning Objectives

This Microsoft Word Tutorial course will show you the most useful functions and techniques in structuring, formatting, and auditing a Word document intended for business purposes.

Upon completing this course, you’ll be able to:

- Understand the design principles you should apply to different types of business documents

- Use features such as line spacing, headings, indentation, table of contents, footnotes and endnotes to enhance the readability of your document

- Utilize built-in tools in Microsoft Word to audit the final product

- Create a professional-looking confidential information memorandum (CIM) by following along in the course

Why Take This Microsoft Word Tutorial Course?

As a financial analyst, you often need to create polished business documents. These documents can be:

- Financial reports presented to internal and external stakeholders at a company

- Transaction documents for deals such as mergers and acquisitions (M&A) and leveraged buyout (LBO)

- Pitches to potential investors or buyers of a company which convey important financial, operational, and other information

- Work reports summarizing past and current projects for managers’ review

This course covers the basic and advanced techniques one could apply in creating a structured, informative, and easy-to-read business document in Microsoft Word. You’ll learn the key functions, tools, and tips & tricks in Word. At the end of this course, you should feel comfortable producing a unique business document that could be presented to management, investors, peers, and other audience in a professional manner.

Who Should Take This Course?

This Word tutorial is perfect for beginners who are new to Microsoft Word, or intermediate and advanced users who aim to learn how to create more professional business documents. This course is designed specifically for financial analysts or professionals working in the area of corporate finance who produce transaction documents such as the CIM.

Get the Microsoft Office Applications Bundle

If you want to learn more about all three Microsoft Office applications (Excel, PowerPoint and Word), you can enroll in CFI’s Financial Modeling & Valuation Analyst which consists of the following courses:

Prerequisite Skills

Recommended skills to have before taking this course.

- Basic computer skills

Microsoft Word Tutorial - Business Documents

Level 1

1h 15min

100% online and self-paced

Field of Study: Finance

Start Learning