Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A key financial metric for digital businesses, Return on Ad Spend helps marketers, advertising agencies, and finance professionals understand how effectively their advertising campaigns drive revenues. This understanding allows professionals to make data-driven decisions about their advertising investments.

ROAS stands for Return on Ad Spend. It measures how much revenue a business gains for every dollar spent on ad campaigns. ROAS is a key performance indicator (KPI) for advertising campaigns.

ROAS is a particularly powerful metric because it isolates the financial impact of advertising from other business activities. By focusing solely on the performance of a company’s ad campaign, ROAS allows you to:

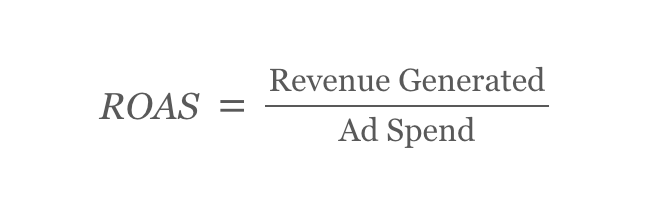

The ROAS formula is relatively simple. Take the revenue from your ad campaign and divide it by the total advertising costs for a specific campaign. The result represents your return on ad spend, providing a clear picture of how efficiently ad dollars contribute to a business’s revenue. It also allows you to align your advertising budget with revenue growth goals.

Here’s how to calculate ROAS one step at a time:

In contrast, suppose your business spends $10,000 on ads that generate $11,000 in revenue. The ads generated only $1.10 for every $1 spent. While the campaign did not lose money, a low ROAS indicates inefficiencies or missed opportunities. In most cases, the marketing team will review their marketing strategy and adjust the ads to improve the ROAS.

A negative ROAS, i.e., losing money on an ad campaign, is unsustainable in the long term.

The definition of a “good” or “acceptable” ROAS depends on the industry and the specific goals of the individual campaign business:

Understanding what constitutes a good ROAS helps businesses set realistic goals and optimize their advertising strategies to align with financial objectives.

While ROAS is a valuable metric, calculating it accurately isn’t always straightforward. Common challenges include:

To address these challenges, follow these guidelines:

For both finance and digital marketing professionals, ROAS is a tool that bridges advertising efforts and financial outcomes. Here’s why it matters:

In short, ROAS helps financial decision-makers ensure that every dollar spent on advertising contributes meaningfully to revenue earned at the bottom line.

Finance and banking professionals use ROAS in various contexts to measure business performance. Here are key examples:

While ROAS is an important metric, it’s not the only one finance professionals should consider. Here’s how it compares to other commonly used metrics:

By combining ROAS with metrics like ROI, CPA, LTV, and CAC, finance professionals and marketers can gain a comprehensive view of advertising performance and its broader business impact.

Suppose you work for a mobile app business that invests $20,000 in Google Ads and $10,000 in social media ads. The campaigns generate $120,000 and $30,000 in revenue, respectively. Here’s how ROAS helps guide decisions:

The higher ROAS for Google Ads suggests that this advertising platform also delivers better results. Based on these insights, the business might increase its Google Ads budget while optimizing its social media campaigns to improve efficiency. This approach helps ensure that resources are allocated to the most profitable channels.

Return on ad spend (ROAS) offers a clear and actionable way to evaluate the efficiency of advertising investments. Professionals who measure and improve ROAS can:

While ROAS isn’t the only metric that matters, its focused nature makes it indispensable for evaluating the effectiveness of advertising efforts. Whether you work in finance or marketing, understanding and applying ROAS can help you drive better financial outcomes.