Get Specialized with our Financial Planning & Analysis (FP&A) Program

Support business leaders in their decision-making with best-in-class financial models to evaluate and forecast the financial performance of a company.

Month-over-month growth helps businesses monitor performance and evaluate strategic actions

Month-over-month growth (abbreviated MoM or M/M) measures the percentage change in a specific metric from one month to the next. The month-over-month growth rate is typically a critical indicator used by businesses to understand quick changes in market conditions and operational results or to evaluate many other metrics. This calculation offers companies a clear view of their growth trajectories (or declines).

Month-over-month growth is commonly calculated in Financial Planning & Analysis (FP&A) or by other corporate finance teams and is less commonly seen in investment banking, private equity, or equity research. This is because monthly information is typically internal data only and is not usually disclosed by companies to external parties.

The formula to calculate month-over-month growth is straightforward and mastery of the calculation is expected of many finance professionals.

Alternatively, month-over-month growth can be calculated as:

The result will be a fraction, so it’s common to format the result as a percentage when using financial software like Excel.

The month-over-month growth rate allows analysts and other stakeholders the ability to quickly spot trends or deviations, allowing company management to enact strategic or operational decisions if necessary.

The month-over-month growth rate also allows professionals the ability to understand the potential cyclicality of a business. Because monthly trends, by default, include more data points than annual ones, companies can monitor and swiftly respond as overall business conditions change.

By analyzing month-over-month growth data, companies can detect short-term trends that might not be apparent from more extended periods. This makes the month-over-month growth rate particularly useful for businesses and industries that need to rapidly adapt to market changes.

The monthly growth rate is especially helpful for businesses looking to keep their fingers on the pulse of their performance. By examining the month-over-month growth rate, companies can quickly understand what’s working and what’s not, allowing decision-makers to address areas that need improvement. This agility and responsiveness are critical for maintaining or establishing a competitive edge.

Understanding month-over-month growth can also help in understanding seasonal patterns, which is necessary for businesses that experience large changes in financial results due to seasonality.

Seasonality is a characteristic where there are predictable large upturns or downturns depending on the time of the year. The most obvious example of seasonality is the retail industry. In retail, consumers tend to spend a lot more money during specific periods like the holiday season (e.g., Christmas in North America).

For businesses subject to seasonal fluctuations, understanding month-over-month growth can help in forecasting production, inventory, and staffing requirements. A pattern in monthly growth rates helps in developing marketing plans and building inventory levels to meet higher anticipated demand during the “busy season.”

Targets based on the MoM growth rate provide actionable insights and specific benchmarks that can be used to motivate teams and align efforts across any organization.

Clear, measurable targets are vital for driving business performance. Month-over-month growth rates provide a key performance indicator (KPI) that can be used across different departments or other job functions, allowing for performance assessment and outcome management.

Month-over-month growth is also important for startups, as well as companies that are currently experiencing distress.

Startups can use monthly growth metrics to evaluate whether the offered products are gaining traction with customers. Month-over-month growth rates may be used to validate the market acceptance of new products or services. An increasing growth rate in metrics like sales or active users indicates whether the market is responding positively to the products or services.

Distressed companies need monthly data points to see if the business is improving or continuing to deteriorate. Understanding this is vital for strategic planning and making decisions about potential cost-cutting or attempts to improve revenue or profitability. Month-over-month metrics help distressed companies prioritize the aspects that are most critical to immediate survival and long-term recovery.

Example 1: Calculate the month-over-month growth rate for an e-commerce company

The management team of an e-commerce company wants to understand how effective a recent advertising campaign was. Based on sales data for May and June, calculate the month-over-month growth rate:

May sales: $110,000

June sales: $125,000

The MoM growth rate is 13.6% [(125000 − 110000) ÷ 110000].

Interpretation: The e-commerce company experienced a 13.6% increase in sales from May to June, indicating a positive impact from the advertising campaign.

Example 2: Calculate the month-over-month growth in monthly active users for a mobile app

The developers of a mobile app want to better understand user engagement and retention. To do so, the developers want to calculate the percentage growth in users from November to December.

November monthly active users: 5,500

December: 7,200

The growth rate is 30.9% (7200 ÷ 5500) – 1.

Interpretation: The developers see a 30.9% increase in monthly active users from November to December, suggesting successful user engagement strategies or effective implementation of new features.

The month-over-month growth rate can also be applied to months that are not consecutive. In this case, analysts might want to calculate the compound monthly growth rate (CMGR). This calculation is similar to the more-familiar compound annual growth rate (CAGR). Instead of taking the simple average of monthly growth rates, the CMGR takes into account the effect of compounding.

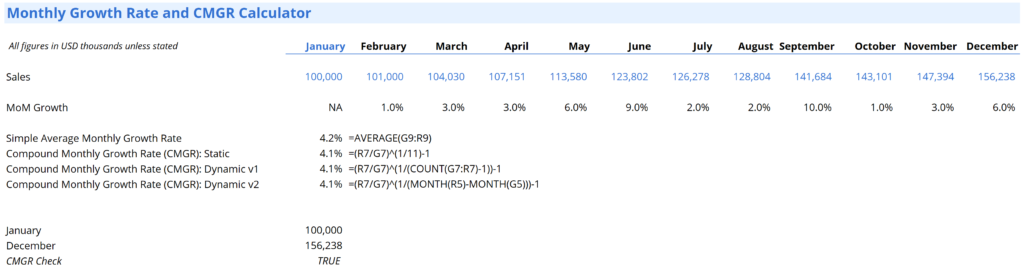

For example, suppose a company has monthly sales data from January to December, as shown in the screenshot below.

The compound monthly growth rate is 4.1% (156,238 ÷ 100,000) ^ (1/11) – 1. We use 11 months in the exponent instead of 12 months since we want the growth rate from January to December, which is actually 11 months. We would use 12 months if we were calculating the growth rate from December to December (which would technically be an annual growth rate). Note that the compounding monthly growth rate is slightly different than the simple average of 4.2%.

One disadvantage of the compound monthly growth rate is that it assumes growth to be constant over the measured time horizon. In essence, the CMGR smooths the actual results, and actual results may differ from month to month.

Complete the form below to download our free Monthly Growth Rate and CMGR Calculator!

While the MoM growth rate offers more timely feedback, other metrics like year-over-year (YoY or Y/Y) growth provide insights into longer-term trends and is less susceptible to short-term fluctuations.

The month-over-month growth rate, when compared to the annual growth rate or compounded monthly growth rate, provides a more immediate understanding of dynamics but must be interpreted within the right context. It’s crucial for businesses not to rely solely on this metric but to use it alongside others like YoY growth and the CMGR to obtain a more comprehensive view of performance over time.

Analyzing MoM growth involves looking at not just the percentage changes but also the underlying reasons behind why these changes occurred. Like many metrics, it’s essential to consider external factors like economic conditions and competition, as well as internal factors like changes in marketing spend or new product launches.

To effectively analyze growth data, it’s essential to dive into the underlying causes of change. This may involve looking at monthly data across various business units and diving deeper into specific days or events that impacted the growth rates.

Businesses use the month-over-month rate to evaluate revenue, expenses, advertising campaigns, and inventory management, among many other uses. For example, a significant increase in monthly users could prompt further investment in user acquisition strategies.

Below are some examples of using month-over-month growth.

For e-commerce businesses, MoM growth can directly influence marketing and sales strategies. If a specific product line experiences significant growth, the business can allocate more resources to promoting that line and acquiring customers. In contrast, if a product line exhibits declining or negative growth, then analysts should investigate potential issues like pricing or product quality.

Retail businesses can use MoM growth to better manage inventory. By understanding which products are gaining (or losing) popularity and at what rate, inventory purchasing can be adjusted to meet demand without overstocking. Additionally, staffing levels often correlate with sales volume; the MoM growth rate can help predict appropriate staffing requirements during both peak and off-peak times.

Hotels and tourism-based businesses benefit from analyzing monthly growth in bookings to optimize marketing strategies and pricing. For example, if there’s a significant increase in bookings month over month, a hotel might consider raising rates or offering premium packages to capitalize on the increased demand.

One of the main challenges of using MoM growth is its sensitivity to short-term fluctuations, which can potentially lead to misleading conclusions without considering broader trends.

Because of these short-term fluctuations, it’s important to use this metric in conjunction with longer-term KPIs. Additionally, external conditions like economic downturns or unexpected market events can disproportionately impact monthly calculations, leading to potentially skewed data and conclusions.

Improving MoM growth can be approached by focusing on strategies that drive consistent improvements, like optimization of marketing efforts or improving customer service to increase customer retention.

Agile businesses use MoM growth as part of continuous improvement. Monthly growth calculators can regularly monitor performance and identify areas for immediate improvement. Strategies like A/B testing can aid in understanding what impacts MoM growth either positively or negatively.

Month-over-month growth is a powerful metric that, when used wisely, provides significant insights into a company’s short-term performance over time. However, it doesn’t tell a complete story and should be used in conjunction with other metrics to provide a more comprehensive picture of a company’s health and growth trajectory.

MoM growth is indispensable for businesses that need to remain agile and responsive. However, it’s important to remember to interpret MoM figures within the broader context of other metrics and market conditions. By doing so, companies can ensure they leverage MoM growth insights effectively to foster sustainable business growth.

Thank you for reading CFI’s guide on Month-Over-Month Growth. To keep advancing your career and skills, the following CFI resources will be useful: