Get In-Demand Finance Certifications

AI and Finance Jobs: How AI is Reshaping Careers in Finance

AI and Finance Jobs: Making AI Work for Your Career

Whether you’re just starting your career in finance or have years of experience, one thing is clear — AI is changing the way finance professionals work. But this isn’t about jobs disappearing. It’s about new opportunities, smarter workflows, and future-proofing your career in a rapidly evolving field.

Understanding how AI is reshaping finance jobs can help you stay ahead. From automating repetitive tasks to enhancing decision-making, AI is shifting the role of finance professionals toward more strategic, high-value work. The question isn’t whether AI will impact finance jobs — it already is. The real question is: How can you make AI work for your career?

Key Highlights

- Finance jobs are evolving into AI-augmented roles that require both AI literacy and domain expertise.

- AI and finance jobs create new career paths like AI auditors and compliance specialists, investment analysts, and product managers.

- To stay competitive, develop AI skills, gain experiences by applying AI to your workflow, and remain proactive in your learning journey.

AI Automation in Finance Jobs

Many manual, repetitive tasks in finance are now being handled by AI. Processes that once took hours can now be completed in minutes with AI-powered automation. Here are some areas where AI is having the biggest impact:

- Data entry and reconciliation: AI can extract data from financial documents and reconcile transactions with high accuracy.

- Customer service: AI chatbots handle routine banking and financial inquiries, reducing the need for human agents.

- Fraud detection and compliance monitoring: AI continuously analyzes transactions in real time to flag suspicious activity faster than human analysts.

- Loan underwriting and credit risk assessment: AI models evaluate loan applicants with greater precision, considering thousands of data points beyond traditional credit scores.

For finance professionals, this shift means less time spent on administrative tasks and more focus on strategic, high-value work. Instead of manually reviewing financial statements, professionals can interpret AI-generated insights and provide deeper analysis.

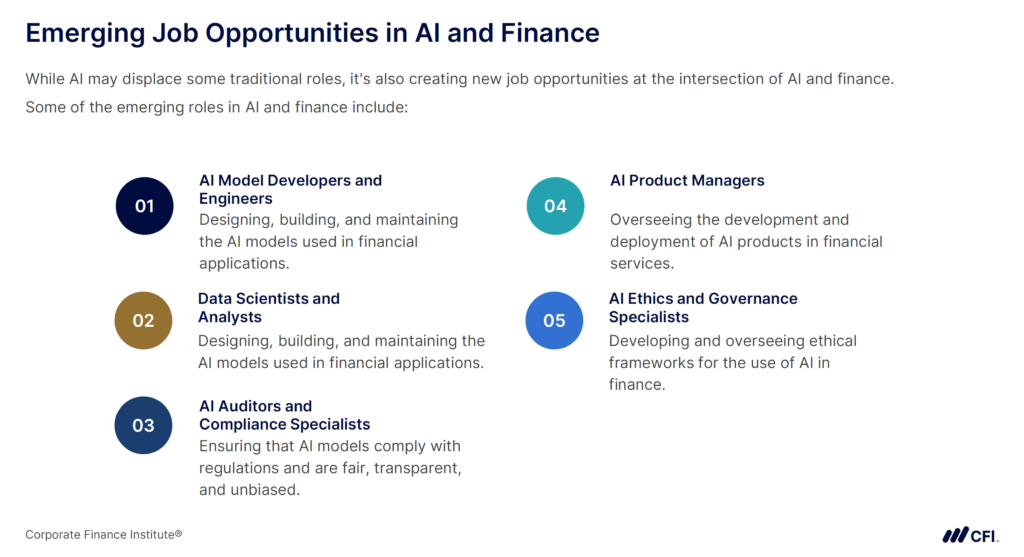

AI Creates New Job Opportunities

Rather than replacing professionals, AI is enhancing their capabilities. Finance roles are evolving to integrate AI-driven tools, creating new career opportunities for those who understand how to leverage them. Some key roles that are growing in importance include:

- AI model developers and engineers: Building AI-powered financial models, predictive analytics tools, and trading algorithms.

- AI auditors and compliance specialists: Ensuring AI systems are fair, unbiased, and in compliance with financial regulations.

- AI-enhanced investment analysts: Using AI to analyze market trends, economic indicators, and risk factors to make more informed investment decisions.

These AI finance job examples shift the role of finance professionals to decision-makers who interpret AI-driven insights. This change means that you will be expected to apply your expertise to guide AI systems rather than simply rely on them.

Why AI and Finance Jobs Now Require Hybrid Skills

The ability to work with AI-driven tools is becoming a key differentiator in finance careers. Simply understanding financial principles is no longer enough — professionals must also be able to interpret AI-generated insights and apply them to complex financial decisions. This demands a blend of technical fluency and strategic thinking to translate AI outputs into actionable business intelligence.

To build this skill set, finance professionals should focus on:

- Data analysis and AI-driven decision making: Understanding how AI processes financial data and generates insights.

- Financial modeling with AI: Using AI-powered forecasting and scenario planning tools for risk assessments.

- AI ethics and governance in finance: Addressing bias, transparency, and fairness in AI-powered decision making.

AI in finance provides better tools for professionals to make faster, more accurate decisions. Those who develop these skills will be well-positioned for the future.

Why Human Oversight Still Matters in AI-Driven Finance

AI can analyze vast amounts of data, but it lacks human intuition, contextual awareness, and ethical reasoning. This is why human oversight remains essential in financial decision making.

For instance, an AI model may flag unusual financial transactions, but a compliance officer determines whether the case requires further investigation. Similarly, AI can recommend investment allocations, but portfolio managers weigh additional factors, such as economic trends and client risk tolerance, before making final decisions.

With the increasing use of AI in finance, new career paths are emerging in AI governance, compliance, and model validation, ensuring that AI-driven systems align with regulatory and ethical standards.

How to Future-Proof Your Finance Career in an AI-Powered World

To make sure your skills stay relevant in the finance industry, actively build AI-related skills and integrate AI-driven tools into your work.

Here’s how you can stay ahead:

- Develop AI-related finance skills: Invest in courses that teach practical skills in using AI for financial analysis, modeling, data analytics, and risk assessment.

- Understand how AI tools work: Learn the basics of machine learning models used in fraud detection, portfolio management, and financial forecasting.

- Develop a mindset of continuous learning: AI technology evolves rapidly — staying informed will keep your skills relevant.

- Use AI to enhance, not replace, your expertise: AI can speed up analysis, but professionals must provide the strategic thinking behind the numbers.

Companies are actively investing in AI training programs for their finance teams, recognizing that a workforce fluent in AI can drive better business outcomes. Professionals who take the initiative to upskill will have an advantage in the job market.

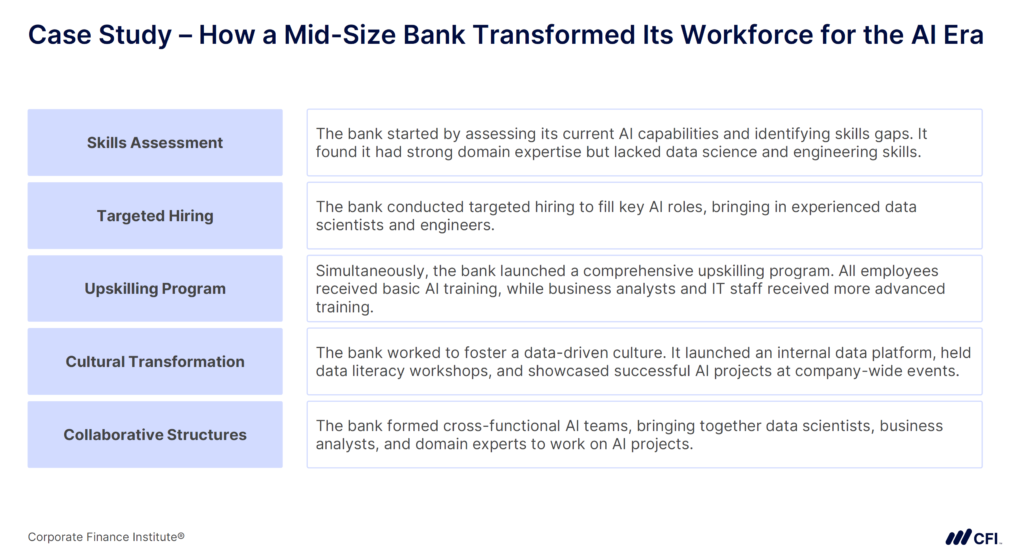

How a Mid-Size Bank Adapted to AI Without Downsizing

A mid-size European bank faced the challenge of integrating AI into its financial operations without eliminating jobs. Instead of automating roles and downsizing staff, the company invested in AI training programs and reskilled employees.

- Employees received training in AI-enhanced risk management, financial modeling, and compliance monitoring.

- Cross-functional AI teams were formed, bringing together data scientists, business analysts, and financial experts.

- Efficiency improved significantly, and employees were able to transition into higher-value roles that required AI-driven decision-making.

The lesson for employers? AI adoption does not have to result in job loss. Instead, financial institutions that embrace AI training and workforce transformation will retain top talent and become more competitive.

AI and Finance Jobs: Develop AI Skills to Stand Out

The effect of AI on finance jobs reshapes how finance professionals analyze markets, investments, and the financial performance of businesses. Finance roles are shifting from manual reporting and reconciliation to workflow automation, data interpretation, and enhanced insights that guide decision-making.

Those who understand AI’s strengths and limitations will take on more strategic, high-impact roles, from optimizing investment decisions to designing risk models that adapt in real time. Employers need professionals who don’t just apply AI insights blindly but critically assess them, ensuring that financial decisions remain accurate, fair, and well-informed.

Ready to build hands-on skills to excel in AI and finance jobs? CFI’s AI for Finance Specialization equips you with practical, industry-relevant skills to integrate AI into modern finance workflows. By the end of the program, you’ll be ready to thrive in finance roles that demand AI innovation and technical expertise.

Earn Your AI for Finance Specialization!

Additional Resources

AI and Financial Statement Analysis: Tools and Techniques

How AI Transforms Scenario Analysis in Corporate Finance

0 search results for ‘’

People also search for:

excel

power bi

esg

accounting

balance sheet

fmva

real estate

Explore Our Certifications

Resources

Popular Courses

Recent Searches