Get Specialized with our Financial Planning & Analysis (FP&A) Program

Support business leaders in their decision-making with best-in-class financial models to evaluate and forecast the financial performance of a company.

As an FP&A professional, strategic financial planning is one of the most valuable skills you can develop. It goes beyond budgeting and forecasting, ensuring that a company’s financial strategy aligns with long-term business goals and supports real decision-making.

You may already understand FP&A’s core role — analyzing financial data to help leadership make better decisions. But how do you translate strategy into measurable goals? How do financial plans connect to daily business operations?

This guide covers the fundamentals of strategic financial planning, including the strategy pyramid, which breaks down corporate goals into actionable steps, and strategic financial mapping, which links business decisions to financial outcomes.

In a company’s annual or quarterly report, the leadership team outlines the strategic plan for the business in the Management Discussion and Analysis (MD&A) section. However, within a company, strategic financial planning extends beyond a high-level vision.

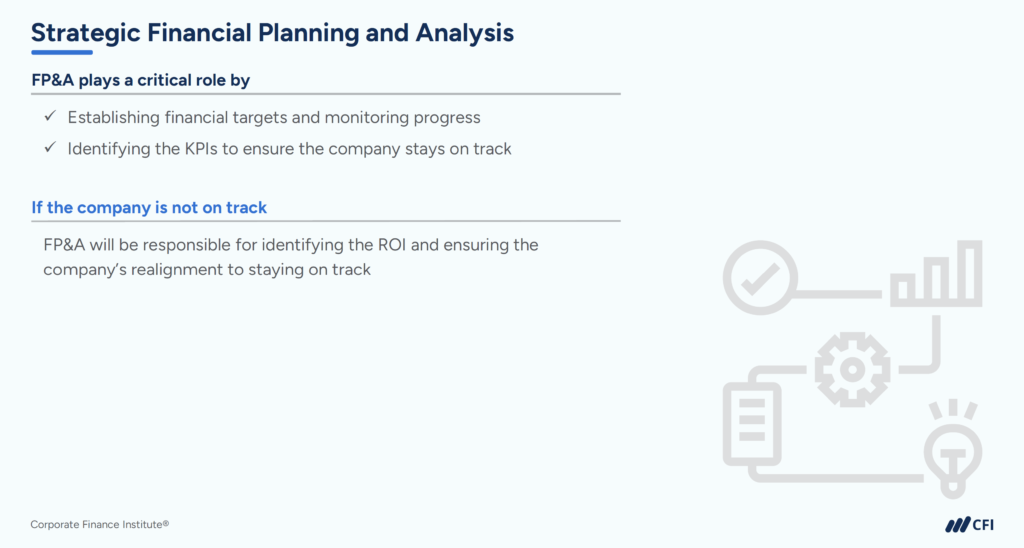

Strategic financial planning focuses on turning a leadership team’s high-level vision into an actionable financial roadmap that guides decision-making. For FP&A professionals, this means:

Unlike short-term budgeting, strategic financial planning takes a long-term approach — typically spanning three to five years. FP&A teams break down these plans into quarterly or monthly targets, ensuring that financial strategy translates into measurable progress.

One of the most effective ways to think about strategic financial planning is through the strategy pyramid. The strategy pyramid approach translates corporate goals into clear, measurable financial and operational objectives.

Suppose you work in FP&A for a manufacturing company that produces external hard drives, solid-state drives, and flash drives. Executive leadership presents an updated strategic plan with the following components:

FP&A’s Role:

However, setting financial objectives is only part of the equation. FP&A professionals must go a step further by connecting financial outcomes to the operational drivers, a process called strategic financial mapping.

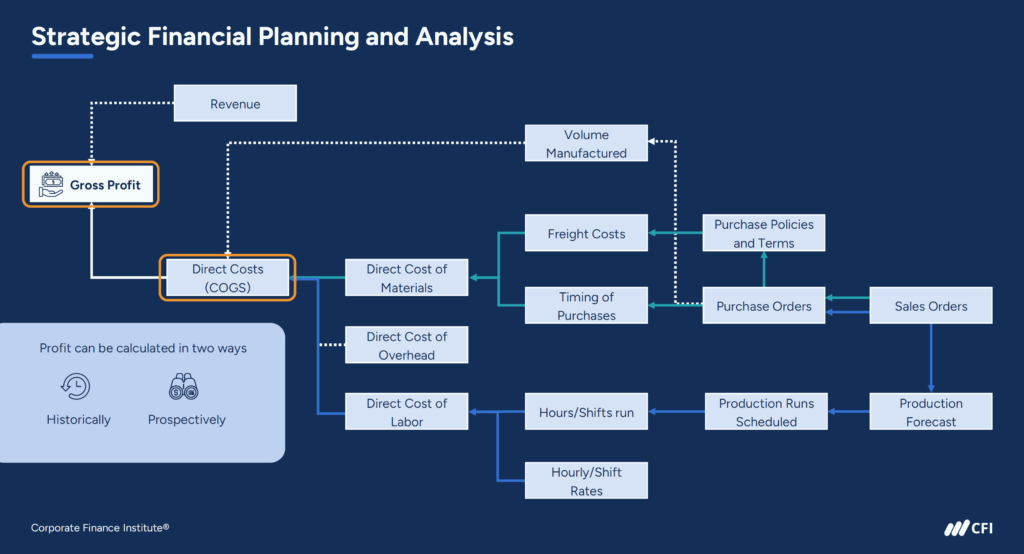

How do those actions set in the strategic pyramid impact financial performance? The answers lie in strategic financial mapping. This approach allows FP&A professionals to trace financial outcomes back to operational decisions and determine the source of a financial discrepancy.

Strategic financial mapping begins with a key financial metric and works backward to uncover the underlying drivers that influence it. For example, a manufacturing company’s gross profit (calculated as Gross Profit = Revenue – Direct Costs) can be analyzed in two ways:

While revenue is influenced by external factors like pricing and customer demand, direct costs (COGS) are within the company’s control. Managing these costs effectively is key to improving gross profit and overall financial performance.

To optimize direct costs, the FP&A team must identify the operational drivers behind cost fluctuations. For this manufacturing company, two key drivers of costs include:

| Freight | Purchase policies and sales orders. | Poor timing or misaligned agreements led to higher shipping expenses. | The increase in COGS drove lower gross profit. |

| Materials | Dependent on supplier pricing agreements and purchasing timing. | Misalignment between procurement and forecasted demand resulted in overpaying for raw materials. | The increase in COGS drove lower gross profit. |

By using strategic financial mapping, the FP&A team identified the sources of higher COGS and used this data to recommend solutions to improve gross profit. The further back you trace these cost drivers, the more you can see how operational decisions impact financial performance.

Effective strategic financial planning ensures that financial targets are not set in isolation. Every forecast, budget, and investment decision must be grounded in data and aligned with the company’s long-term strategy. As an FP&A professional, you play a critical role in translating financial plans into real-world execution.

The FP&A work doesn’t stop once forecasts are set. You need to continuously monitor performance, adjust projections, and guide leadership on key financial trade-offs. Here’s how you can turn financial strategy into action:

| Align Financial Targets with Business Strategy | Establish clear, measurable financial targets that support strategic objectives. | ✅ Define KPIs for revenue growth, cost control, and profitability. ✅ Ensure department budgets align with corporate financial goals. ✅ Build financial models to test assumptions about key drivers like sales volume, pricing, and supply-chain costs. |

| Monitor Financial Performance and Adjust Plans Proactively | Financial plans need to be continuously updated to reflect real business conditions. | ✅ Track actual vs. projected performance and analyze variances. ✅ Identify early warning signs of financial risks, such as cost overruns or declining margins. ✅ Update forecasts regularly using rolling projections to keep financial plans aligned with market realities. |

| Use Scenario Planning to Prepare for Uncertainty | Anticipate risks and opportunities by modeling multiple financial outcomes. | ✅ Develop best-case, base-case, and worst-case financial models. ✅ Simulate how changes in revenue, costs, or investment decisions impact profitability. ✅ Provide actionable insights to help leadership navigate market shifts and economic uncertainty. |

| Advise Leadership on Data-Driven Decision Making | Translate financial insights into strategic recommendations for leadership. | ✅ Recommend adjustments to resource allocation, capital investments, and cost management strategies. ✅ Present insights through data visualizations and executive summaries. ✅ Collaborate across departments to align financial and operational strategies. |

If you’re serious about building a career in FP&A, mastering strategic financial planning is a must. It’s what separates top-tier FP&A professionals from those who simply report numbers.

Understanding how to map financial goals to business strategy, analyze cost drivers, and adjust financial plans based on performance will make you an indispensable asset to any company.

Ready to take your FP&A skills to the next level? Explore CFI’s courses tailored for FP&A professionals and start building the expertise you need to excel in strategic financial planning.

How to Analyze Budget Variances with 10 Essential Questions