Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

ROA (Return on Assets) and ROE (Return on Equity) are two distinct financial ratios that measure a company’s performance from different angles. While both use net income as their starting point, they provide financial analysts with separate perspectives:

Both ROA and ROE use the same starting point: net income, the company’s bottom-line profit reported on the income statement.

But each ratio compares that profit to a different figure on the balance sheet — total assets for ROA and shareholders’ equity for ROE — giving you two distinct perspectives in evaluating returns.

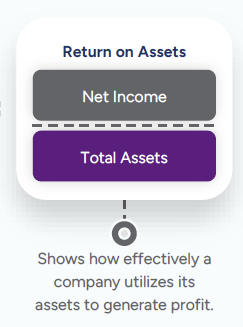

ROA measures how efficiently a company uses its total assets to generate profit. Financial analysts typically use ROA to assess performance over time or compare companies within the same industry.

When comparing ROAs across different companies, consider the scale of their businesses and the nature of their operations. For example, the average ROA for retailers tends to be lower than less capital-intensive sectors, such as SaaS and subscription-based companies.

To calculate a company’s ROA, use this formula:

ROA = Net Income ÷ Total Assets

Let’s compare two fictional companies in the same industry: Bluehill Retail and Maple & Co., both mid-sized general merchandise retailers.

Both companies are profitable, but Maple & Co. is generating more profit per dollar of assets, suggesting it uses its resources more efficiently. You might conclude that Maple & Co. has tighter asset management — perhaps it carries less excess inventory or turns over fixed assets more effectively. But you want to calculate ROE before making any conclusions.

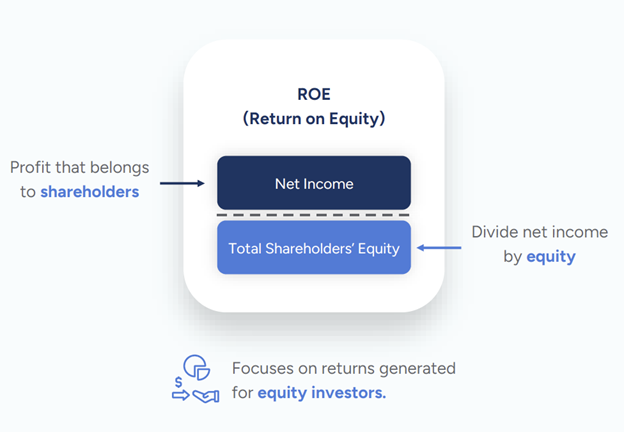

ROE measures how effectively a company utilizes shareholders’ capital to generate profits. A higher ROE indicates better strong profitability and greater return on shareholders’ investment.

To calculate a company’s ROE, use this formula:

ROE = Net Income ÷ Shareholders’ Equity

Now let’s look at how those profits translate into shareholder returns.

Here’s where it gets interesting: even though Maple & Co. has a higher ROA, Bluehill delivers a higher ROE. Bluehill’s has higher debt relative to equity. This debt boosts its ROE, i.e., shareholder returns, by reducing the amount of equity required — although higher debt also increases financial risk.

| Net Income | ||

| Total Assets | ||

| Shareholders’ Equity | ||

| Debt | ||

| ROA | ||

| ROE | ||

| Capital Structure | More leveraged (40% debt) | Less leveraged (20% debt) |

| Key Insight | Higher ROE due to more debt than equity. | Higher ROA from effective use of assets to drive earnings. |

While debt isn’t part of the ROE formula, it can still influence the outcome. The difference highlights why both ratios matter. ROA helps you evaluate overall performance across the business. ROE helps you assess how that performance translates into value for equity investors.

Understanding what each ratio compares profit to — assets versus equity — reveals important distinctions in how they should be interpreted and applied in financial analysis:

| Applicable Financial Statements | Income Statement + Balance Sheet (Assets) | Income Statement + Balance Sheet (Equity) |

| Formula | Net Income ÷ Total Assets | Net Income ÷ Shareholders’ Equity |

| Focus | How well a company uses its total assets to drive profitability. | How much profit a company generates for its shareholders. |

| Viewpoint | Company-wide perspective — value creation from efficient use of assets. | Shareholder perspective — value creation from investor capital. |

| Capital Structure Impact | Less affected by debt levels. | Significantly influenced by debt-to-equity ratios. |

| Industry Considerations | Asset-intensive industries typically have lower ROAs. | Can be high in companies with minimal equity. |

| Risk Assessment | Provides insight into operational efficiency. | Helps evaluate financial risk and shareholder returns. |

These complementary metrics work best when analyzed together, providing a more comprehensive view of a company’s financial health and performance strategy.

Understanding the difference between ROA and ROE is just one piece of the financial analysis puzzle. World-class financial analysts connect the dots between performance metrics, business strategy, and investor outcomes. That kind of insight takes practice, structure, and the right tools.

CFI’s Financial Modeling & Valuation Analyst (FMVA®) certification is one of the most recognized programs for learning financial modeling skills. It’s designed for professionals pursuing careers in investment banking, equity research, FP&A, corporate finance, and related fields. Over 75% of CFI learners report significant career advancement within months of program completion.

The FMVA program provides the structured path and hands-on training you need to build real-world modeling skills and apply them with confidence in any corporate finance environment.

Financial Ratios Definitive Guide