Get Certified for

Business Intelligence (BIDA®)

Develop analytical superpowers by learning how to use programming and data analytics tools such as VBA, Python, Tableau, Power BI, Power Query, and more.

Your creditworthiness. Your insurance premium. Your ability to buy a home. AI models influence all of these decisions — but are they making them fairly? AI ethics in finance is about ensuring that AI-driven decisions uphold fairness, transparency, and accountability.

When AI models inherit biases from flawed data or poorly designed algorithms, they can unintentionally discriminate, restricting access to financial services and triggering compliance penalties. Preventing bias requires more than adopting AI — you must actively monitor, refine, and ensure transparency in AI-driven decisions.

This guide explores the sources of AI bias, its risks, and the best practices to detect and prevent bias before it becomes a liability.

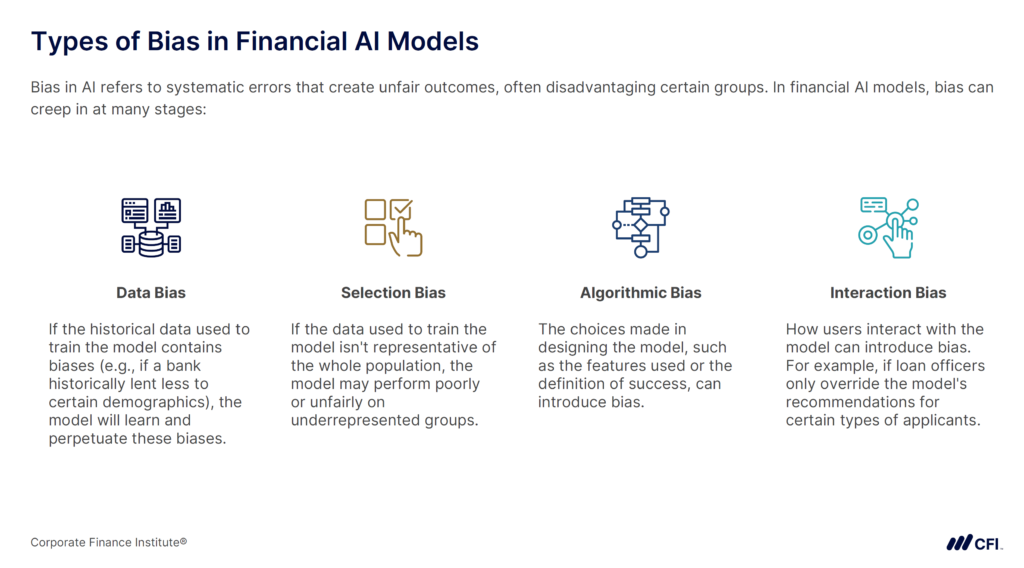

AI models don’t operate in a vacuum. They learn from historical financial data, which often reflects human biases.

Without intervention, AI can amplify patterns of inequality, reinforcing past discrimination rather than eliminating it. Bias can emerge from how data is collected, which variables are prioritized, or how models weigh certain factors in decision-making.

| Historical Bias | When past inequalities are embedded in training data. | If a bank historically approved more loans for certain demographics, an AI-driven credit scoring model may learn to favor those groups over others. |

| Selection Bias | When training data is not representative of the population AI serves. | If an AI algorithm is trained only on high-income borrower data, it may unfairly assess risk for applicants with non-traditional income sources. |

| Algorithmic Bias | When AI assigns undue weight to specific variables, leading to skewed outcomes. | If an AI model overemphasizes zip codes in lending decisions, it could result in geographic discrimination that disproportionately affects marginalized communities. |

| Interaction Bias | When users interact with an AI model in a way that introduces bias to it. | If loan officers constantly override the model’s recommendations for certain types of candidates, it could result in excluding people from certain groups. |

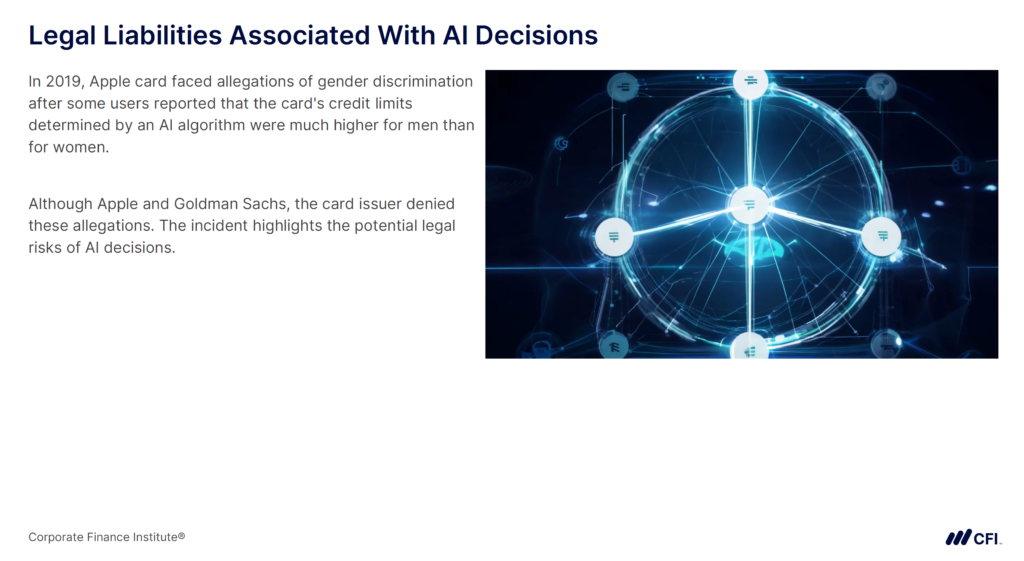

In 2019, Apple and Goldman Sachs faced public scrutiny after reports surfaced that Apple Card’s AI-driven credit limit decisions were biased against women. Some customers found that men were approved for significantly higher limits than women, despite similar financial backgrounds.

Goldman Sachs was later cleared of the allegations, but the controversy underscored a critical issue. Even when AI bias is unintentional, it can still create unfair outcomes if models are not rigorously tested and monitored.

When AI models favor traditional credit histories, they may exclude entrepreneurs, gig workers, and immigrants who don’t fit conventional profiles, limiting access to essential financial services.

A single high-profile AI failure can erode public trust in a financial institution. When AI bias makes headlines, financial institutions face media scrutiny, investor skepticism, and long-term brand damage.

Regulators are cracking down on AI-driven discrimination in finance. Several major regulations set clear fairness and transparency requirements:

The financial consequences of biased AI extend beyond regulatory fines. Companies that fail to ensure fairness in AI models face legal action and costly settlements.

In 2023, iTutorGroup, a global online education company, faced a lawsuit from the U.S. Equal Employment Opportunity Commission (EEOC). Its AI system excluded thousands of applicants based solely on their age, violating the Age Discrimination in Employment Act (ADEA). The company ultimately settled the case, but it marked one of the first high-profile legal actions against AI-driven discrimination.

This case serves as a warning for both financial institutions and non-financial organizations. Regulators and courts are holding companies accountable for AI bias. Those that fail to address fairness face lawsuits, financial penalties, and lasting reputational damage.

Addressing AI ethics in finance requires proactive measures to reduce bias and ensure fair decision-making. Simply deploying an AI model isn’t enough — you must continuously assess whether it treats all applicants, customers, or stakeholders fairly.

Below are key strategies to detect and prevent AI bias in finance.

Bias often originates in the data used to train AI models. If your AI system is trained on historically biased financial data, it will likely replicate those biases unless proactive measures are taken to correct them.

To avoid this, you must carefully evaluate whether your data reflects the full spectrum of individuals it is meant to serve by:

Even if an AI model does not explicitly use race, gender, or other protected attributes, it can still learn to discriminate indirectly.

Some features used in AI models — such as ZIP codes, education levels, or employment history — can indirectly signal protected characteristics. This may lead to unintended bias in AI-driven decisions. To minimize this risk:

For example, an AI-powered credit-scoring system might place too much weight on employment gaps. This factor can unfairly penalize women who have taken career breaks for caregiving.

Identifying and adjusting these model inputs ensures that AI-driven decisions are truly reflective of an applicant’s creditworthiness, not their demographic profile.

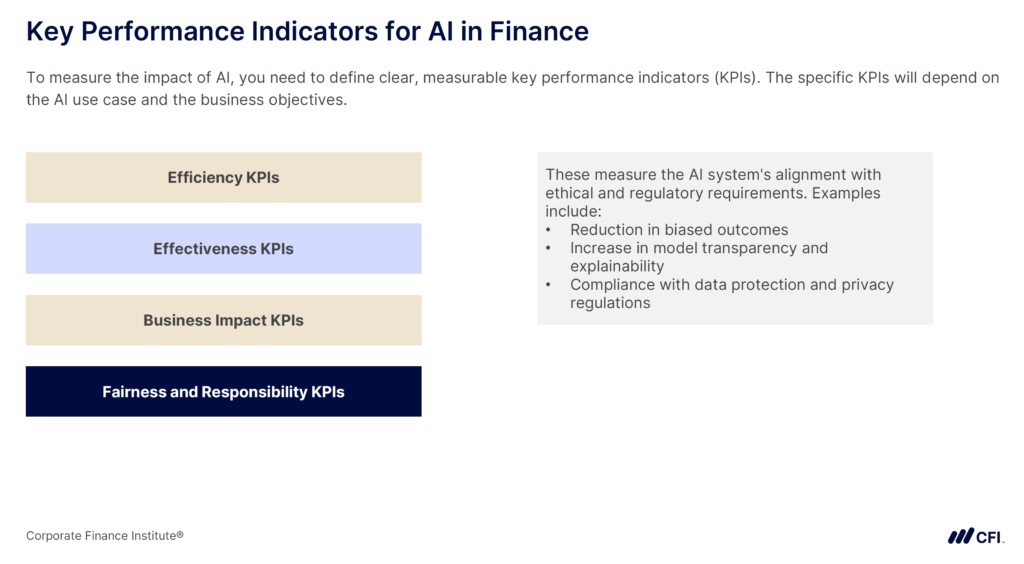

Never assume that an AI system is fair and ethical. You need key performance indicators (KPIs) to verify that your models produce equitable results across different demographic groups. Financial institutions should regularly test their AI models using fairness metrics to detect disparities.

Examples of key fairness metrics include:

By integrating fairness testing throughout the AI model’s lifecycle, you can catch and correct bias before it leads to harmful real-world consequences.

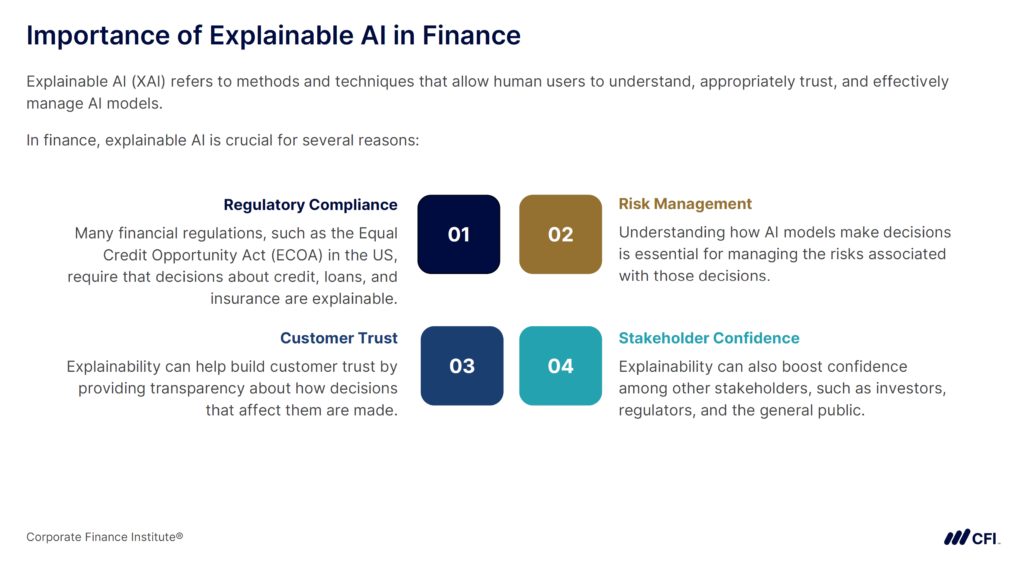

AI models should not operate as black boxes, especially when they make high-stakes financial decisions that affect people’s livelihoods. If a financial institution cannot explain why an AI system denied a loan or flagged a transaction as suspicious, both customers and regulators will question the fairness of the system.

Explainable AI enhances transparency by:

Even with the best technology, AI cannot replace human judgment in financial decision-making. Human oversight is essential to ensuring that AI operates fairly and ethically. Without human review, AI models can develop biases that go unchecked until they cause significant harm.

To maintain ethical accountability:

For example, financial institutions that use AI for loan approvals should have trained loan officers to review borderline cases, ensuring that AI-driven rejections aren’t based on biased model assumptions.

By combining AI efficiency with human judgment, financial institutions can create more ethical and trustworthy financial systems.

AI ethics in finance requires professionals and institutions to take an active role in building trust, reducing bias, and ensuring fair decision-making. Without oversight, AI models can introduce compliance risks, reputational harm, and financial penalties. To uphold ethical AI practices, you must continuously:

Embedding these ethical principles into your AI-driven processes reduces risk and strengthens your ability to make informed and responsible financial decisions.

Ready to lead AI-driven finance decision-making? CFI’s AI for Finance Specialization gives you the practical, finance-specific AI skills to integrate into your workflows. Gain hands-on expertise in applying AI ethically in financial analysis, scenario analysis, risk management, and more!

Specialize in AI for Finance now!

AI Anomaly Detection in Finance: ChatGPT Case Studies

How AI Transforms Scenario Analysis in Corporate Finance

Preparing Financial Data for AI: Best Practices for Accuracy & Machine-Readable Statements