Get Specialized with our Financial Planning & Analysis (FP&A) Program

Support business leaders in their decision-making with best-in-class financial models to evaluate and forecast the financial performance of a company.

AI tools like ChatGPT rely on structured, machine-readable financial data to generate accurate insights. These models interpret financial statements by recognizing patterns, relationships, and trends in well-organized datasets. When data contains merged cells, inconsistent labels, or missing values, AI tools struggle to extract meaningful information, leading to errors in analysis and forecasting.

AI tools analyze historical financial statements, ratio trends, and cash flow patterns by applying advanced natural language processing and machine learning techniques. These tools can:

Poor data preparation leads to misinterpreted financial ratios, distorted earnings forecasts, and incorrect variance analysis — all of which reduce the reliability of AI-generated insights.

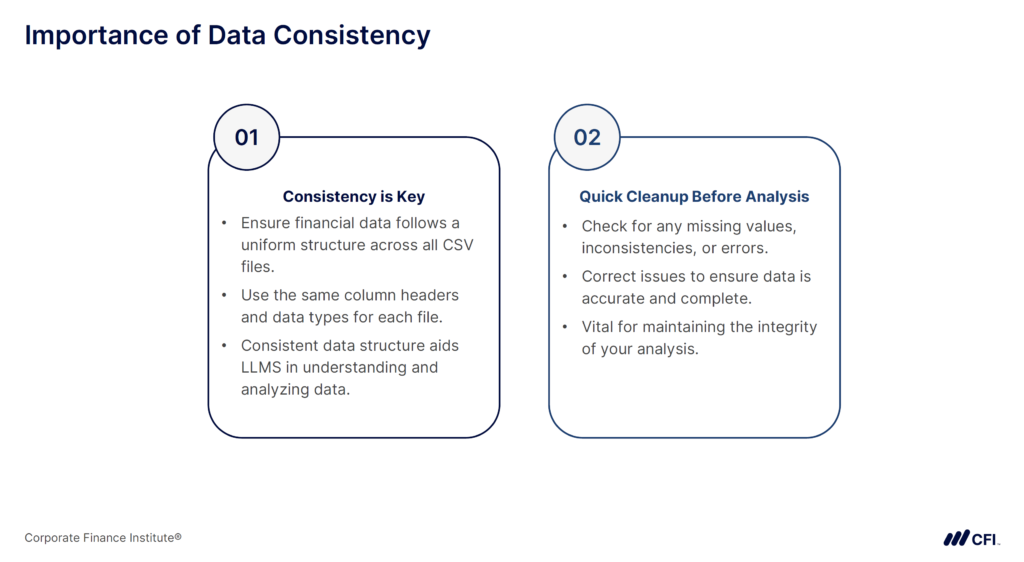

To prevent these issues, financial data must follow consistent formats, standardized column headers, and properly labeled numerical values to ensure AI can process it effectively.

To ensure AI accurately processes financial statements, follow these best practices for data preparation:

By applying these practices, financial analysts can ensure their data is clean, consistent, and AI-ready.

Let’s look at a practical example inspired by Acme Solar Technologies, a fictional company used in CFI’s Advanced Prompting for Financial Statement Analysis course.

Acme’s financial statements contained:

With clean, structured data, AI models could accurately calculate financial ratios, analyze trends, and generate precise forecasts — turning raw data into actionable insights.

Even seasoned analysts can run into data structuring issues when preparing financial statements for AI. Here’s how to avoid them:

| Unclear column headers | Use descriptive financial terms (e.g., “Net Income” instead of “Amount”). |

| Mixed data formats | Ensure all numbers are stored as numeric values, not text. |

| Inconsistent time periods | Align datasets across quarterly and annual reports for trend accuracy. |

By tackling these challenges, financial analysts can minimize AI errors and maximize analytical accuracy.

AI-driven financial analysis starts with clean, structured data. Without proper formatting, AI models risk producing misleading insights. Financial analysts who refine their data preparation processes will see significant improvements in AI-powered forecasting, ratio analysis, and strategic decision-making.

Ready to take your financial analysis to the next level with AI? Learn more in CFI’s Advanced Prompting for Financial Statement Analysis course and gain a competitive edge in financial forecasting and AI-driven insights!

Explore Advanced Prompting for Financial Statement Analysis!

AI and Financial Statement Analysis: Tools and Techniques

How AI Transforms Scenario Analysis in Corporate Finance

AI Tools for Finance: ChatGPT vs. Claude vs. Gemini