Get Certified for

Business Intelligence (BIDA®)

Develop analytical superpowers by learning how to use programming and data analytics tools such as VBA, Python, Tableau, Power BI, Power Query, and more.

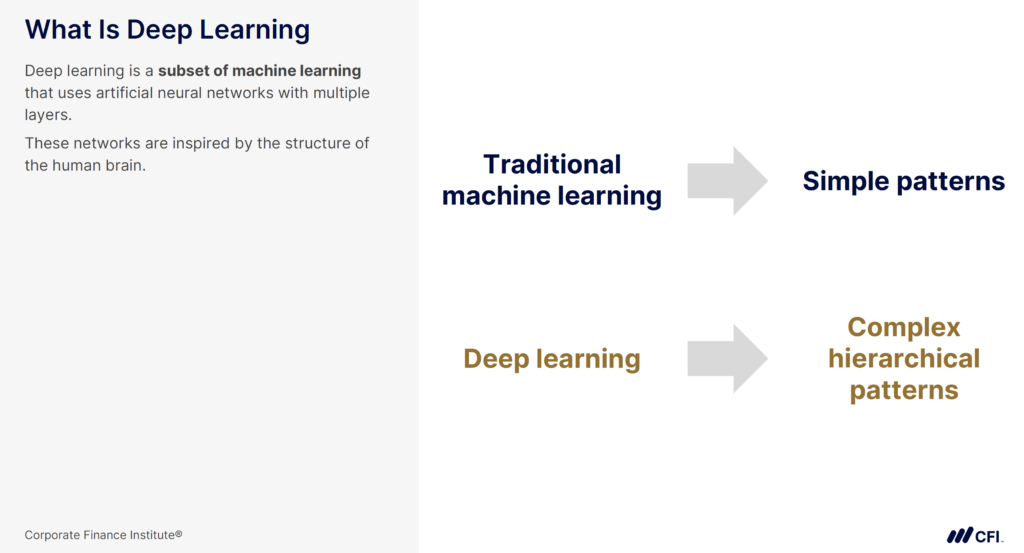

As a subset of machine learning, deep learning teaches itself patterns and relationships by analyzing vast amounts of data. Unlike traditional systems that follow pre-programmed rules, deep learning learns on its own — much like a human brain. It’s similar to how people can improve face recognition or languages with repeated exposure.

At the core of deep learning are artificial neural networks (ANNs), which help computers process information, mimicking the human brain. Just as the brain has neurons that pass signals to each other, ANNs consist of layers of interconnected nodes that analyze data one layer at a time.

Each time the model makes a prediction, it adjusts based on new data, continuously improving its accuracy.

Traditional machine learning requires human experts to decide which data features — such as revenue growth or volatility — are most relevant for making predictions. Analysts feed the model predefined inputs, which it uses to classify data or forecast outcomes. This process works well for structured financial data but struggles with unstructured data like text or images.

Deep learning, however, eliminates this manual step. Instead of relying on human-defined inputs, it processes vast amounts of raw data, detecting subtle correlations and dependencies that may be too complex for rule-based systems to detect.

In finance, this automated learning process makes deep learning ideal for:

One of deep learning’s biggest advantages is its ability to identify patterns within patterns, continuously refining its insights based on new information. This adaptability is critical in finance, where markets shift rapidly, and relying on outdated models can lead to costly mistakes.

Understanding the difference between deep learning and machine learning is just the first step. The real question is: How is deep learning actually being used in finance today?

Deep learning is already embedded in financial markets, influencing everything from trading strategies to fraud prevention. Financial institutions rely on AI-driven models to analyze massive datasets, uncover risks, and generate insights faster than ever.

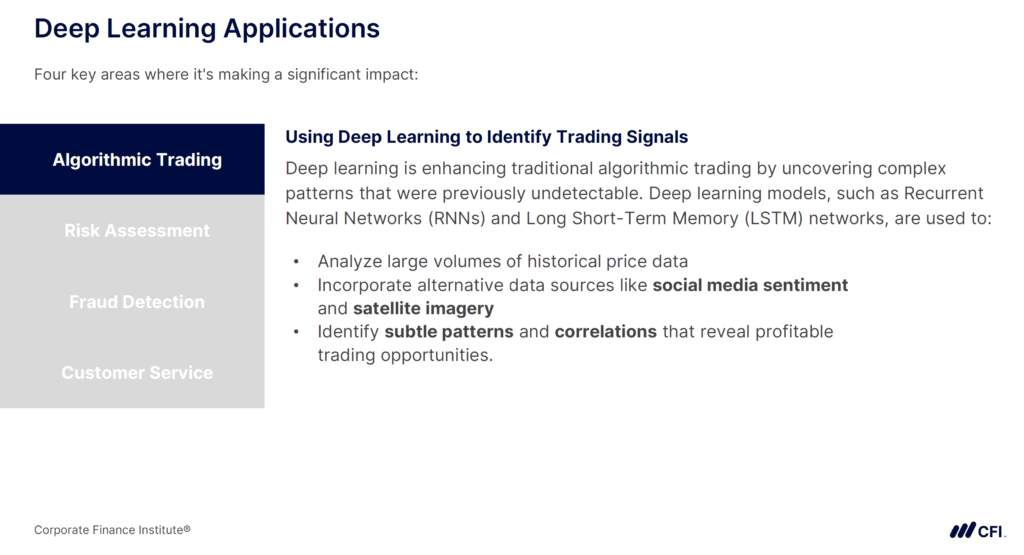

Deep learning is revolutionizing algorithmic trading by enabling financial models to process real-time market data and execute trades faster than any human. Unlike traditional quantitative models that rely on pre-set indicators, deep learning models can:

For example, a deep learning-powered trading algorithm could identify a short-term buying opportunity before competitors react. This allows firms to adjust positions instantly and capitalize on price movements.

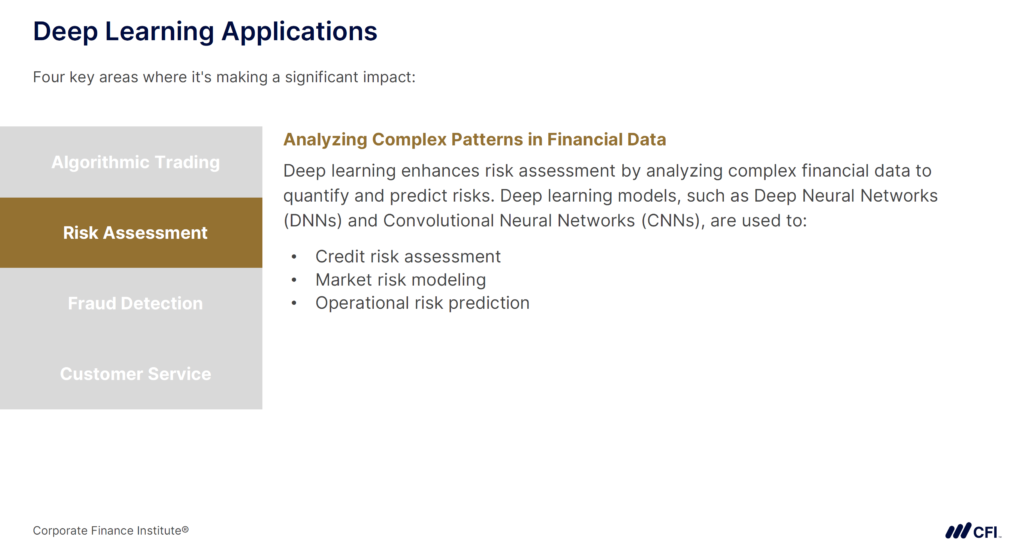

Financial institutions face a complex web of different risks that require more than traditional models to manage effectively. Deep learning strengthens institutional risk assessment by analyzing vast datasets in real time and identifying patterns that traditional models might miss. It plays a key role in:

By continuously learning from new data, deep learning enables financial institutions to anticipate risks, strengthen resilience, and make data-driven decisions with greater confidence.

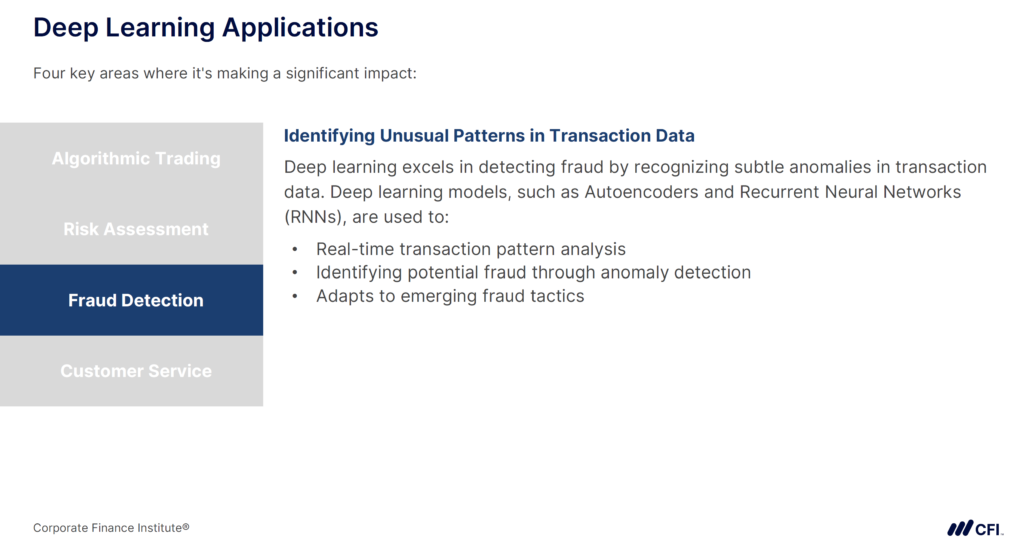

Traditional fraud detection relies on rule-based systems, which fraudsters learn to bypass. Deep learning models identify unusual transaction behaviors, even when no predefined rule applies.

For example, instead of flagging only large, unusual transactions, deep learning detects pattern shifts. For example, it could flag a customer suddenly making frequent low-value purchases across multiple accounts, a possible sign of money laundering. By continuously learning from evolving fraud tactics, these models stay ahead of emerging threats.

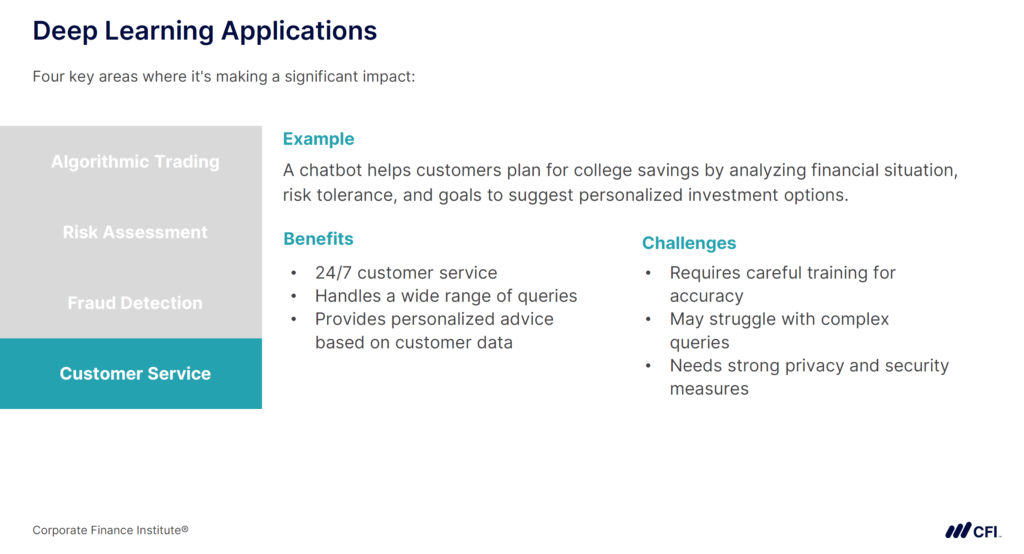

Traditional banking chatbots are rule-based, offering generic, scripted responses that often fail to answer complex financial questions. Deep learning-powered chatbots, however, can:

For instance, instead of simply displaying a user’s balance, a deep learning chatbot could analyze spending trends and income patterns to suggest personalized savings strategies. These AI assistants continuously improve with each customer interaction, making financial services more accessible and efficient.

While deep learning offers major advantages, its adoption in finance faces three key challenges: lack of transparency, data limitations, and high computational costs.

Deep learning models process thousands of variables in complex ways, making their decisions difficult to interpret. Unlike traditional models, where analysts can trace how specific inputs lead to an outcome, deep learning lacks clear explanations. This raises concerns for financial regulators and customers alike.

For example, if an AI-driven model denies a loan, it may be unclear whether credit history, spending behavior, or hidden correlations influenced the decision. Financial institutions must balance accuracy with explainability, ensuring compliance with regulatory standards like General Data Protection Regulation (GDPR). This has fueled demand for explainable AI (XAI) to make deep learning more transparent.

Deep learning models require large, high-quality datasets, but financial data is often limited, unstructured, or biased. Fraud detection models, for example, need millions of labeled transactions, yet fraud tactics evolve constantly, making past data less reliable.

Unstructured data — like news sentiment and alternative financial indicators — poses another challenge. While useful, it is difficult to structure and integrate into financial models.

Deep learning requires substantial computing power, particularly for large-scale financial applications. Unlike traditional models, which run on standard servers, deep learning relies on high-performance GPUs or TPUs, leading to high infrastructure and energy costs.

Many firms offset this by using cloud-based AI solutions, which provide on-demand computing power without the need for expensive hardware. Other strategies include model optimization techniques like pruning, quantization, and transfer learning — reducing computational demands while maintaining accuracy.

Despite these obstacles, deep learning continues to gain traction in finance due to its ability to improve risk assessment, detect fraud, and enhance decision making.

Deep learning offers a competitive edge by uncovering patterns in vast datasets, enabling faster, smarter decision-making. Deep learning, machine learning, and generative AI applications will become even more embedded in finance. Understanding and applying AI-driven tools and methods positions you to thrive now and in the future of finance.

Ready to boost your machine learning and AI skills? Explore CFI’s Foundations of Machine Learning and Deep Learning for Finance course for expert-led instruction using AI and Machine Learning methods in financial contexts.

Explore Foundations of Machine Learning and Deep Learning for Finance!

Preparing Financial Data for AI

AI Anomaly Detection in Finance: ChatGPT Case Studies