Get Certified for

Business Intelligence (BIDA®)

Develop analytical superpowers by learning how to use programming and data analytics tools such as VBA, Python, Tableau, Power BI, Power Query, and more.

Business intelligence professionals extract, analyze, and present data for specific reports or projects, creating metrics and models that help stakeholders to answer important questions.

A business intelligence (BI) analyst, also known as a data analyst, is responsible for extracting, analyzing, and presenting data for specific reports or projects. They create metrics and models that help stakeholders to answer important questions.

Their goal is to work closely with the business, to understand the drivers of performance, and produce metrics and reports that help decision makers do their jobs.

This task is generally achieved by focusing on the following areas:

Analysts require a variety of skills, ranging from technical skills such as math, basic statistics, and technical proficiency in BI tools, all the way to soft skills involving business, communication, and critical thinking.

They use these skills to understand what questions they need to ask, what data they need to use, and how to leverage that data to create insights. BI analysts are often responsible for communicating those insights to key stakeholders, so communication is essential to complete the process.

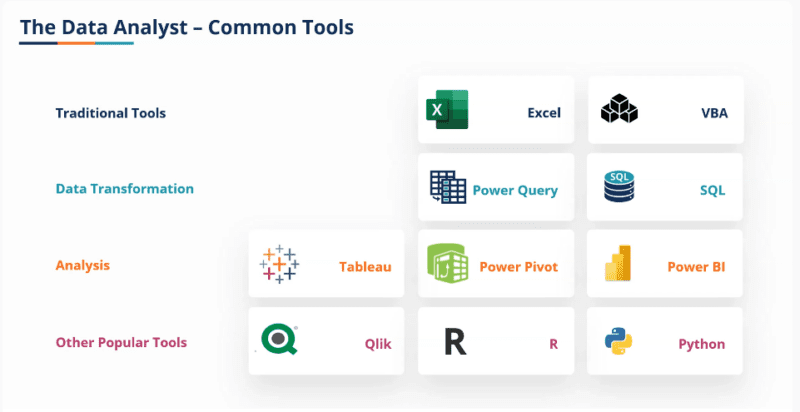

BI analysts have many tools at their disposal. Traditionally, analysts relied on Excel and VBA. However, as the field has grown and technology has progressed, many analysts now rely on the next generation of tools to boost their productivity, streamline their workflows, and produce higher quality outputs.

Power Query: For data transformation tasks, the most prevalent tools are Power Query and Structured Query Language (SQL). Power Query is an Excel add-on that seamlessly integrates, is easy to learn, and saves hours and hours.

SQL, on the other hand, is perhaps the analysts most powerful tool. This query language enables BI analysts to request data from a database in a particular format. Though it’s easy to learn and use, SQL sets its users apart from dashboard-focused BI analysts because it enables them to better understand the building blocks of data.

Once they have the data they need in the format they want, it’s time for analysis. Popular tools include Tableau, Power Pivot, and Power BI.

Power BI is the world’s leading analysis and data visualization platform. It allows users to transform data and build data models and dashboards, all in a single, easy-to-use interface.

Tableau is known for world-class visualizations, functionality that aids in metric creation and joining data from different sources, and creating data models.

Power Pivot is another Excel add-on that brings the DAX formula language and data modeling capabilities right into the heart of Excel workflows, making it a must-have for Excel users.

More advanced analysts also use coding languages like R and Python to write scripts that automate workflows, such as updating a model over time as new data becomes available.

A typical day for a business intelligence analyst involves gathering data before cleaning and processing it. They spend time coding and working with other software tools to do what they do best: generate actionable insights. Analysts often spend time meeting with others on the analytics team and sometimes need to get involved with other business stakeholders to understand business challenges and data requirements.

A business intelligence analyst will constantly be changing environment, one minute talking to the data engineering team about how data is stored in a data warehouse, the next meeting with data visualization specialists to discuss dashboard creation, or even presenting their findings to business leaders, or understanding how a business process works.

There are multiple routes to becoming a BI analyst. One of the most common tracks is pursuing a degree in a field like math, statistics, or computer science, but keep in mind that these qualifications are useful but not strictly necessary. There are also certifications, such as CFI’s Business Intelligence & Data Analysis (BIDA), that can demonstrate a candidate’s analytics prowess to a potential employer.

However, as with almost any technical role, the most important qualification will always be know-how and demonstrable project experience. Experience working in a BI analyst role is useful, though a candidate who can demonstrate successful projects in SQL, Power BI, Tableau, and Excel as well as industry-specific knowledge should be able to find a good job because demand for analysts is high.

An average BI analyst can expect to earn about twice as much as a data entry professional, though not quite as much as a data scientist salary or data engineer salary.

That said, pay for analysts positions does scale well with experience. A senior data analyst with five or more years of experience can easily command a six-figure salary, while a principal data analyst can earn even more. This makes becoming a BI analyst a smart long-term move, especially for motivated individuals who want to continue to expand their technical skill sets.

Overall, BI analysts are well-paid and work on interesting projects that often have direct and meaningful impacts on their organizations’ performance. They generally have broad skill sets that span soft and technical skills. This fast-changing world of analytics provides a continuous learning environment, and skilled analysts will always have good prospects of finding jobs that suit their needs and lifestyle.