Get Specialized with our Financial Planning & Analysis (FP&A) Program

Support business leaders in their decision-making with best-in-class financial models to evaluate and forecast the financial performance of a company.

Ever spent hours deciphering a colleague’s financial model — hunting through scattered data, tracing cryptic formulas, and wondering what these numbers actually mean? These moments reveal the true cost of poor design. Thoughtful Excel model design is the foundation that determines whether your financial insights will guide decisions or gather digital dust.

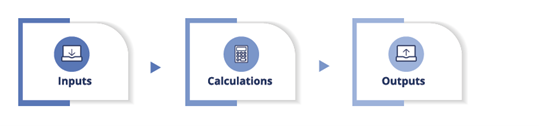

A common misstep is diving straight into inputs, then calculations, and finally outputs. This approach creates models that either oversimplify business dynamics or burden users with unnecessary complexity.

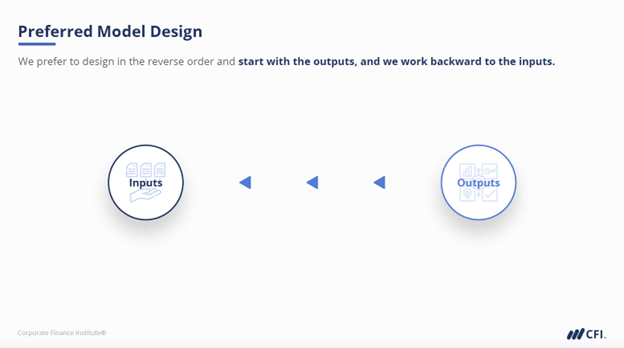

This guide walks through a better approach to designing effective Excel models: starting with outputs and working backward. You’ll discover how this reverse-order process keeps models focused, saves development time, and makes them valuable decision-making tools.

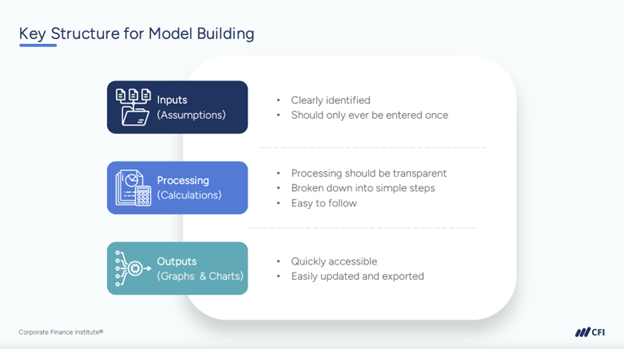

When people think about designing a financial model in Excel, they often imagine an inputs-first workflow. This traditional design process typically flows like this:

Logical as it seems, this inputs-first approach often leads to confusion and inefficiency. Halfway through, you may realize that key inputs are either missing or haven’t clearly defined your outputs.

A reverse-order method, starting with outputs instead of inputs, is not only more efficient but also maintains the focus on the most critical elements.

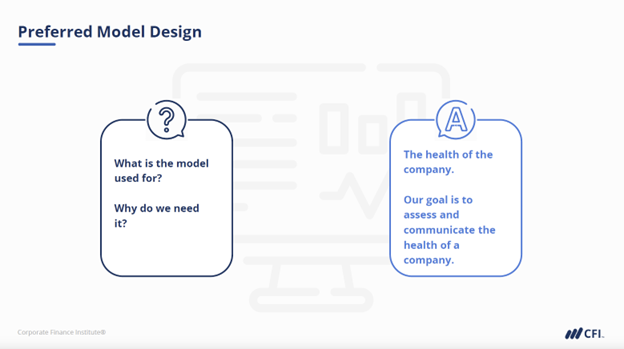

Financial models are ultimately decision-making tools. So, a logical first step is to identify the decisions — or questions — that your model needs to answer. What information does your company’s leadership need to solve problems and make informed decisions?

| Pro Tip |

|---|

| Before proceeding with an Excel model build: • Focus on what business leaders actually need for decision-making. • Identify the questions your model must answer. • Define the specific metrics needed to answer these questions. • Begin with your desired outputs to clarify the model’s objective. • Let these outputs determine the calculations and inputs. |

Example Scenario: Your CFO requests a model focused on revenue and cash flow key performance indicators (KPIs) for the current and previous years.

Key Questions Your Dashboard Should Answer:

Practical Steps:

This approach ensures your model maintains a clear objective throughout development, supporting business leaders with exactly the insights they need.

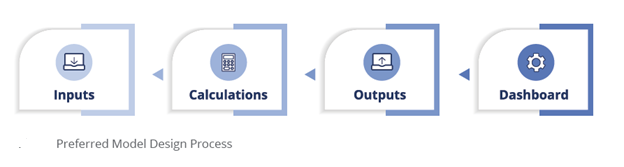

With clearly defined outputs, you’re ready to identify the calculations the model should include to arrive at the desired outputs. Then you’ll be ready for the last step of the design — determining the inputs that will power your model.

With clearly defined model outputs, you can begin backward-solving to identify the necessary calculations followed by inputs.

Scenario: You need to build a simple cash flow model with annual pro forma estimates.

Step 1: Identify Required Calculations: Determine exactly what calculations and supporting schedules you need to support your outputs.

Step 2: Define the Necessary Inputs: Backtrack further to identify precisely what inputs will drive those calculations.

The examples used here are simplified to highlight the effectiveness of starting your Excel model design with outputs. In real-world practice, FP&A roles and financial modeling needs and complexity vary significantly from company to company.

That said, mastering this output-focused approach helps you build actionable and relevant models, even as complexity grows. You ensure every part in your model serves a purpose. Less confusion and more clarity. Just actionable information.

An outputs-first approach to Excel model design saves valuable time, enhances output clarity, and increases overall usefulness. When your model begins with the specific questions business leaders need answered, the entire design process becomes more focused and efficient.

Implementing design methodology requires both conceptual understanding and practical skills. While this guide provides the framework, developing proficiency in outputs-first modeling demands hands-on practice and professional guidance. Taking the next step in your modeling expertise can transform your effectiveness as an FP&A professional.

Ready to level up your FP&A modeling skills? CFI’s FP&A Specialization equips you with the skills and knowledge to excel as an FP&A professional. You will emerge from this program prepared to support business leaders with top-tier financial models, budgets, forecasts, analysis, and more. Learn the techniques used by top finance teams at Amazon, JPMorgan, and PwC.