Get Specialized with our Financial Planning & Analysis (FP&A) Program

Support business leaders in their decision-making with best-in-class financial models to evaluate and forecast the financial performance of a company.

Accurately planning for employee compensation is essential for managing labor costs, budgeting, and financial planning. But even small headcount forecasting errors can have ripple effects across payroll, cash flow, and workforce planning. Forecasts that don’t reflect real scheduling constraints, benefits costs, or payroll timing can lead to budget shortfalls and cash flow issues.

Many FP&A professionals rely on Excel models for headcount forecasting, but errors in formulas, data validation, or scheduling logic can lead to unreliable results. The good news? You can avoid these mistakes with a few simple Excel functions. This guide breaks down five common errors in headcount forecasting and explains how to avoid them.

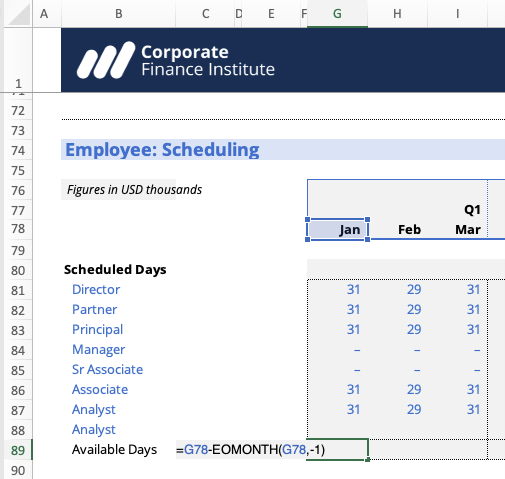

One of the biggest forecasting errors is assuming that salaries can be divided evenly across 12 months. In reality, the number of workdays in each month varies, and failing to adjust for this difference can lead to inaccurate payroll forecasts.

For example, if you allocate a fixed salary of $60,000 as $5,000 per month, you ignore that some months have more workdays than others. Over time, this creates discrepancies in payroll expenses and affects financial planning.

Instead of dividing salaries equally, use workday-based allocations to reflect actual payroll expenses:

This approach ensures that monthly salary forecasts reflect real-world conditions, improving accuracy in financial planning.

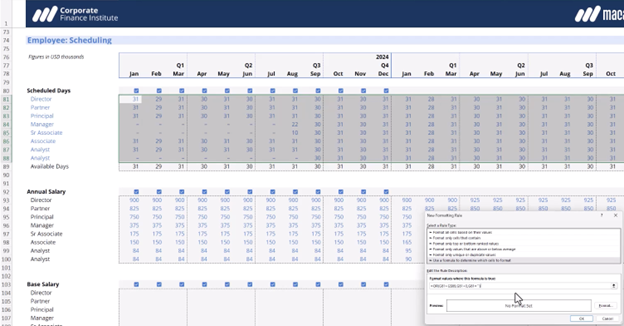

Another common issue is allocating more workdays than actually exist in a month. This often happens when forecasting full-time employees across multiple months without factoring in weekends, holidays, or time off.

For example, if your model assigns 32 workdays to an employee in January, your total labor costs become overestimated, leading to inflated budget projections.

To prevent this error, implement safeguards that flag over-scheduled employees:

A well-structured FP&A headcount model will immediately flag these errors, helping you avoid misallocations and maintain accurate labor cost forecasting.

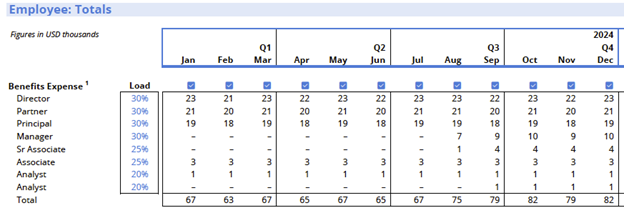

Base salaries alone do not capture the full cost of an employee. If you overlook benefits, taxes, or bonuses, your forecast will underestimate compensation expenses, leading to budgeting shortfalls.

For example, a $75,000 salary with a 30% benefits load actually costs $97,500 annually, yet many forecasts only include the base amount. Similarly, annual bonuses that fluctuate each year often go unaccounted for in static forecasting models.

To avoid missing key compensation costs:

In a dynamic headcount forecasting model, these adjustments ensure total compensation is accurately forecast, not just base salary costs.

Manual data entry is a major source of forecasting errors. If you’re not using built-in alerts, validation rules, and automated checks, you may overlook data gaps or incorrect inputs.

For example, without error detection, your model might include:

Rather than manually scanning for issues, automate error detection with Excel’s built-in tools:

By incorporating automated checks, you can quickly identify and correct errors before they impact financial models.

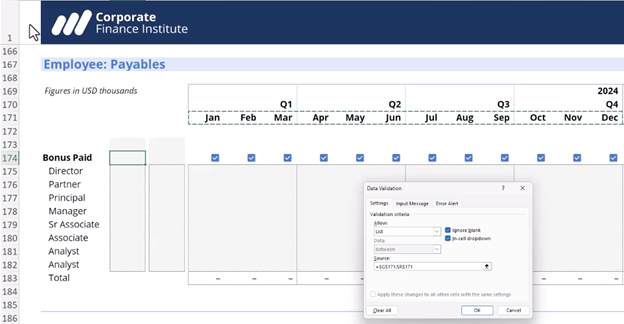

Forecasting salary expenses is not the same as forecasting cash flow impact. Many models account for salary costs but fail to reflect the timing of payroll payments, which can cause cash flow mismatches.

For example, if you forecast a $100,000 payroll expense for Q4 but fail to account for December’s payment being made in January, your cash flow projection will overestimate Q1 cash availability.

To align salary expenses with cash flow timing, use:

By tracking payroll accruals properly, your cash flow model stays aligned with actual payment schedules, preventing funding gaps and liquidity miscalculations.

Avoiding headcount forecasting errors requires structured modeling, automation, and proactive validation. Whether you’re forecasting for salary expenses, benefits, or workforce capacity, applying formula-driven forecasting techniques ensures more reliable financial planning.

By implementing workday-based salary allocations, error detection tools, and accrual-based forecasting, you can prevent budget misalignment and improve forecasting accuracy.

Want to take your headcount forecasting skills to the next level? Enroll in CFI’s FP&A Professional Headcount Forecasting & Analysis course to master best practices in financial modeling and workforce financial planning.

The Role of Supporting Schedules in 3-Statement Modeling

Four Forecasting Models Compared (And When You Should Use Each)

10 Common Causes of Imbalance in 3-Statement Models (And How to Fix Them)