Get Specialized with our Financial Planning & Analysis (FP&A) Program

Support business leaders in their decision-making with best-in-class financial models to evaluate and forecast the financial performance of a company.

Imagine you’re an FP&A analyst for a consumer goods company. One day, your manager hands you two proposals — one to replace outdated machinery (a maintenance investment) and another to fund an expansion into a new market (a growth investment).

Faced with two different proposals, you need to decide which analysis method to use — cost-benefit, discounted cash flow, or scenario analysis.

In capital allocation, the depth of analysis should match a project’s size and strategic impact. This guide breaks down the differences between growth and maintenance investments and highlights the analytical methods best suited for each, so you can deliver clear, data-driven recommendations.

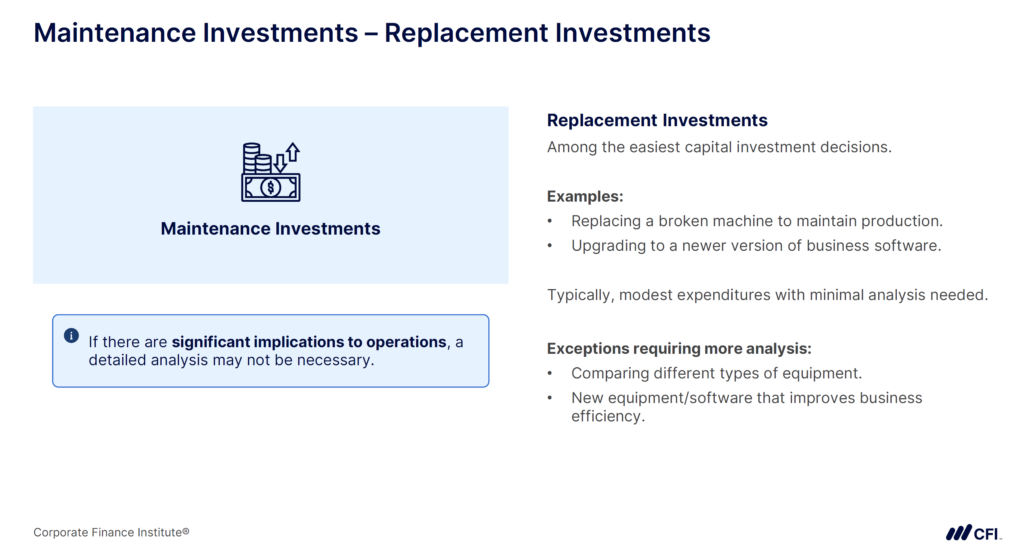

Before diving into the details of growth vs. maintenance investments, it’s important to define what maintenance investments are. These expenditures keep day-to-day operations running smoothly, preserve cash flow, and prevent disruptions. Typically, they carry lower risk and uncertainty, so you usually need less intensive analysis.

Think of replacement investments as straightforward maintenance decisions. When essential machinery breaks down or your software becomes outdated, the need to replace it is often clear-cut. Since these costs are relatively modest, you generally don’t require a complex financial model — unless you’re comparing multiple options or the upgrade promises significant efficiency gains.

Companies often make investments to fulfill regulatory requirements, like those under the US Occupational Safety and Health Administration (OSHA) and the UK’s Health and Safety Executive (HSE). Adhering to regulations is usually non-negotiable. Because they’re essentially required, they often don’t need extensive analysis — unless you’re evaluating different compliance strategies or considering major operational shifts.

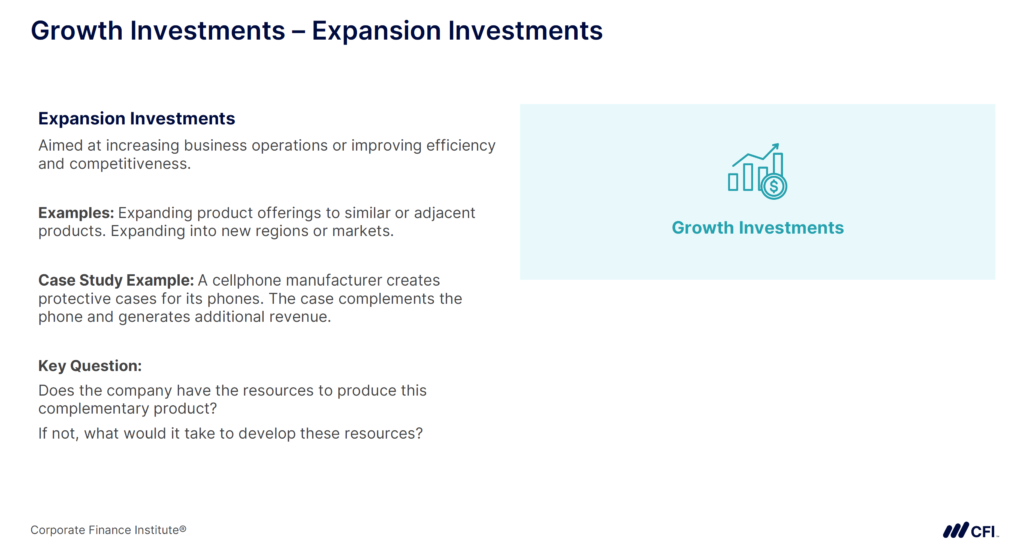

Growth investments, or growth capex, are the initiatives designed to expand your business or enhance its capabilities.

Unlike maintenance investments, growth investments carry higher risk and greater uncertainty. They require a deeper level of analysis because they aim to create new value — whether by increasing revenue, opening up new markets, or developing innovative products or services.

Expansion investments help a company extend its product lines or break into new markets.

Imagine a mobile phone manufacturer branching out by adding complementary accessories like protective cases.

With more variables like competitive positioning and resource allocation, growth initiatives demand robust forecasting and scenario planning to ensure they deliver on their promise.

Growth investments sometimes mean venturing into entirely new territory.

For instance, if that same phone manufacturer decides to offer cellular service, it’s stepping into a new business area. These moves are inherently riskier and call for an especially thorough analysis to understand the market dynamics and potential operational challenges.

Mergers and acquisitions also fall under growth investments. As an FP&A professional, you might only play a peripheral role in these deals, but M&A is a key growth strategy that often requires specialized analysis.

In making capital allocation decisions about growth vs. maintenance investments, the real question is how detailed your analysis should be.

High-risk projects with large budgets or critical strategic importance demand robust modeling, such as discounted cash flow (DCF) or detailed scenario analysis. Meanwhile, straightforward maintenance tasks might need a simpler cost-benefit analysis.

Keep in mind that the stakes can change. What starts as a simple maintenance fix might turn into a major efficiency driver. Or, a growth initiative can quickly expand in scope.

Your analysis should be flexible, adapting to the evolving risk and reward profile of each investment.

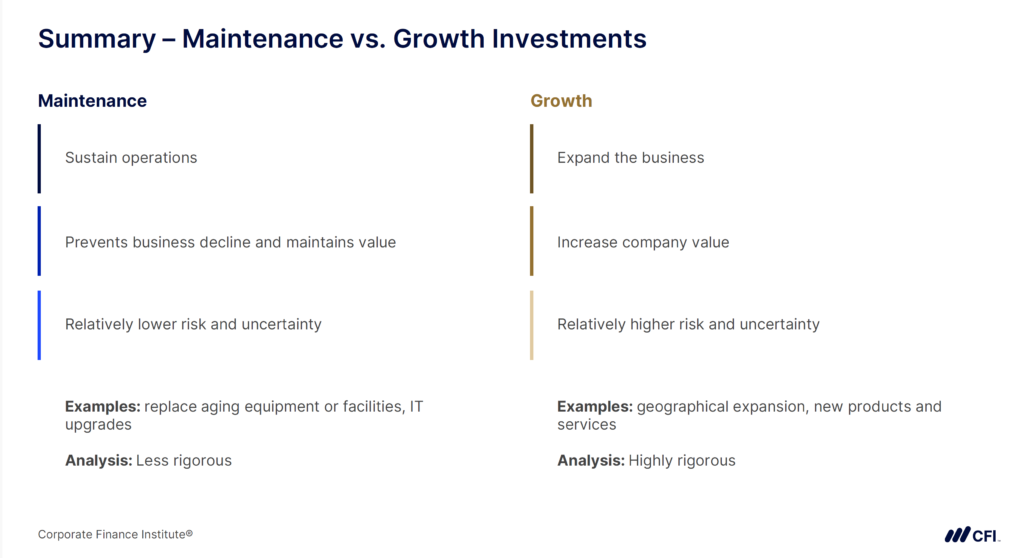

Maintenance investments are about operational continuity and stability with lower uncertainty and simpler analysis. Whether it’s replacing outdated equipment or meeting regulatory standards, these investments help keep a business running smoothly.

Growth investments, on the other hand, aim to create new value. They involve expanding into new markets or developing innovative products, but they come with higher risk and require more rigorous financial modeling.

By understanding these differences, you can tailor your analysis appropriately. Use a quick ROI check for straightforward maintenance investments, and deeper modeling for high-stakes growth initiatives.

For effective capital allocation of maintenance and growth investments:

Distinguishing between growth vs. maintenance investments is essential for analyzing capital allocation proposals. Maintenance investments focus on preserving operations and can often be evaluated with a straightforward cost-benefit lens. Growth initiatives, on the other hand, require deeper modeling and judgment to assess potential returns and strategic alignment.

Each analysis you conduct strengthens the foundation for smarter, more resilient business decisions. By aligning your approach to the specific risk profile and expected impact of each investment, you can deliver actionable insights that leadership can trust. This is how FP&A professionals become strategic partners — by shaping decisions that drive value.

Looking to sharpen that strategic lens even further? CFI’s Making Effective Business Decisions course gives you the tools to evaluate investments through a structured, practical framework. You’ll learn how to assess both operational and strategic opportunities — and emerge ready to make sound, data-backed recommendations that move the business forward.

Enroll now and take your decision-making skills to the next level!